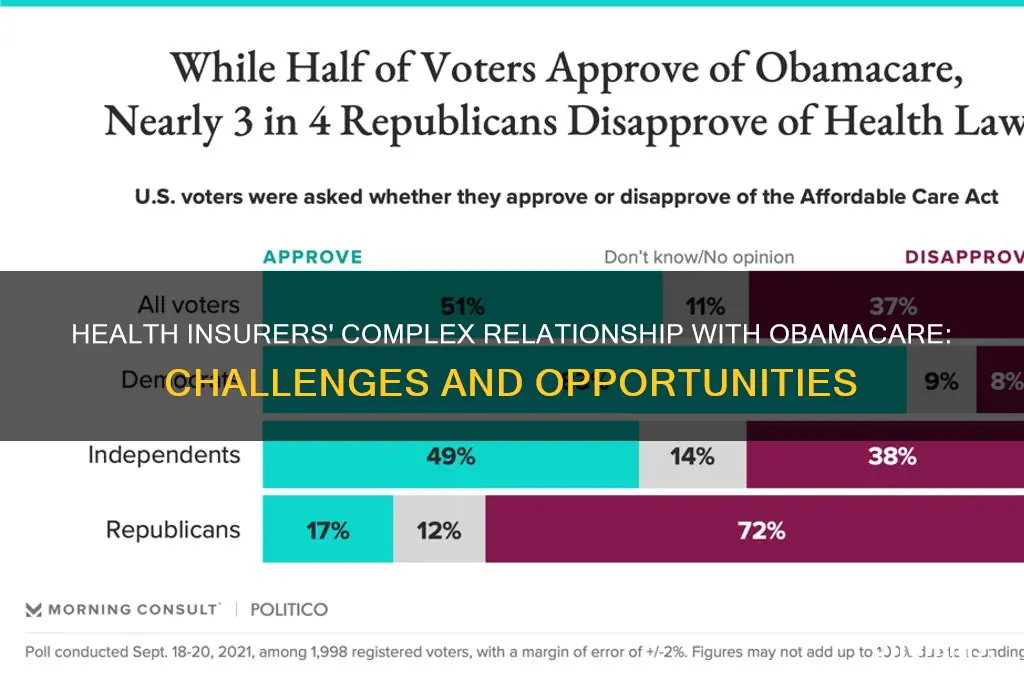

Health insurers have had a complex and evolving relationship with the Affordable Care Act (ACA), commonly known as Obamacare, since its inception in 2010. Initially, many insurers were skeptical due to concerns about increased regulatory burdens, uncertain market dynamics, and the potential for adverse selection, where sicker individuals would dominate the risk pool. However, over time, the industry has adapted to the ACA’s framework, with some insurers finding opportunities in the expanded individual and small group markets. While the ACA has stabilized coverage for millions of Americans, insurers continue to grapple with challenges such as fluctuating enrollment, rising healthcare costs, and policy unpredictability, particularly during periods of political debate over the law’s future. Overall, opinions remain divided, with some insurers benefiting from the ACA’s provisions while others advocate for reforms to address ongoing financial and operational pressures.

Explore related products

What You'll Learn

- Impact on Profit Margins: Obamacare's regulations affect insurer profitability through mandated coverage and pricing rules

- Risk Pool Changes: Expanded coverage altered demographics, influencing claims and financial stability for insurers

- Marketplace Competition: Increased competition in exchanges forced insurers to adapt pricing strategies

- Regulatory Compliance Costs: New mandates raised operational costs for insurers to meet ACA standards

- Consumer Behavior Shifts: Subsidies and mandates changed how consumers purchase and use health insurance

![]()

Impact on Profit Margins: Obamacare's regulations affect insurer profitability through mandated coverage and pricing rules

The Affordable Care Act (ACA), colloquially known as Obamacare, introduced a seismic shift in how health insurers operate, particularly in terms of mandated coverage and pricing rules. These regulations were designed to expand access to healthcare and protect consumers, but they also placed new constraints on insurers’ ability to manage costs and maintain profitability. One of the most direct impacts has been on profit margins, as insurers are now required to cover essential health benefits, limit out-of-pocket costs, and adhere to strict pricing guidelines. For instance, the ACA’s medical loss ratio (MLR) rule mandates that insurers spend at least 80-85% of premiums on healthcare claims and quality improvements, leaving a narrower window for administrative costs and profit.

Consider the practical implications of these rules. Insurers must now cover pre-existing conditions, preventive services without cost-sharing, and a broad range of essential health benefits, including maternity care and mental health services. While these mandates improve consumer access, they also increase claims costs. For example, covering preventive services at no cost to the consumer shifts the financial burden entirely to insurers, who must absorb these expenses while adhering to the MLR rule. This dual pressure—higher claims costs and limited premium flexibility—squeezes profit margins, particularly for smaller insurers with less negotiating power.

