The United States is one of the most insured nations globally, with a complex and multifaceted insurance landscape that spans health, auto, property, and life coverage. While millions of Americans rely on insurance for financial protection, the level of coverage varies significantly across demographics, regions, and policy types. Health insurance, for instance, remains a contentious issue, with approximately 91% of the population insured as of 2023, yet gaps persist due to affordability and accessibility challenges. Auto and homeowners insurance are widely held but often mandated by law or lenders, while life insurance coverage is less universal, with only about 54% of adults having a policy. Despite its high insurance penetration, the U.S. faces ongoing debates about affordability, regulatory disparities, and the adequacy of coverage in addressing unforeseen risks, highlighting both the strengths and limitations of its insurance system.

Explore related products

What You'll Learn

![]()

Health Insurance Coverage Rates

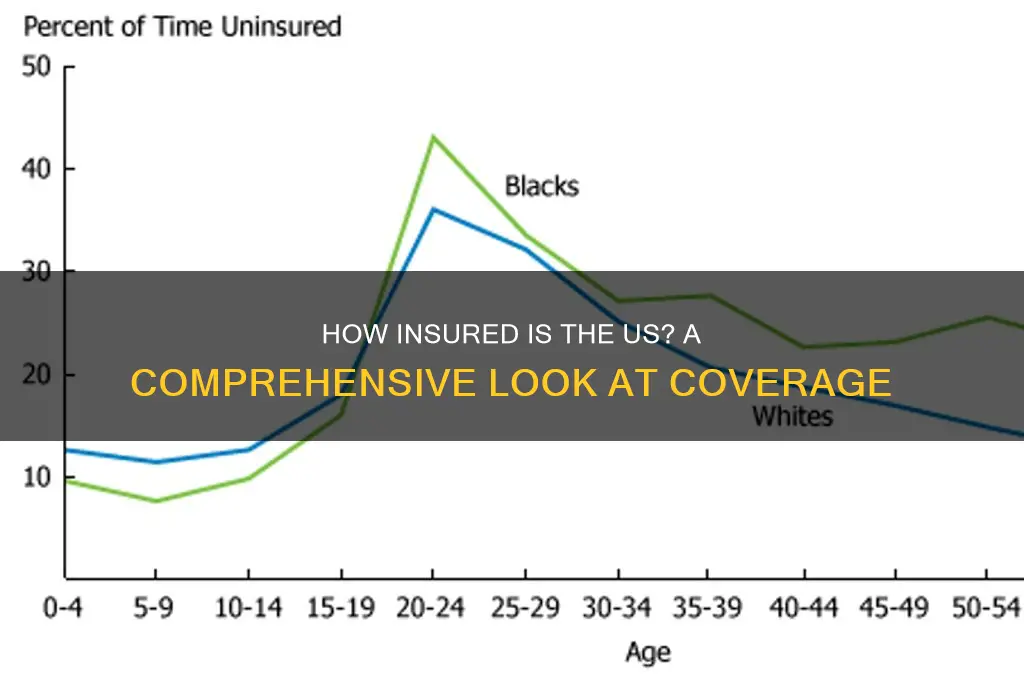

The United States has seen significant fluctuations in health insurance coverage rates over the past decade, influenced by policy changes, economic shifts, and public health crises. As of 2023, approximately 91% of Americans have some form of health insurance, a notable increase from 84% in 2013. This improvement is largely attributed to the Affordable Care Act (ACA), which expanded Medicaid eligibility and established health insurance marketplaces. However, disparities persist: while 95% of children are insured, only 88% of working-age adults have coverage. Understanding these trends is crucial for addressing gaps and ensuring equitable access to healthcare.

Analyzing the data reveals that employer-sponsored insurance remains the primary source of coverage, covering about 54% of the population. Medicaid and Medicare collectively insure another 36%, with individual market plans and other programs covering the remainder. Despite these numbers, approximately 25 million Americans remain uninsured, often due to affordability issues or ineligibility for public programs. For instance, in states that have not expanded Medicaid, many low-income adults fall into the "coverage gap," earning too much for Medicaid but too little to afford private insurance. This highlights the need for targeted policy interventions to close these gaps.

