Insurance, while intended to mitigate the financial burden of healthcare, often exacerbates affordability issues due to its complex and profit-driven structure. High premiums, deductibles, and copays force individuals to pay significant out-of-pocket costs, even with coverage. Additionally, insurance companies negotiate discounted rates with healthcare providers, incentivizing providers to inflate list prices, which further drives up overall healthcare costs. The administrative overhead of managing insurance claims adds billions in unnecessary expenses, while restrictive networks limit patient choice and competition. Moreover, the focus on maximizing profits leads insurers to deny or delay necessary treatments, leaving patients vulnerable to financial strain. These factors collectively contribute to a system where insurance, rather than making healthcare accessible, often renders it unaffordable for many.

| Characteristics | Values |

|---|---|

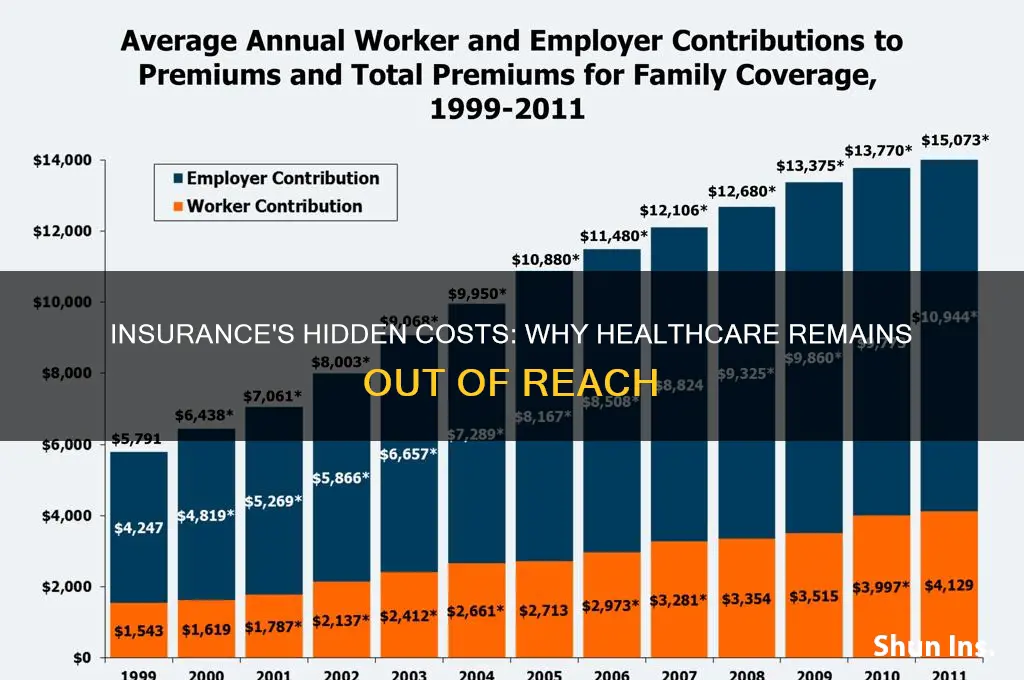

| High Premiums | Average annual premiums for employer-sponsored health insurance in the U.S. reached $7,739 for single coverage and $22,221 for family coverage in 2023 (Kaiser Family Foundation). |

| Rising Deductibles | Average deductibles for individual plans increased to $1,760 in 2023, up from $1,669 in 2022, making out-of-pocket costs prohibitive before insurance kicks in (HealthPocket). |

| Narrow Networks | Insurance plans often limit access to specific providers, forcing patients to pay higher out-of-network costs or switch doctors, reducing affordability and choice. |

| Administrative Costs | U.S. healthcare spends 8% of total costs on administrative expenses, compared to 1-3% in other countries, driving up premiums (Journal of the American Medical Association, 2022). |

| Price Opacity | Lack of transparent pricing for medical services and procedures makes it difficult for patients to compare costs, leading to unexpected bills. |

| Prior Authorization | Insurers require prior authorization for many treatments, delaying care and increasing administrative burdens on providers, which can raise costs. |

| Profit Margins | Health insurance companies prioritize profit, with the top five U.S. insurers reporting combined profits of $48 billion in 2022 (Statista). |

| Fragmented System | Multiple payers and plans create inefficiencies, duplicating administrative processes and increasing overall system costs. |

| Cost-Shifting | Providers charge insured patients more to offset losses from treating uninsured or underinsured individuals, inflating costs for those with insurance. |

| Lack of Price Negotiation | Insurers often fail to negotiate lower drug and service prices effectively, passing higher costs onto consumers. |

