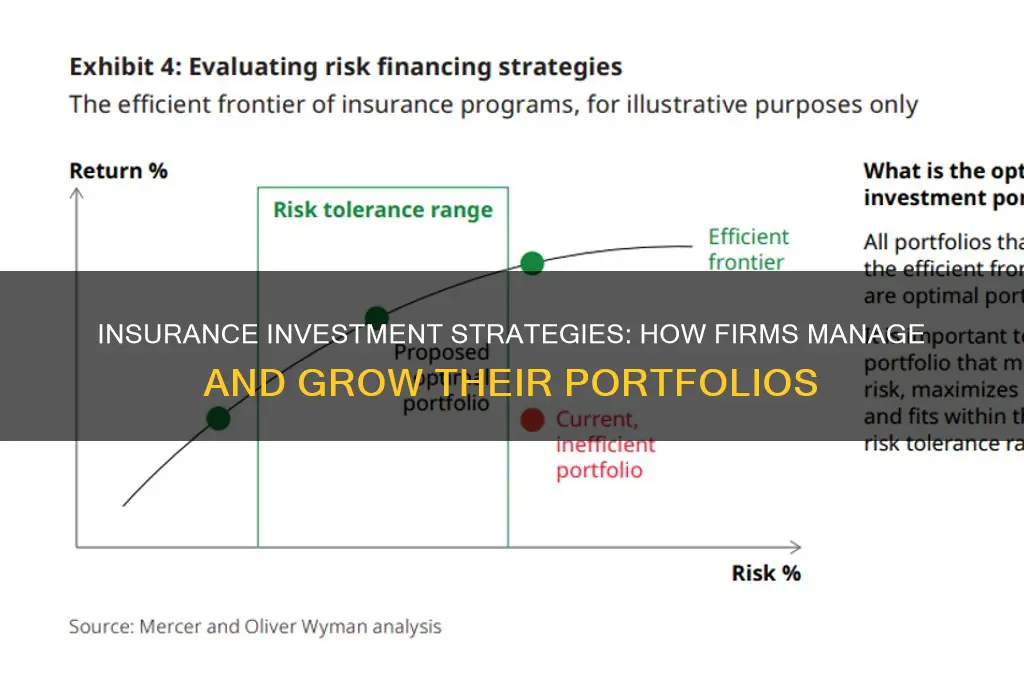

Insurance firms conduct their investment activities with a primary focus on balancing risk and return to ensure long-term financial stability and meet policyholder obligations. Given their unique liability structure, insurers prioritize investments in fixed-income securities, such as government bonds and high-grade corporate debt, which offer predictable cash flows and lower volatility. However, to enhance yields and diversify portfolios, they also allocate capital to equities, real estate, and alternative investments like private equity or infrastructure projects. Investment decisions are guided by regulatory requirements, liquidity needs, and risk management frameworks, often leveraging sophisticated modeling and asset-liability management techniques to align investments with future payout obligations. Additionally, insurers increasingly consider environmental, social, and governance (ESG) factors to mitigate risks and align with broader sustainability goals, reflecting their role as long-term stewards of capital.

Explore related products

What You'll Learn

![]()

Asset Allocation Strategies

Insurance firms, as long-term investors with unique liabilities, approach asset allocation with a precision that balances risk and return. Unlike individual investors, they must align their portfolios with future claims payouts, regulatory requirements, and capital preservation needs. This demands a strategic, data-driven approach to asset allocation, often involving sophisticated models and a focus on diversification across asset classes.

Asset allocation for insurers isn't a one-size-fits-all solution. It's a dynamic process that considers factors like policy duration, liability cash flows, and risk appetite. For instance, life insurers with long-term liabilities might tilt towards equities for growth, while property and casualty insurers with shorter-term claims may favor fixed-income securities for stability.

A key strategy employed by insurers is liability-driven investment (LDI). This approach prioritizes matching the duration and cash flow characteristics of assets to those of liabilities. Imagine a pension fund insurer: they'd invest heavily in long-term bonds with maturities mirroring their pension payout obligations, ensuring they have the funds available when needed. This minimizes the risk of being unable to meet future claims due to asset-liability mismatches.

Beyond traditional asset classes, insurers are increasingly exploring alternative investments like private equity, real estate, and infrastructure. These assets offer potentially higher returns and diversification benefits, mitigating the impact of market volatility on their portfolios. However, they also come with higher risk and liquidity concerns, requiring careful due diligence and risk management frameworks.

The regulatory landscape significantly influences asset allocation decisions. Solvency II in Europe, for example, imposes capital requirements based on the riskiness of an insurer's portfolio. This encourages insurers to hold more capital against riskier assets, potentially leading to a greater allocation to lower-risk, but lower-yielding, investments. Striking a balance between regulatory compliance and achieving investment objectives is a constant challenge for insurers.

Ultimately, successful asset allocation for insurance firms hinges on a deep understanding of their unique liabilities, a robust risk management framework, and the ability to adapt to changing market conditions and regulatory requirements. It's a complex, ongoing process that requires expertise, discipline, and a long-term perspective.