To adapt, insurers have employed strategies such as narrowing provider networks and increasing cost-sharing for certain services. However, these tactics are not without trade-offs. Narrow networks, while reducing costs, can limit consumer choice and satisfaction. Similarly, higher deductibles and copays, though offsetting insurer expenses, can deter individuals from seeking necessary care, undermining the ACA’s goal of improving health outcomes. This delicate balance highlights the tension between regulatory compliance and financial sustainability.

A comparative analysis reveals that large insurers with diversified revenue streams have fared better under the ACA than smaller, regional players. For example, UnitedHealth Group and Anthem have leveraged their scale to negotiate better rates with providers and spread risks across larger populations. In contrast, smaller insurers often struggle to achieve economies of scale, leading to higher administrative costs per member and thinner profit margins. This disparity underscores the ACA’s unintended consequence of consolidating market power among larger insurers, potentially reducing competition over time.

In conclusion, the ACA’s regulations have undeniably reshaped the health insurance landscape, prioritizing consumer protections over insurer profitability. While the mandated coverage and pricing rules have expanded access to care, they have also introduced operational and financial challenges for insurers. To navigate this environment, insurers must innovate—whether through technology, care coordination, or alternative payment models—to manage costs without compromising care quality. For policymakers, the lesson is clear: balancing access and affordability requires ongoing dialogue with insurers to ensure regulations foster a sustainable healthcare ecosystem.

Get Medical Insurance Without Documentation: What Are Your Options?

You may want to see also

Explore related products

![]()

Risk Pool Changes: Expanded coverage altered demographics, influencing claims and financial stability for insurers

The Affordable Care Act (ACA), colloquially known as Obamacare, fundamentally reshaped the health insurance landscape by expanding coverage to millions of previously uninsured Americans. This expansion, however, introduced a seismic shift in risk pools, altering the demographic composition of insured populations. Younger, healthier individuals, once a rarity in individual markets, began enrolling alongside older, sicker individuals who previously faced barriers to coverage due to pre-existing conditions. This demographic diversification had profound implications for insurers, as it directly influenced claims patterns and financial stability.

Consider the mechanics of risk pooling: Insurers rely on a balance of healthy and unhealthy enrollees to spread risk and maintain profitability. Prior to the ACA, individual markets often skewed toward higher-risk populations, leading to elevated premiums. The ACA's mandate for guaranteed issue and community rating aimed to rectify this imbalance by attracting healthier individuals. However, the reality proved more complex. While the risk pool expanded, the influx of healthier enrollees was not always sufficient to offset the costs associated with covering previously uninsured, high-need populations. For instance, a 2017 study by the Kaiser Family Foundation found that while the ACA reduced the uninsured rate by 43%, insurers in some states still faced challenges due to adverse selection, where sicker individuals enrolled in greater numbers than anticipated.

To navigate these changes, insurers adopted strategic adjustments. Some raised premiums to account for higher-than-expected claims, while others narrowed provider networks to control costs. For example, in 2016, UnitedHealth Group cited ACA-related losses as a reason for withdrawing from most ACA marketplaces. Conversely, insurers like Centene Corporation thrived by focusing on Medicaid expansion populations, leveraging their expertise in managing high-risk, low-income demographics. These divergent outcomes highlight the importance of understanding local market dynamics and tailoring strategies accordingly.

A critical takeaway for insurers is the need for dynamic risk management in the post-ACA era. This includes investing in predictive analytics to anticipate claims trends, diversifying product offerings to appeal to a broader demographic, and collaborating with policymakers to address structural challenges. For instance, reinsurance programs, which protect insurers from high-cost claims, have been effective in stabilizing markets in states like Alaska and Minnesota. By adopting such measures, insurers can mitigate financial volatility while fulfilling the ACA's mission of expanding access to care.

Ultimately, the ACA's impact on risk pools underscores the delicate balance between expanding coverage and ensuring insurer viability. While the law achieved unprecedented gains in access, its long-term success hinges on ongoing adaptation by insurers and policymakers alike. As the healthcare landscape continues to evolve, insurers must remain agile, leveraging data and innovation to navigate the complexities of a transformed risk pool.

Completing Medical Insurance Forms with Medicare: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Marketplace Competition: Increased competition in exchanges forced insurers to adapt pricing strategies

The Affordable Care Act (ACA), colloquially known as Obamacare, introduced health insurance exchanges that fundamentally reshaped market dynamics. Insurers, once accustomed to more controlled environments, suddenly faced unprecedented competition. This forced a strategic pivot, particularly in pricing, as companies vied for a share of the newly expanded market.