Explore related products

What You'll Learn

- High premiums reduce disposable income, limiting access to essential healthcare services for many individuals

- Insurance bureaucracy increases administrative costs, driving up overall healthcare expenses significantly

- Narrow networks restrict provider choices, forcing patients into costlier out-of-network care options

- Profit-driven models prioritize shareholder returns over patient affordability, inflating healthcare prices

- Complex billing systems lead to unexpected costs, making healthcare financially unpredictable for consumers

![]()

High premiums reduce disposable income, limiting access to essential healthcare services for many individuals

The relentless rise in insurance premiums has become a silent thief, siphoning away disposable income from households across the nation. For a family of four earning the median income, a 20% increase in premiums over five years translates to roughly $6,000 less annually for groceries, education, or emergencies. This financial strain forces difficult choices: pay the premium or risk going uninsured. When premiums consume a larger share of income, the ability to afford even basic healthcare services—like preventive check-ups or prescription medications—dwindles. For instance, a diabetic patient might skip insulin doses to save money, leading to complications that cost far more in the long run.

Consider the mechanics of this dilemma. Premiums are not just numbers on a bill; they represent a trade-off between financial stability and health security. A single parent earning $40,000 annually might face premiums of $500 monthly, leaving little room for copays, deductibles, or out-of-pocket expenses. This creates a paradox: insurance is meant to protect against catastrophic costs, but its very cost becomes a barrier to accessing care. For low-income individuals, this often means delaying treatment until conditions worsen, turning manageable issues into medical crises.

To mitigate this, individuals can take proactive steps. First, explore high-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs). While HDHPs have lower premiums, they require careful budgeting for potential out-of-pocket costs. Second, leverage employer-sponsored wellness programs, which often offer discounts on premiums for healthy behaviors like regular exercise or smoking cessation. Third, compare plans annually during open enrollment, as premiums and coverage can change significantly year-to-year. Tools like Healthcare.gov or state marketplaces provide side-by-side comparisons to find the best value.

However, systemic solutions are equally critical. Policymakers must address the root causes of premium inflation, such as administrative bloat and drug pricing. For example, capping administrative costs at 15% of premiums, as some states have done, could redirect funds toward patient care. Additionally, expanding Medicaid and subsidizing premiums for low-income families would ensure that insurance remains a tool for access, not exclusion. Until then, individuals must navigate this complex landscape with vigilance, balancing the need for coverage against the reality of shrinking disposable income.

Does Insurance Roadside Assistance Charge? Understanding Costs and Coverage

You may want to see also

Explore related products

$8.99 $17.99

![]()

Insurance bureaucracy increases administrative costs, driving up overall healthcare expenses significantly

The labyrinthine bureaucracy of insurance systems imposes staggering administrative burdens on healthcare providers, diverting resources from patient care to paperwork. Consider this: physicians in the U.S. spend nearly 8.7 hours per week navigating insurance-related tasks, from prior authorizations to claims disputes. This equates to roughly 21% of their workweek, time that could otherwise be allocated to treating patients. For a primary care physician seeing 20 patients daily, this translates to 4 fewer patients each week, exacerbating access issues. Multiply this across thousands of providers, and the system-wide inefficiency becomes clear.

To illustrate, a 2022 study by the American Medical Association found that hospitals dedicate $10 billion annually to billing and insurance-related (BIR) costs alone. These expenses include staffing for coding specialists, compliance officers, and software to manage insurer requirements. For context, this $10 billion could fund 1.2 million hip replacements or 3.5 million MRI scans at average Medicare reimbursement rates. Instead, it vanishes into administrative overhead, inflating the cost of care without improving health outcomes.

Contrast this with single-payer systems, where administrative costs are a fraction of those in the U.S. Canada, for instance, spends 2.4% of its healthcare budget on administration, compared to 8% in the U.S. This disparity underscores how insurance bureaucracy acts as a hidden tax on healthcare. Providers pass these costs onto patients through higher fees, while insurers justify premium increases by pointing to complex regulatory compliance. The result? A vicious cycle where administrative bloat drives up prices, making care less affordable for everyone.

