Short-term health insurance is often marketed as a cost-effective alternative to traditional health plans, but its affordability can be misleading. While premiums are typically lower than those of comprehensive plans, short-term policies come with significant limitations, such as high deductibles, limited coverage, and exclusions for pre-existing conditions. Additionally, these plans often cap payouts, leaving policyholders vulnerable to substantial out-of-pocket expenses in the event of serious illness or injury. When considering the true cost, it’s essential to weigh not only the monthly premium but also the potential financial risks associated with inadequate coverage. Ultimately, while short-term health insurance may seem inexpensive upfront, it can prove costly in the long run for those needing comprehensive medical care.

Explore related products

$11.26 $19.99

What You'll Learn

![]()

Monthly Premiums vs. Coverage Limits

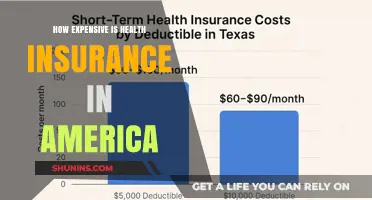

Short-term health insurance plans often lure consumers with their lower monthly premiums, which can be as much as 50-80% cheaper than comprehensive ACA-compliant plans. For a healthy 30-year-old, this might translate to a monthly premium of $50-$100, compared to $300-$500 for a traditional plan. However, these savings come with a critical trade-off: coverage limits that can leave you financially exposed when you need care the most.

Consider the fine print: short-term plans frequently cap payouts at $250,000 to $2 million per policy period, far below the $8 million average cost of a prolonged hospital stay for a severe condition like sepsis. Additionally, most exclude pre-existing conditions, maternity care, mental health services, and prescription drugs. For instance, a plan with a $5,000 deductible and a $1 million cap might seem robust until you realize it won’t cover a $300,000 cancer treatment or a $50,000 emergency surgery if the condition is deemed pre-existing.

To navigate this trade-off, evaluate your risk tolerance and health history. If you’re under 35, rarely visit the doctor, and need temporary coverage (e.g., between jobs), a short-term plan with a $75 monthly premium and a $500,000 cap might suffice. However, if you’re over 40, have chronic conditions, or anticipate high-cost care, the $200 monthly savings could evaporate in a single medical event, leaving you with bills exceeding $100,000.

A practical tip: calculate your potential out-of-pocket costs by multiplying the plan’s deductible (often $10,000+) by the likelihood of needing care. For example, a 25-year-old with no health issues might risk $10,000 for a $50 monthly premium, but a 45-year-old with hypertension should reconsider, as their risk of hospitalization is 3x higher. Always compare these costs to the $1,200-$2,400 annual premium difference between short-term and comprehensive plans.

Ultimately, the choice between monthly premiums and coverage limits hinges on whether you’re insuring against catastrophic events or merely filling a temporary gap. Short-term plans excel at the latter but falter at the former. Before signing, ask yourself: “Can I afford a $50,000 medical bill if this plan doesn’t cover my needs?” If the answer is no, the lower premium may be a costly illusion.

Best Affordable Medical Insurance Plans in New York

You may want to see also

Explore related products

![]()

Deductibles and Out-of-Pocket Costs

Short-term health insurance plans often lure consumers with lower premiums, but the trade-off lies in higher deductibles and out-of-pocket costs. Unlike comprehensive plans, which may have deductibles ranging from $1,000 to $3,000, short-term plans can set deductibles as high as $10,000 or more. This means you’ll pay significantly more before the plan begins to cover expenses, making it a risky choice for those with frequent medical needs. For example, a 30-year-old with a short-term plan might face a $5,000 deductible, while a similar age group on an ACA-compliant plan could have a deductible closer to $2,000.

Understanding out-of-pocket costs is equally critical. These include copays, coinsurance, and any expenses beyond the deductible. Short-term plans often cap out-of-pocket maximums at $10,000 or higher, compared to the $9,450 limit for ACA-compliant plans in 2023. For instance, if you require a $20,000 surgery, you could pay the full deductible plus 20% coinsurance, totaling $7,000 or more, depending on the plan’s terms. This lack of financial predictability can turn a seemingly affordable plan into a costly burden during emergencies.