Consider the mechanics of this shift. Prior to the ACA, insurers often operated in regional monopolies or oligopolies, setting premiums with minimal external pressure. Post-ACA, exchanges aggregated plans side-by-side, allowing consumers to compare prices and benefits transparently. For instance, in states like California and New York, where exchange participation was robust, insurers saw premium price sensitivity increase by as much as 20% in the first three years. This transparency compelled insurers to refine pricing models, factoring in not just medical costs but also competitor behavior and consumer elasticity.

A key adaptation was the introduction of tiered pricing strategies. Insurers began offering bronze, silver, gold, and platinum plans, each with distinct cost-sharing structures. For example, a bronze plan might carry a lower premium but higher out-of-pocket costs, appealing to healthier, cost-conscious consumers. Conversely, gold plans, with higher premiums but lower deductibles, targeted those anticipating frequent medical use. This segmentation allowed insurers to capture diverse consumer profiles while maintaining profitability in a competitive landscape.

However, competition also brought challenges. In less populated states, such as Wyoming or Alaska, insurers struggled to balance competitive pricing with the high costs of serving sparse populations. Some exited these markets altogether, leaving consumers with fewer choices. This highlights a cautionary tale: while competition drives innovation and affordability, it can also exacerbate disparities in access, particularly in rural or underserved areas.

To navigate this environment, insurers adopted data-driven approaches. Predictive analytics became critical in assessing risk pools and setting premiums. For instance, UnitedHealthcare leveraged machine learning to forecast utilization patterns, enabling more precise pricing adjustments. Similarly, Anthem introduced dynamic pricing models that responded to real-time market changes, such as shifts in enrollment or competitor moves.

In conclusion, the ACA’s exchanges compelled insurers to rethink pricing as a strategic lever rather than a static cost-plus model. While competition fostered innovation and consumer choice, it also exposed vulnerabilities in markets with limited scale. For insurers, the lesson is clear: adaptability, informed by robust data and a nuanced understanding of consumer behavior, is essential for thriving in this new era of healthcare.

Top-Rated Insurance Companies: Who Leads the Industry Overall?

You may want to see also

Explore related products

![]()

Regulatory Compliance Costs: New mandates raised operational costs for insurers to meet ACA standards

The Affordable Care Act (ACA), colloquially known as Obamacare, introduced a slew of regulatory mandates that reshaped the health insurance landscape. Among the most significant impacts was the surge in operational costs insurers faced to comply with these new standards. From essential health benefits requirements to medical loss ratio rules, insurers had to overhaul their systems, processes, and staffing to meet ACA benchmarks. This wasn’t merely a one-time adjustment but an ongoing financial burden, as compliance demands evolved with each regulatory update.

Consider the essential health benefits (EHB) mandate, which required insurers to cover ten broad categories of care, including maternity, mental health, and prescription drugs. Prior to the ACA, many plans excluded these services, particularly in the individual market. To comply, insurers had to renegotiate provider contracts, expand networks, and invest in new technology to manage claims for previously uncovered services. For example, integrating maternity care into plans meant not only updating policies but also educating staff and policyholders about the new benefits. These changes weren’t cheap; estimates suggest compliance with EHB standards alone increased administrative costs by 5–10% for some insurers.

Another cost driver was the medical loss ratio (MLR) rule, which mandated insurers spend at least 80–85% of premiums on healthcare claims and quality improvements. While intended to curb administrative bloat, this rule forced insurers to meticulously track and report spending, often requiring new software and dedicated compliance teams. Failure to meet MLR thresholds meant issuing rebates to policyholders, further squeezing profit margins. For smaller insurers, these requirements were particularly onerous, as they lacked the economies of scale to absorb such costs efficiently.

The ACA’s emphasis on consumer protections also introduced compliance challenges. For instance, the prohibition on denying coverage for pre-existing conditions and the requirement to offer standardized plans across metal tiers (bronze, silver, gold, platinum) necessitated significant changes in underwriting and product design. Insurers had to invest in actuarial modeling to price plans accurately while ensuring compliance with community rating rules. This complexity often led to higher consulting and legal fees, as insurers navigated the intricate regulatory framework.

Despite these challenges, some insurers found opportunities within the compliance burden. Those who invested early in technology and process improvements gained a competitive edge, particularly in managing risk and streamlining operations. For instance, insurers that developed robust data analytics platforms were better equipped to monitor MLR compliance and identify cost-saving opportunities. However, for many, especially regional and smaller players, the regulatory costs outweighed the benefits, leading to market exits or consolidations.