Practical solutions exist, but they require systemic change. Streamlining prior authorization processes, standardizing billing codes, and adopting interoperable electronic health records (EHRs) could slash administrative waste. For example, automating prior authorizations—which currently take 13.1 hours weekly per physician—could free up $2,075 per provider per week, funds that could offset rising drug costs or expand preventive services. Policymakers and insurers must prioritize such reforms to curb the bureaucratic drag on affordability.

Ultimately, the administrative costs of insurance bureaucracy are not an inevitable feature of healthcare but a policy choice. Every dollar spent on redundant paperwork is a dollar diverted from patient care, innovation, or cost reduction. Until stakeholders dismantle this inefficiency, insurance will remain a driver of unaffordability, not a solution to it. The path forward is clear: simplify, standardize, and refocus resources on what matters—delivering care, not processing claims.

Life Insurance Overfunding: Risks and Rewards

You may want to see also

Explore related products

![]()

Narrow networks restrict provider choices, forcing patients into costlier out-of-network care options

Narrow provider networks, a common feature of many health insurance plans, often leave patients with limited choices when it comes to selecting healthcare providers. These networks dictate which doctors, hospitals, and specialists are considered "in-network," and receiving care from out-of-network providers can result in significantly higher out-of-pocket costs for the patient. For instance, a study by the Kaiser Family Foundation found that out-of-network emergency room visits can cost patients up to 300% more than in-network visits, even when the facility is within the same geographical area.

Consider a scenario where a patient requires specialized care for a chronic condition, such as diabetes management. If their insurance plan’s narrow network excludes the endocrinologist they’ve been seeing for years, they face a difficult choice: switch to an in-network provider who may not have the same expertise or continue with their trusted specialist and incur substantial out-of-network fees. For a 45-year-old patient on a high-deductible plan, this could mean paying $500 per visit instead of the $100 in-network copay, plus a higher coinsurance rate. Over time, these additional costs can make essential care unaffordable, leading to delayed treatment or skipped appointments.

The problem intensifies in rural or underserved areas, where narrow networks may leave patients with no in-network options for critical services. For example, a patient in a rural community might need to travel hours to see an in-network oncologist, while a closer, out-of-network provider is available but financially out of reach. This not only increases direct costs but also imposes indirect burdens, such as lost wages from time off work and transportation expenses. A practical tip for patients in such situations is to request a network adequacy review from their state insurance commissioner, which can sometimes lead to exceptions or expanded network coverage.

Insurance companies argue that narrow networks help keep premiums lower by negotiating discounted rates with a select group of providers. However, this cost-saving measure often shifts the financial burden onto patients, particularly those with complex or ongoing healthcare needs. To mitigate this, patients should carefully review their plan’s provider directory before enrolling, verify that their preferred doctors are in-network, and consider using telehealth services when available, as these are often covered at in-network rates even if the provider is geographically distant.

Ultimately, narrow networks exemplify how insurance structures can inadvertently make healthcare unaffordable by restricting access to affordable care. While these networks may reduce premiums for some, they disproportionately harm patients who require specialized or consistent care. Policymakers and insurers must balance cost containment with patient choice to ensure that insurance plans provide meaningful, affordable access to healthcare rather than forcing patients into costly out-of-network situations.

Calculating Damages: Subtracting Insurance Claims Made Simple

You may want to see also

Explore related products

![]()

Profit-driven models prioritize shareholder returns over patient affordability, inflating healthcare prices

The relentless pursuit of profit in healthcare has created a system where the financial interests of shareholders often overshadow the needs of patients. Consider this: in 2022, the top five U.S. health insurance companies reported combined profits of over $40 billion. Meanwhile, nearly 10% of Americans remain uninsured, and medical debt is the leading cause of bankruptcy. This disparity highlights a fundamental issue: profit-driven models prioritize shareholder returns over patient affordability, driving healthcare prices to unsustainable levels.

To understand how this happens, examine the mechanics of insurance company operations. Insurers negotiate rates with healthcare providers, often securing discounts in exchange for patient volume. However, these savings rarely translate to lower costs for consumers. Instead, insurers pocket the difference, funneling it into executive bonuses and shareholder dividends. For instance, a 2021 study found that for every dollar spent on healthcare, 25 cents goes to administrative costs and profits, rather than direct patient care. This inefficiency inflates prices, making even basic services unaffordable for many.

