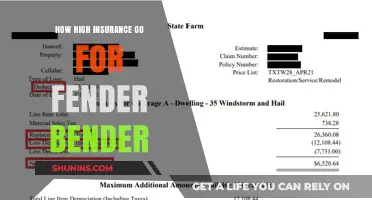

Insurance rates are on the rise, with many people facing surging auto and home insurance premiums. There are a multitude of factors that can cause insurance rates to increase, including accidents, violations, age, and location. Accidents and violations indicate to insurance companies that a driver is more likely to have another accident and file a claim, resulting in a rate increase. Age can also be a factor, with insurance companies viewing older drivers as riskier than middle-aged adults. Additionally, insurance rates can be influenced by location, with drivers in metropolitan areas or high-crime neighbourhoods often paying more due to the increased risk of accidents or theft. Other factors that can contribute to rising insurance rates include inflation, supply chain disruptions, and severe weather events.

Explore related products

What You'll Learn

![]()

Accidents and violations

The nature of the accident or violation is another critical factor. At-fault accidents generally lead to higher premium increases compared to no-fault accidents. For example, an at-fault accident can result in an average annual increase of $1,110 for a full-coverage policy. Accidents involving driving under the influence (DUI) or reckless driving may impact premiums for up to 10 years. The severity of the collision and the presence of any driving violations, such as speeding, are also taken into account.

Age is another determinant of rate increases. Younger drivers are often considered a risky group to insure, and their rates may increase more significantly after an accident or violation. Conversely, senior citizens may qualify for reduced rates or discounts if they store their vehicles for extended periods.

Some insurance companies offer accident forgiveness programs, which prevent rates from increasing after certain types of accidents, especially minor ones or first-time incidents. These programs may be offered as incentives for customer loyalty or maintained driving records over several years.

Finally, the impact of accidents and violations on insurance rates is not immediate and permanent. While accidents remain on driving records for several years, insurance rates may drop back down after a few years of claim-free driving. Shopping around for insurance after an accident can help identify more affordable options, as rates vary significantly between companies.

Personal Injury Protection: What Insurance to Carry

You may want to see also

Explore related products

![]()

Inflation and supply chain issues

The rise in inflation has also contributed to higher claims payouts for property and casualty insurance. The increasing cost of construction materials and labour has led to higher repair and replacement costs for damaged property. Insurers are forced to raise premiums to cover these increased costs. Additionally, inflation diminishes the buying power of money, further driving insurers to raise rates to keep up with increasing expenses.

Supply chain issues have also played a role in rising insurance rates. Post-pandemic supply chain disruptions have resulted in higher costs for vehicle parts, prolonged repair times, and increased rental car expenses. These factors have escalated insurance claims and costs, leading to higher premiums for policyholders. The increased frequency and severity of claims, driven by rising medical costs and the higher expense of repairing modern vehicles, have further contributed to the rise in insurance rates.

Moreover, legislative changes and legal system abuse have also impacted insurance rates. Stricter regulations on insurance practices have inadvertently increased administrative costs for insurers, which are often passed on to consumers in the form of higher premiums. Aggressive marketing and excessive third-party litigation have also driven up the cost of claims and increased premiums.

Fixing Glass: Will My Insurance Rates Increase?

You may want to see also

Explore related products

![]()

Age and experience

According to the Centers for Disease Control and Prevention (CDC), the risk of motor vehicle crashes is higher among teens aged 16 to 19 than any other age group. The fatal crash-per-mile rate for licensed drivers in this age bracket is nearly three times that of individuals aged 20 and older. Teenage drivers are also more likely to engage in distracted driving, which, coupled with their inexperience, makes them a greater risk on the road.

As drivers gain experience and age, their insurance rates tend to decrease. The biggest drop in insurance rates typically occurs between the ages of 18 and 19, with rates decreasing by over 20% on average. By the time drivers reach 25, they are considered significantly lower risk, and their insurance rates stabilize, with premiums about 65-70% lower than at age 16. Drivers in their late twenties and early thirties continue to benefit from lower insurance rates, provided there are no changes in other factors such as location, credit score, or marital status.