To improve coverage rates, individuals should explore all available options, including employer plans, ACA marketplaces, and public programs like Medicaid and CHIP. For those under 30 or facing financial hardship, catastrophic health plans offer a low-cost alternative, though they come with higher deductibles. Additionally, open enrollment periods (typically November 1 to January 15) are critical times to review and update coverage. Outside these periods, qualifying life events—such as marriage, birth of a child, or loss of job-based insurance—allow for special enrollment. Staying informed about policy changes and eligibility criteria can maximize access to affordable coverage.

Comparing the U.S. to other high-income countries underscores its unique challenges. Nations with universal healthcare systems, like Canada and the UK, achieve near-universal coverage with lower per capita costs. In contrast, the U.S. relies on a fragmented mix of public and private insurance, leading to higher administrative costs and uneven access. While the ACA has narrowed disparities, the U.S. still lags in covering its entire population. Learning from international models could inspire reforms to streamline coverage and reduce costs, though such changes would require significant political and systemic shifts.

Ultimately, addressing health insurance coverage rates in the U.S. demands a multi-faceted approach. Policymakers must expand Medicaid in non-expansion states, increase subsidies for marketplace plans, and address affordability barriers. Employers can play a role by offering more comprehensive benefits, while individuals must stay proactive in seeking and maintaining coverage. By combining these efforts, the nation can move closer to ensuring that all Americans have access to the healthcare they need.

Uber Drivers: Bonded and Insured?

You may want to see also

Explore related products

![]()

Auto Insurance Mandates by State

In the United States, auto insurance requirements vary significantly from state to state, creating a patchwork of mandates that drivers must navigate. While some states enforce strict liability coverage limits, others adopt a more lenient approach, allowing drivers to opt for minimal or even no insurance. For instance, New Hampshire stands out as the only state that doesn’t require drivers to carry auto insurance, though it mandates proof of financial responsibility to cover accident costs. In contrast, states like Maine and Alaska impose higher liability limits, reflecting their emphasis on protecting drivers and pedestrians alike. Understanding these differences is crucial for drivers moving across state lines or seeking comprehensive coverage beyond the legal minimum.

Analyzing these mandates reveals a clear divide between "tort" and "no-fault" states, which directly impacts insurance requirements. In no-fault states like Michigan and New York, drivers are required to carry Personal Injury Protection (PIP) coverage, ensuring medical expenses are paid regardless of fault. This system aims to reduce litigation but often results in higher premiums. Tort states, such as California and Texas, allow drivers to sue for damages, leading to lower mandatory coverage limits but potentially higher out-of-pocket costs in accidents. This distinction highlights how state policies shape not only insurance costs but also the legal landscape for drivers involved in accidents.

For drivers, navigating these mandates requires a proactive approach. Start by verifying your state’s minimum liability requirements, typically expressed in a 25/50/25 format (e.g., $25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage). However, consider purchasing coverage beyond the minimum, especially if you own a newer vehicle or have significant assets. For example, adding collision and comprehensive coverage can protect against theft, vandalism, and accidents, regardless of fault. Additionally, uninsured/underinsured motorist coverage is essential in states with high rates of uninsured drivers, such as Florida and Michigan, where nearly 20% of drivers lack insurance.

A comparative look at penalties for non-compliance underscores the importance of adhering to state mandates. In California, driving without insurance can result in fines up to $1,000 and vehicle impoundment, while in Tennessee, fines start at $300 but escalate with repeated offenses. Some states, like New Jersey, impose harsher penalties, including license suspension and community service. These variations emphasize the need for drivers to stay informed and compliant, as the consequences extend beyond financial penalties to include long-term impacts on driving privileges and insurance rates.

Ultimately, auto insurance mandates by state reflect a balance between protecting the public and providing drivers with affordable options. While compliance with state laws is non-negotiable, drivers should view these mandates as a starting point rather than an endpoint. By assessing personal risk factors, such as vehicle value, driving habits, and financial stability, individuals can tailor their coverage to provide adequate protection. In a nation where auto insurance is both a legal requirement and a financial safeguard, understanding and exceeding state mandates ensures peace of mind on the road.