A comparative analysis of single-payer systems, such as those in Canada or the UK, reveals a stark contrast. In these models, healthcare is funded through taxation, eliminating the profit motive. As a result, administrative costs are significantly lower, and prices are more controlled. For example, a knee replacement in the U.S. costs an average of $30,000, compared to $7,000 in Canada. This price discrepancy underscores how profit-driven models distort the market, prioritizing financial gain over accessibility.

To mitigate the impact of profit-driven healthcare, patients can take proactive steps. First, scrutinize insurance plans for hidden costs, such as high deductibles or limited provider networks. Second, consider generic medications, which can cost up to 80% less than brand-name equivalents. For instance, a 30-day supply of generic Lipitor (atorvastatin) for cholesterol management costs around $10, compared to $180 for the brand version. Finally, advocate for policy changes that prioritize patient affordability, such as capping insurer profits or expanding public healthcare options. By demanding transparency and accountability, consumers can push back against a system that prioritizes profit over people.

Life Insurance: Protecting Your Loved Ones and Their Future

You may want to see also

Explore related products

![]()

Complex billing systems lead to unexpected costs, making healthcare financially unpredictable for consumers

The labyrinthine nature of healthcare billing systems often leaves patients bewildered, facing unexpected costs that can spiral into financial hardship. Consider a routine outpatient procedure: a patient might receive separate bills from the hospital, the surgeon, the anesthesiologist, and the lab, each with its own coding system and pricing structure. For instance, a 45-year-old patient undergoing a colonoscopy could be charged $1,200 for the facility fee, $800 for the physician’s services, and $300 for anesthesia, not to mention additional lab fees for biopsy analysis. Without clear communication or itemized breakdowns, these charges often come as a shock, making it nearly impossible for consumers to anticipate their financial liability.

To navigate this complexity, patients must adopt a proactive approach. Start by requesting a detailed estimate of all potential charges before any procedure, including facility fees, physician fees, and ancillary services. For example, if prescribed a 30-day course of a specialty medication, ask for both the brand and generic pricing options, as well as whether prior authorization is required by your insurer. Additionally, verify in-network status for all providers involved—a surprise out-of-network charge can double or triple expected costs. Tools like healthcare price transparency websites or insurer cost estimators can provide benchmarks, but always confirm directly with the provider to avoid discrepancies.

The unpredictability of healthcare costs is exacerbated by insurance policies that shift more financial risk onto consumers. High-deductible plans, now covering over 50% of insured Americans, require patients to pay thousands out-of-pocket before coverage kicks in. For a family on a $50,000 annual income, a $4,000 deductible can represent nearly a month’s wages. When combined with opaque billing practices, this creates a perfect storm: patients delay care to avoid unforeseen expenses, leading to worse health outcomes and higher long-term costs. A study by the Journal of the American Medical Association found that 40% of patients with chronic conditions skipped medications or appointments due to cost concerns, highlighting the systemic impact of financial unpredictability.

To mitigate these risks, advocate for yourself by scrutinizing every bill for errors—up to 80% of medical invoices contain mistakes, such as duplicate charges or incorrect procedure codes. For instance, a patient billed for 10 physical therapy sessions when only 8 were attended can dispute the discrepancy with documentation. Keep a record of all communications, including dates, names, and outcomes, to build a case if needed. If overwhelmed, consider hiring a medical billing advocate, whose fees (typically $50–$150 per hour) can be offset by savings from corrected bills. While these steps require time and effort, they are essential to reclaiming control over healthcare finances in a system designed to obfuscate costs.

Longview, TX: Get Comprehensive Insurance Coverage for Peace of Mind

You may want to see also

Frequently asked questions

Insurance companies often negotiate higher rates with healthcare providers, knowing they can pass the costs onto policyholders through premiums, deductibles, and copays. This dynamic drives up overall healthcare expenses, making it less affordable for individuals and families.

High insurance premiums reduce disposable income, leaving individuals with less money to cover other essential expenses. Additionally, even with insurance, out-of-pocket costs like deductibles and copays can be prohibitively expensive, making healthcare inaccessible for many.

The complexity of insurance plans, including varying coverage limits, exclusions, and networks, often results in unexpected costs for patients. This lack of transparency makes it difficult for individuals to predict healthcare expenses, contributing to financial strain and unaffordability.