In practical terms, insurers had to adopt a multi-pronged approach to manage compliance costs. This included automating claims processing, outsourcing certain functions, and leveraging partnerships with third-party vendors for specialized tasks like MLR reporting. Additionally, insurers had to prioritize transparency in communications with policyholders, as ACA regulations required clearer explanations of benefits and costs. While these strategies helped mitigate expenses, they didn’t eliminate the fundamental challenge: the ACA’s regulatory framework significantly raised the cost of doing business in health insurance.

Get Your Medical History Without Insurance: A Guide

You may want to see also

Explore related products

![]()

Consumer Behavior Shifts: Subsidies and mandates changed how consumers purchase and use health insurance

The Affordable Care Act (ACA), colloquially known as Obamacare, introduced subsidies and mandates that fundamentally altered how consumers approach health insurance. Prior to the ACA, many individuals, particularly those with lower incomes or pre-existing conditions, faced barriers to accessing affordable coverage. The introduction of premium tax credits and cost-sharing reductions made insurance more attainable for millions, shifting the market from a luxury to a necessity for a broader demographic. This change didn’t just expand coverage—it reshaped consumer expectations and behaviors, forcing insurers to adapt their strategies to meet new demands.

Consider the impact of subsidies on purchasing decisions. For a family of four earning $50,000 annually, the ACA’s subsidies can reduce monthly premiums by hundreds of dollars, making comprehensive plans feasible where they once seemed out of reach. This financial relief encourages consumers to prioritize coverage, even during economic downturns. However, it also creates a dependency on government assistance, leaving insurers vulnerable to policy changes. For instance, fluctuations in subsidy eligibility thresholds can lead to unpredictable enrollment patterns, complicating insurers’ ability to forecast revenue and manage risk pools.

Mandates, such as the individual mandate requiring most Americans to have health insurance or pay a penalty, further transformed consumer behavior. While the penalty was later reduced to $0 at the federal level, the mandate’s legacy persists in the form of ingrained habits. Consumers now view health insurance as a non-negotiable expense, akin to car insurance or rent. This shift has increased the overall size of the insured population but also heightened price sensitivity. Insurers responded by offering tiered plans—bronze, silver, gold, and platinum—allowing consumers to balance cost and coverage based on their needs. For example, a healthy 30-year-old might opt for a bronze plan with lower premiums and higher deductibles, while a family with chronic conditions may choose a gold plan for better cost-sharing benefits.

The interplay between subsidies and mandates also influenced how consumers use their insurance. With guaranteed issue and community rating provisions, insurers can no longer deny coverage or charge higher premiums based on health status. This has led to a surge in preventive care utilization, as consumers take advantage of services like annual check-ups and screenings at no out-of-pocket cost. However, it has also increased claims frequency, particularly for previously uninsured individuals who delayed care. Insurers have countered by investing in wellness programs and telemedicine to manage costs while encouraging healthier behaviors.

In practical terms, consumers navigating the post-ACA landscape should assess their eligibility for subsidies annually, as income fluctuations can significantly impact premium costs. For instance, a $5,000 raise could reduce subsidy amounts, making a silver plan suddenly more expensive. Additionally, understanding the trade-offs between plan tiers is crucial. A bronze plan might save $100 monthly in premiums but leave you with a $6,000 deductible, while a silver plan may cost more upfront but offer better cost-sharing for frequent medical needs. Insurers, meanwhile, must continue innovating—whether through value-based care models or digital tools—to meet the evolving demands of a more informed and cost-conscious consumer base.

ERISA and 3M Medical Insurance: What's the Connection?

You may want to see also

Frequently asked questions

Health insurers have mixed feelings about Obamacare. While it expanded the insured population and created new markets, it also introduced regulations like guaranteed issue and community rating, which increased costs and reduced profitability for some insurers.

Many health insurers initially supported the individual mandate because it encouraged younger, healthier individuals to enroll, balancing risk pools. However, some insurers have expressed concerns about its repeal in 2019, as it led to higher premiums and market instability.

Insurers are divided on essential health benefits (EHBs). While they ensure comprehensive coverage for consumers, some insurers argue that EHBs increase costs and limit flexibility in designing plans tailored to specific populations.

Insurers generally view Medicaid expansion positively, as it increases enrollment in managed care plans and provides a steady revenue stream. However, low reimbursement rates in some states have led to concerns about profitability.

Insurers have mixed opinions about the risk adjustment program. While it aims to stabilize markets by redistributing funds from plans with healthier enrollees to those with sicker ones, some insurers criticize its complexity and argue it doesn’t always achieve fairness in payments.