Is Motorcycle Insurance Required in Florida? Essential Coverage Explained

You may want to see also

Explore related products

![]()

Homeowners Insurance Penetration Levels

Homeowners insurance penetration in the U.S. varies significantly by state, with rates ranging from 38% in North Dakota to 82% in Florida, according to the Insurance Information Institute. This disparity highlights the influence of regional factors such as natural disaster risk, state regulations, and local housing markets. For instance, Florida’s high penetration is driven by its vulnerability to hurricanes, while North Dakota’s lower rate may reflect its lower risk of catastrophic events and more affordable housing costs. Understanding these regional differences is critical for policymakers and insurers aiming to improve coverage equity.

Analyzing the data reveals a clear correlation between disaster-prone areas and higher insurance penetration. States along the Gulf Coast and Atlantic seaboard, where hurricanes and flooding are common, consistently show higher rates of homeowners insurance adoption. Conversely, states in the Midwest and Great Plains, with lower risks of severe weather, tend to have lower penetration. This trend underscores the role of perceived risk in consumer behavior, as homeowners in high-risk areas are more likely to invest in protection. However, it also raises concerns about underinsured populations in areas where disasters, though rare, can still be devastating.

To increase penetration in underinsured regions, insurers and policymakers can adopt targeted strategies. For example, offering bundled policies that combine homeowners and flood insurance can simplify the purchasing process and reduce costs for consumers. Public awareness campaigns can educate homeowners about the risks they face and the long-term financial benefits of insurance. Additionally, state governments can incentivize coverage by providing subsidies or tax breaks for policyholders in high-risk areas. These measures, when tailored to local needs, can help bridge the gap in penetration levels across the country.

A comparative analysis of international homeowners insurance penetration rates provides further context. In countries like the UK and Canada, penetration is nearly universal, often due to stricter lending requirements that mandate insurance for mortgaged properties. The U.S., by contrast, relies on voluntary adoption, which contributes to its lower overall penetration. While this approach aligns with American preferences for individual choice, it also leaves millions of homeowners vulnerable to financial ruin in the event of a disaster. Balancing personal freedom with collective risk mitigation remains a key challenge in improving U.S. homeowners insurance penetration.

Finally, technological advancements offer promising solutions to enhance penetration levels. Insurtech companies are leveraging data analytics and AI to assess risk more accurately, enabling them to offer customized policies at competitive prices. Digital platforms streamline the purchasing process, making it easier for homeowners to compare options and buy coverage. For example, tools that integrate property data with local risk factors can provide instant quotes tailored to individual needs. By embracing these innovations, the insurance industry can make coverage more accessible and appealing to a broader segment of the population.

Decoding Marketplace Insurance TrackID SP-006: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Life Insurance Ownership Statistics

Life insurance ownership in the U.S. is surprisingly low, with only about 54% of Americans having any form of coverage. This statistic, from the 2023 Insurance Barometer Study by LIMRA and Life Happens, reveals a significant protection gap. Despite life insurance being a critical financial safety net, nearly half of the population remains uninsured. This gap is particularly concerning given that life insurance is designed to provide financial security to dependents in the event of the policyholder’s death, covering expenses like mortgages, debts, and daily living costs.

Breaking down the data by age group highlights stark disparities. Millennials, aged 25 to 40, are the least insured generation, with only 41% owning life insurance. In contrast, Baby Boomers, aged 57 to 75, have the highest ownership rate at 60%. This generational divide may reflect differing financial priorities, with younger adults often prioritizing student loan repayment or homeownership over life insurance. However, it also underscores a missed opportunity for millennials to secure affordable coverage at a younger age, when premiums are lower.

The type of life insurance owned also varies widely. Term life insurance, which provides coverage for a specified period (typically 10 to 30 years), is the most common, accounting for 75% of policies. Permanent life insurance, such as whole life or universal life, which offers lifelong coverage and a cash value component, makes up the remaining 25%. While term life is more affordable and straightforward, permanent life insurance appeals to those seeking long-term financial planning tools. Understanding these preferences is crucial for insurers and consumers alike to tailor solutions effectively.