Canceling Sun Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Risk Management Frameworks

Insurance firms, by their very nature, are risk managers. This expertise extends beyond underwriting policies to their investment activities, where a robust risk management framework is critical. Such frameworks are not one-size-fits-all; they are tailored to the firm's risk appetite, asset allocation strategy, and regulatory environment.

A cornerstone of these frameworks is stress testing. This involves simulating extreme but plausible scenarios, such as a market crash or a surge in inflation, to assess the portfolio's resilience. For instance, an insurer might model the impact of a 20% decline in equity markets on its equity holdings, considering factors like duration, credit quality, and liquidity. The results inform capital adequacy, hedging strategies, and asset rebalancing decisions.

Another crucial element is scenario analysis, which goes beyond stress testing by exploring a range of potential outcomes, both positive and negative. This helps insurers understand the potential range of returns and risks associated with different investment strategies. For example, an insurer might analyze how changes in interest rates could affect the value of its bond portfolio, considering both the immediate impact and the longer-term effects on cash flows and reinvestment opportunities.

By integrating stress testing and scenario analysis, insurers can develop a dynamic risk management framework that adapts to changing market conditions. This proactive approach allows them to identify vulnerabilities, optimize their portfolios, and ultimately protect policyholder funds while pursuing sustainable investment returns.

Effective risk management frameworks also incorporate robust governance structures. This includes establishing clear roles and responsibilities for risk management functions, ensuring independent oversight, and fostering a culture of risk awareness throughout the organization. Regular risk reporting and transparent communication are essential to keep stakeholders informed and enable timely decision-making.

Furthermore, insurers are increasingly leveraging technology to enhance their risk management capabilities. Advanced analytics, machine learning algorithms, and data visualization tools enable them to process vast amounts of data, identify emerging risks, and make more informed investment decisions. For instance, natural language processing can be used to analyze news sentiment and its potential impact on specific asset classes.

In conclusion, risk management frameworks are the backbone of insurance firms' investment activities. By combining stress testing, scenario analysis, robust governance, and technological advancements, insurers can navigate the complexities of the investment landscape, protect policyholder funds, and achieve their long-term financial objectives.

Can You Transfer Your Epic Pass with Insurance Coverage?

You may want to see also

Explore related products

![]()

Regulatory Compliance Requirements

Insurance firms must navigate a complex web of regulatory compliance requirements when conducting investment activities, ensuring alignment with legal standards while pursuing financial growth. These requirements vary by jurisdiction but universally aim to protect policyholders, maintain market stability, and prevent systemic risks. For instance, in the United States, insurers are subject to state-specific regulations under the National Association of Insurance Commissioners (NAIC), while in the European Union, the Solvency II directive sets capital adequacy and risk management standards. Compliance is not optional; failure to adhere can result in severe penalties, reputational damage, and operational disruptions.

One critical aspect of regulatory compliance is the investment concentration limits imposed on insurers. These limits restrict the proportion of assets that can be allocated to specific asset classes, sectors, or individual securities. For example, many jurisdictions cap investments in a single issuer’s bonds or equities to 5% of the insurer’s total admitted assets. Such limits mitigate concentration risk, ensuring that a single investment’s failure does not jeopardize the insurer’s solvency. Insurers must continuously monitor their portfolios to remain within these thresholds, often leveraging technology to automate compliance checks.

Another key compliance requirement is the maintenance of sufficient capital to cover potential investment losses. Regulatory frameworks like Solvency II mandate insurers to hold capital commensurate with the risk profile of their investment portfolios. This involves calculating risk-based capital requirements using standardized formulas or internal models approved by regulators. For instance, investments in equities typically attract higher capital charges than government bonds due to their greater volatility. Insurers must strike a balance between maximizing returns and maintaining adequate capital buffers, a task that requires sophisticated risk modeling and strategic asset allocation.

Transparency and reporting are also central to regulatory compliance. Insurers are required to disclose their investment strategies, risk management practices, and financial performance to regulators and, in some cases, the public. Quarterly or annual filings, such as the Schedule D in the U.S. or the Solvency and Financial Condition Report (SFCR) in the EU, provide detailed insights into an insurer’s investment activities. These reports must be accurate and timely, necessitating robust internal controls and audit processes. Non-compliance with reporting requirements can lead to regulatory scrutiny and enforcement actions.

Finally, insurers must stay abreast of evolving regulatory landscapes, as new rules and guidelines are frequently introduced in response to market developments and emerging risks. For example, the growing focus on environmental, social, and governance (ESG) factors has led regulators to incorporate sustainability considerations into investment compliance frameworks. Insurers are increasingly required to assess and disclose the ESG risks associated with their portfolios, aligning their investment practices with broader societal goals. Proactive engagement with regulatory changes, coupled with a commitment to ethical investing, positions insurers to meet compliance requirements while contributing to sustainable economic growth.

Borrowing from Military Life Insurance: Is It Possible?