To mitigate these risks, evaluate your health needs carefully. If you’re under 30 and rarely visit the doctor, a short-term plan with a $7,500 deductible might suffice as a temporary safety net. However, if you have chronic conditions or anticipate medical expenses, the high deductible could negate any premium savings. For example, a diabetic requiring regular insulin and check-ups would likely spend more on out-of-pocket costs than they save on premiums.

Practical tips include comparing deductibles across plans and calculating potential annual costs based on your health history. For instance, if you typically spend $1,500 annually on healthcare, a plan with a $5,000 deductible might not offer meaningful coverage. Additionally, consider pairing short-term insurance with a health savings account (HSA) to offset out-of-pocket expenses. While short-term plans can provide temporary coverage, their high deductibles and out-of-pocket costs demand careful scrutiny to avoid unexpected financial strain.

Health Insurance Liability: Understanding Coverage for Dependents and Beneficiaries

You may want to see also

Explore related products

![]()

Pre-Existing Conditions Exclusions

Short-term health insurance plans often exclude coverage for pre-existing conditions, a critical factor that significantly impacts their cost and value. These exclusions are a double-edged sword: they keep premiums lower by limiting risk for insurers but leave individuals with ongoing health issues vulnerable to out-of-pocket expenses. For example, a 30-year-old with asthma might find short-term plans affordable at $100–$200 monthly, but any asthma-related treatment would likely be denied, rendering the plan ineffective for their primary healthcare needs. Understanding these exclusions is essential for anyone considering short-term coverage.

Analyzing the mechanics of pre-existing condition exclusions reveals their broad scope. Insurers define pre-existing conditions as any health issue diagnosed or treated within a specific look-back period, typically 2–5 years. This includes chronic conditions like diabetes, hypertension, or mental health disorders, but also acute issues like recent surgeries or injuries. For instance, a policyholder who had knee surgery two years ago might be denied coverage for any knee-related complications, even if unrelated to the original procedure. This lack of coverage for ongoing or recurring issues underscores the limited utility of short-term plans for those with medical histories.

To navigate these exclusions effectively, individuals must scrutinize policy details before purchasing. Start by reviewing the plan’s definition of pre-existing conditions and the look-back period. Next, assess your medical history to identify potential exclusions. For example, if you’ve been prescribed medication for high cholesterol in the past three years, most short-term plans will exclude coverage for cardiovascular-related care. Practical tips include keeping a detailed record of past diagnoses and treatments, consulting with a broker to clarify exclusions, and considering alternative options like COBRA or ACA-compliant plans if pre-existing conditions are a concern.

Comparatively, short-term plans with pre-existing condition exclusions are best suited for healthy individuals facing temporary coverage gaps, such as recent graduates or those between jobs. For instance, a 25-year-old with no chronic conditions might find a $150 monthly plan adequate for covering unexpected accidents or illnesses during a three-month job transition. However, for someone with a pre-existing condition, the same plan could lead to financial strain if they require treatment. The takeaway is clear: short-term insurance is a cost-effective option only for those without ongoing health needs, making it a niche solution rather than a universal answer to affordability.

Puppy Medical Insurance: Is It Worth It?

You may want to see also

Explore related products

$29.99 $29.99

![]()

Duration and Renewal Restrictions

Short-term health insurance plans typically offer coverage for a limited duration, ranging from 30 days to 364 days, depending on the state and insurer. This temporary nature is both a strength and a limitation, making it crucial to understand the duration and renewal restrictions before committing. For instance, in states like California and New Jersey, plans are capped at 90 days, while others, such as Texas and Florida, allow up to 364 days. Knowing your state’s regulations is the first step in assessing whether short-term insurance aligns with your needs.

Renewal restrictions are a critical aspect often overlooked by consumers. Unlike long-term health plans, short-term policies cannot be renewed indefinitely. Most insurers limit renewals to a maximum of 36 months of cumulative coverage within a five-year period. This means if you’ve used a short-term plan for 12 months, you may only have 24 months left before you’re ineligible for further coverage under the same type of plan. Additionally, some states prohibit renewals entirely, forcing policyholders to seek alternative coverage once their term ends.

The inability to renew short-term plans without gaps in coverage can pose significant risks, especially for individuals with ongoing medical needs. For example, if you’re undergoing treatment for a chronic condition, a sudden lapse in coverage could leave you financially vulnerable. To mitigate this, consider pairing short-term insurance with a health savings account (HSA) or exploring supplemental policies that cover specific services, such as prescription drugs or urgent care visits.