One alarming trend is the underinsurance of households. Among those with life insurance, 40% admit they do not have enough coverage to meet their needs. This often stems from underestimating future expenses or overestimating the cost of additional coverage. For example, a family with a $250,000 policy might find it insufficient to cover a $300,000 mortgage, childcare costs, and lost income over a decade. To address this, experts recommend calculating coverage needs based on 10–12 times annual income, plus outstanding debts and future expenses like college tuition.

Practical steps can help bridge the life insurance gap. First, educate yourself on the types of policies available and their benefits. Second, use online calculators to estimate your coverage needs accurately. Third, compare quotes from multiple insurers to find affordable options. Finally, consider starting with a term policy if budget constraints are a concern, with the option to convert to permanent coverage later. By taking these steps, individuals can ensure they are adequately protected, closing the gap between need and ownership in life insurance statistics.

Maximizing Life Insurance Benefits: Strategies to Minimize Estate Tax

You may want to see also

Explore related products

![]()

Employer-Sponsored Insurance Trends

Employer-sponsored insurance (ESI) remains the cornerstone of health coverage in the U.S., with approximately 158 million Americans relying on it as of 2023. This dominance, however, masks a shifting landscape. One notable trend is the rise of high-deductible health plans (HDHPs), which now account for over 50% of ESI offerings. These plans, paired with health savings accounts (HSAs), are marketed as cost-effective but often leave employees exposed to significant out-of-pocket expenses. For instance, the average deductible for a single-coverage HDHP reached $2,000 in 2023, a 5% increase from the previous year. While employers save on premiums, employees, particularly those in lower-wage jobs, face financial strain when accessing care.

Another emerging trend is the expansion of voluntary benefits within ESI packages. Employers are increasingly offering add-ons like telehealth services, mental health apps, and wellness programs to attract and retain talent. For example, 72% of large employers now include telehealth options, up from 50% in 2018. These benefits address gaps in traditional coverage but can create complexity for employees navigating multiple vendors and platforms. Employers must ensure these additions are seamlessly integrated into existing plans and communicate their value clearly to maximize utilization.

The shift toward value-based care is also influencing ESI trends. Employers are partnering with providers to implement bundled payment models and accountable care organizations (ACOs), aiming to improve outcomes while controlling costs. For instance, a 2022 study found that companies using ACOs saw a 3-5% reduction in healthcare spending compared to traditional fee-for-service models. However, this approach requires significant upfront investment and data infrastructure, limiting adoption among smaller employers.

Finally, the role of ESI in addressing health disparities is gaining attention. Data shows that employees in low-wage industries are less likely to have access to comprehensive ESI, exacerbating inequities. Some forward-thinking employers are responding by offering tiered plans or subsidies for lower-income workers. For example, a manufacturing company in the Midwest introduced a $0-premium plan for employees earning below $40,000 annually, resulting in a 20% increase in enrollment among this group. Such initiatives demonstrate how ESI can be a tool for equity, but broader policy changes are needed to ensure universal access.

In summary, while ESI remains the primary source of health coverage in the U.S., its evolution reflects broader trends in cost management, employee engagement, and equity. Employers must balance financial constraints with the need to provide meaningful benefits, leveraging innovations like HDHPs, voluntary benefits, and value-based care while addressing disparities. As the landscape continues to shift, proactive strategies will be essential to ensure ESI remains a viable solution for both employers and employees.

Is Building Insurance Mandatory? Understanding Your Coverage Requirements

You may want to see also

Frequently asked questions

As of recent data, approximately 91% of Americans have health insurance, with coverage provided through employer-sponsored plans, government programs like Medicare and Medicaid, or individual plans.

About 8-9% of the U.S. population remains uninsured, though this figure fluctuates based on economic conditions, policy changes, and access to affordable coverage.

Employer-sponsored health insurance is the most common type, covering roughly 55% of the insured population.

The U.S. has a higher percentage of uninsured individuals compared to most developed countries with universal healthcare systems, but it also has a mix of private and public insurance options.

The U.S. government offers insurance through programs like Medicare (for seniors), Medicaid (for low-income individuals), and the Children’s Health Insurance Program (CHIP).