You may want to see also

Explore related products

![]()

Portfolio Diversification Techniques

Insurance firms, as long-term investors with significant liabilities, must balance risk and return to ensure financial stability. Portfolio diversification is a cornerstone of their investment strategy, aiming to minimize risk without sacrificing potential gains. One key technique is asset class diversification, where insurers allocate capital across equities, bonds, real estate, and alternative investments like private equity or infrastructure. For instance, a large insurer might allocate 40% to fixed income for stability, 30% to equities for growth, and the remaining 30% to alternatives and real estate for diversification and inflation hedging. This approach ensures that poor performance in one asset class doesn’t disproportionately impact the overall portfolio.

Another critical diversification technique is geographic allocation, spreading investments across regions to mitigate country-specific risks. Insurers often invest in developed markets like the U.S. and Europe for stability, while allocating a smaller portion to emerging markets for higher growth potential. For example, a global insurer might allocate 60% to North America and Europe, 20% to Asia, and 10% to Latin America and Africa. This strategy reduces exposure to regional economic downturns, currency fluctuations, and geopolitical risks, ensuring a more resilient portfolio.

Duration diversification is particularly vital for insurers due to their long-term liabilities. By investing in bonds with varying maturities, insurers can manage interest rate risk effectively. A typical approach is to hold a mix of short-term, intermediate, and long-term bonds. For instance, 40% of the fixed-income portfolio might be in short-term bonds (1–3 years), 40% in intermediate bonds (5–10 years), and 20% in long-term bonds (20+ years). This ensures liquidity for near-term obligations while capturing higher yields from longer-duration assets.

Finally, sector diversification within equity holdings helps insurers avoid overexposure to volatile industries. For example, instead of concentrating on technology or financials, insurers might allocate 20% to healthcare, 15% to consumer staples, and 10% to utilities—sectors known for stability and consistent dividends. This approach reduces the impact of sector-specific shocks, such as regulatory changes or economic cycles, on the overall portfolio.

In practice, insurers often use quantitative models to optimize diversification, balancing risk-adjusted returns with regulatory constraints. For instance, Solvency II in Europe requires insurers to maintain sufficient capital against investment risks, influencing asset allocation decisions. By combining these techniques, insurers create robust portfolios capable of weathering market volatility while meeting long-term obligations. The takeaway? Diversification isn’t just about spreading investments—it’s a strategic, data-driven process tailored to an insurer’s unique risk profile and liabilities.

Life Insurance and Chewing Tobacco: What's the Verdict?

You may want to see also

Explore related products

![]()

Long-Term Investment Horizons

Insurance firms, by their very nature, are stewards of long-term financial security. This inherent characteristic shapes their investment approach, favoring strategies that prioritize stability and sustained growth over short-term gains. Long-term investment horizons, typically spanning decades, are a cornerstone of their portfolio construction.

Unlike hedge funds or day traders, insurance companies aren't chasing quick profits. Their primary obligation is to meet future policyholder claims, which can materialize years or even decades after premiums are paid. This necessitates a patient, disciplined approach, focusing on assets that appreciate steadily over time, weathering market fluctuations.

Consider the case of life insurance. A 20-year policy requires the insurer to hold assets capable of generating sufficient returns to cover the payout upon maturity, even if the policyholder lives a full, healthy life. This demands investments in assets like government bonds, blue-chip stocks, and real estate, known for their relative stability and long-term growth potential.

While these assets may not offer the explosive returns of riskier ventures, they provide the predictability and security essential for fulfilling long-term obligations. Think of it as a marathon, not a sprint. Insurance firms aren't aiming for the fastest lap time; they're focused on completing the entire race, ensuring they have the resources to cross the finish line when needed.

This long-term perspective allows insurers to capitalize on compounding returns, a powerful force that exponentially increases wealth over time. By reinvesting dividends and interest earned, insurers can significantly grow their portfolios, ensuring they can meet future liabilities even in the face of inflation and economic downturns.

However, long-term investing isn't without its challenges. Market volatility, changing interest rates, and unforeseen economic events can disrupt even the most carefully crafted strategies. Insurers must constantly monitor their portfolios, rebalancing asset allocations and adjusting strategies to adapt to evolving market conditions while staying true to their long-term objectives.

In essence, long-term investment horizons are not just a preference for insurance firms; they are a necessity. This approach, characterized by patience, discipline, and a focus on stability, allows them to fulfill their core mission: providing financial security and peace of mind to policyholders, today and for generations to come.

Gerber Life Insurance Cash Value: Why So Low?

You may want to see also

Frequently asked questions

Insurance firms allocate funds based on risk tolerance, regulatory requirements, and long-term financial goals. They diversify investments across asset classes like bonds, stocks, real estate, and alternative investments to balance risk and return.

ALM ensures that insurance firms match their investment strategies with their liabilities (e.g., policy payouts). It helps manage interest rate risk, liquidity, and solvency to meet obligations over time.

Yes, insurance firms invest policyholder premiums after setting aside reserves for claims and operational costs. These investments generate returns to cover future liabilities and grow the firm’s assets.

Insurance firms use hedging, diversification, and stress testing to mitigate risks. They also adhere to regulatory guidelines and maintain capital buffers to absorb potential losses.

Insurance firms typically favor fixed-income securities like government and corporate bonds due to their stability and predictable cash flows. They also invest in equities, real estate, and infrastructure for higher returns.