From a cost perspective, the limited duration and renewal restrictions of short-term health insurance can make it cheaper upfront, with monthly premiums often 50–80% lower than ACA-compliant plans. However, this affordability comes at a trade-off: short-term plans are not required to cover essential health benefits like maternity care, mental health services, or pre-existing conditions. Before opting for this route, evaluate your health history and anticipated needs to ensure the savings don’t outweigh the potential risks.

Finally, practical planning is essential when navigating short-term health insurance. If you anticipate needing coverage beyond the initial term, research alternative options in advance, such as employer-sponsored plans, COBRA, or state-based marketplaces. Some insurers also offer “bridge” plans designed to provide temporary coverage until you qualify for a more permanent solution. By proactively addressing renewal restrictions, you can avoid gaps in coverage and ensure continuous protection for yourself and your family.

Steps to Launch Your Health Insurance Broker Career in New Jersey

You may want to see also

Explore related products

![]()

Cost Comparison with ACA Plans

Short-term health insurance plans often appear cheaper upfront, with monthly premiums ranging from $50 to $200, compared to ACA (Affordable Care Act) plans, which average $400 to $700 monthly for individuals. This price disparity stems from short-term plans’ limited coverage and exclusions for pre-existing conditions, preventive care, and prescription drugs. ACA plans, mandated to cover essential health benefits, offer comprehensive protection but at a higher cost. For healthy individuals under 30 with minimal healthcare needs, short-term plans might seem like a budget-friendly option. However, this comparison hinges on understanding the trade-offs in coverage and potential out-of-pocket expenses.

Consider a 28-year-old nonsmoker in Texas: a short-term plan might cost $90 monthly with a $5,000 deductible, while an ACA bronze plan could be $350 monthly with a $6,000 deductible. The ACA plan’s higher premium includes subsidies for those earning under 400% of the federal poverty level, reducing costs significantly. Short-term plans lack subsidies, making them less affordable for lower-income individuals. Additionally, ACA plans cap out-of-pocket maximums at $9,450 for individuals in 2023, whereas short-term plans often have no such limits, exposing policyholders to higher financial risk in case of serious illness or injury.

A persuasive argument for ACA plans lies in their long-term value. While short-term plans save money in months of good health, they provide little to no coverage for chronic conditions, maternity care, or mental health services. For instance, a short-term plan might deny coverage for a $50,000 hospital stay due to a pre-existing condition, leaving the policyholder responsible. In contrast, ACA plans guarantee coverage regardless of health history, making them a safer bet for unexpected medical needs. For families or individuals with ongoing health concerns, the higher premium of an ACA plan is an investment in financial stability.

To illustrate the cost comparison practically, imagine a scenario where a policyholder requires emergency surgery. Under a short-term plan, the $10,000 procedure might be partially or fully denied, leaving the individual with a hefty bill. An ACA plan, with its broader coverage, would cover the procedure after the deductible and coinsurance, limiting out-of-pocket costs. This example highlights the importance of evaluating not just monthly premiums but also potential liabilities. For those prioritizing affordability over comprehensive coverage, short-term plans may suffice temporarily, but ACA plans offer greater peace of mind and protection against catastrophic expenses.

In conclusion, the cost comparison between short-term health insurance and ACA plans reveals a clear trade-off: lower premiums versus comprehensive coverage. Short-term plans appeal to those seeking temporary, budget-friendly options, but their limitations can lead to significant financial risk. ACA plans, though pricier, provide robust protection and subsidies for eligible individuals, making them a more reliable choice for long-term health security. When deciding, assess your health needs, budget, and risk tolerance to choose the plan that aligns best with your circumstances.

Applying for Medical Insurance in California: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Short-term health insurance premiums vary widely but generally range from $50 to $200 per month, depending on factors like age, location, coverage limits, and deductible amounts.

Yes, short-term health insurance is often significantly cheaper than traditional plans because it offers limited coverage, excludes pre-existing conditions, and may not cover essential health benefits like preventive care or prescription drugs.

Yes, additional costs can include high deductibles (often $1,000 or more), copays, and out-of-pocket expenses for services not fully covered. Some plans also charge separate fees for specialist visits or hospital stays.

Yes, costs can vary by state due to differences in regulations, healthcare costs, and available plans. States with fewer restrictions on short-term plans may offer lower premiums, while states with stricter rules may have higher costs.