However, it is important to note that insurance rates may start to increase again for senior drivers due to physical and cognitive limitations that can negatively impact their driving abilities. Older drivers may experience impaired vision or hearing, slower response times, and cognitive decline, making them more prone to accidents. While age is a significant factor in determining insurance rates, other factors, such as driving record, location, and gender, also play a role in calculating premiums.

Insurance Economics: Risk Management and Financial Stability

You may want to see also

Explore related products

![]()

Location and local issues

The type of location, whether it is a city or a rural area, can also impact insurance rates. Urban areas tend to have higher rates of vandalism, theft, and collisions, leading to increased premiums. However, it's not always the case that rural areas have lower insurance rates. States with wide-open spaces and small populations, like Montana, may have higher insurance rates due to residents travelling longer distances as part of their daily routine, increasing the likelihood of accidents.

Weather patterns and natural disasters in specific regions can also influence insurance rates. If an area experiences severe weather, such as hail storms or hurricanes, it can lead to more vehicle damage and insurance claims. As a result, insurers may increase rates to compensate for their higher expenses. Climate change, which contributes to more frequent disasters, is another factor that can indirectly impact insurance rates over time.

In addition to natural disasters, local issues such as the percentage of uninsured drivers in a state can affect insurance rates. For example, in Mississippi, a high percentage of uninsured drivers contribute to higher insurance rates for insured drivers. This is because insurance companies have to cover the higher expenses associated with accidents involving uninsured motorists.

Other local factors that can influence insurance rates include treacherous roadways and a high percentage of drunk drivers. These issues can increase the likelihood of accidents and, consequently, insurance claims, leading to higher insurance rates for residents in those areas.

Traffic Tickets: Insurance Premiums and You

You may want to see also

Explore related products

$79.99 $99.99

![]()

Vehicle type and usage

The type of vehicle you drive can significantly impact your insurance rates. The make and model of your car can affect your insurance rate based on how often that make is involved in insurance claims, how much it costs to repair or replace the vehicle, and the safety features it has. For example, an expensive car model usually has a higher insurance rate for comprehensive and collision coverage. Certain makes and models are also known to cause more damage than other vehicles. The more claims a make and model has and the more it costs to repair, on average, the higher your rate will be. However, if your car has great safety ratings, your rate may be lower. Similarly, safety features such as anti-lock brakes and proximity warnings may also make a difference. The likelihood of theft for similar models is another factor that determines insurance rates.

The age of your vehicle could also impact insurance costs. Both newer and older cars can cost more to fix, and premium parts on expensive vehicles could be pricey to repair. Therefore, a luxury SUV could potentially cost more to insure than a non-luxury counterpart. The size of a vehicle also makes a difference in road accidents. Larger vehicles usually fare better than compact cars because of the impact of the circumstances. Since less damage means a lower repair cost, this can work in favor of SUVs. However, if your car causes damage in an accident, it may increase your insurance rates due to comprehensive and collision costs.

The amount of driving you do is another key factor in determining insurance rates. Driving less frequently means you’re less likely to be exposed to risk, so your rates will be lower if you drive a few miles per week compared to if you drive 2 hours a day, 5 days a week.

Workers' Comp: Self-Insured or Carrier-Insured?

You may want to see also

Frequently asked questions

Insurance rates can go up immediately after an accident, especially if you were at fault. Accidents indicate a higher risk of future claims, and insurance companies will price you accordingly.

Yes, changing the address where your car is kept can increase your insurance rate. Moving to a high-crime or high-congestion area will likely result in higher premiums.

Yes, insurance rates often increase as drivers age, especially for seniors. Insurance companies view older drivers as riskier than middle-aged adults, which can lead to higher premiums.

Yes, adding a new driver, especially a teenage or inexperienced driver, can increase your insurance rate. This is because having multiple drivers increases the risk of accidents and claims.

Yes, insurance rates often increase with overall inflation. Additionally, factors such as supply chain disruptions, rising repair costs, and severe weather events can contribute to rising insurance premiums.