The health insurance participation rate, a critical metric in assessing the accessibility and utilization of healthcare services, is determined through a multifaceted analysis of various factors. This rate reflects the proportion of individuals or households within a population who have enrolled in health insurance plans, either through private providers, government-sponsored programs, or employer-based schemes. Key determinants include demographic characteristics such as age, income, and employment status, as well as socioeconomic factors like education level and geographic location. Additionally, policy-related elements, such as the availability of affordable plans, government mandates, and public awareness campaigns, play a significant role in shaping participation rates. Understanding these factors is essential for policymakers, insurers, and healthcare providers to design effective strategies that enhance coverage and improve overall public health outcomes.

| Characteristics | Values |

|---|---|

| Definition | Percentage of individuals within a defined population who are enrolled in a health insurance plan. |

| Data Source | Primarily government surveys (e.g., US Census Bureau's Current Population Survey, American Community Survey), insurance company data, and national health statistics. |

| Population Covered | Varies by study/report, often includes total population, specific age groups, income brackets, or geographic regions. |

| Time Period | Typically measured annually, but can be quarterly or monthly depending on data availability. |

| Calculation | (Number of individuals with health insurance) / (Total population in the defined group) * 100 |

| Key Factors Influencing Rate | - Income and affordability - Employer-sponsored insurance availability - Government policies and subsidies - Individual mandate (where applicable) - Demographics (age, health status) - Cultural attitudes towards insurance |

| Latest Global Average (2021) | Approximately 68% (varies widely by country, with high-income countries generally having higher rates) |

| US Participation Rate (2022) | 91.4% (CDC data) |

| Trends | Generally increasing in countries with expanding healthcare coverage policies, but disparities persist across income levels and regions. |

Explore related products

What You'll Learn

- Demographic Factors: Age, income, employment status, and geographic location influence participation rates significantly

- Policy Costs: Premiums, deductibles, and out-of-pocket expenses directly impact enrollment decisions

- Employer Coverage: Availability of employer-sponsored plans is a key determinant of participation

- Government Policies: Subsidies, mandates, and public programs like Medicaid affect enrollment rates

- Awareness & Education: Knowledge of benefits and application processes boosts participation levels

![]()

Demographic Factors: Age, income, employment status, and geographic location influence participation rates significantly

Age is a critical determinant of health insurance participation rates, with distinct trends across different life stages. Young adults aged 18–25 often exhibit lower enrollment due to perceived good health and limited financial resources. Conversely, individuals over 65, eligible for Medicare in the U.S., show near-universal participation. Middle-aged adults (35–64) typically have higher rates due to increased health awareness and employer-sponsored plans. Policymakers can target younger demographics with affordable, tailored plans to boost participation, while ensuring seamless transitions to Medicare for older populations.

Income levels directly correlate with health insurance participation, creating a stark divide. Households earning below the federal poverty level (FPL) often face barriers like high premiums and out-of-pocket costs, despite subsidies like those under the Affordable Care Act. Conversely, households earning above 400% of the FPL are more likely to have employer-sponsored insurance or afford private plans. To bridge this gap, expanding Medicaid eligibility and enhancing premium tax credits can make coverage more accessible to low-income groups, thereby increasing participation rates.

Employment status is another pivotal factor, as job-based insurance remains the primary coverage source for most Americans. Full-time workers are significantly more likely to be insured than part-time or gig workers, who often lack employer-provided benefits. Unemployment rates inversely correlate with insurance participation, as job loss frequently results in coverage loss. Addressing this requires policies like COBRA subsidies or public insurance options for the unemployed, ensuring continuity of coverage during transitions.

Geographic location shapes participation rates through variations in state policies, healthcare infrastructure, and cost of living. States that expanded Medicaid under the ACA, such as California and New York, have higher insured rates compared to non-expansion states like Texas and Florida. Rural areas often face limited provider networks and higher uninsured rates, while urban centers benefit from greater access. Tailoring solutions to regional needs, such as incentivizing providers to serve rural areas or implementing state-specific subsidies, can mitigate these disparities and improve overall participation.

Auto Liability Insurance: Medical Expense Coverage Explained

You may want to see also

Explore related products

![]()

Policy Costs: Premiums, deductibles, and out-of-pocket expenses directly impact enrollment decisions

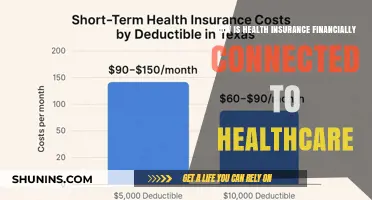

The cost of health insurance policies is a critical factor in determining participation rates, as individuals and families weigh the financial burden of premiums, deductibles, and out-of-pocket expenses against the perceived value of coverage. For instance, a study by the Kaiser Family Foundation found that employees are more likely to opt out of employer-sponsored insurance when their share of the premium exceeds 5% of their income. This threshold highlights the sensitivity of enrollment decisions to even modest increases in policy costs. When premiums rise, particularly in the individual market, potential enrollees may forgo coverage altogether, opting instead to pay the penalty or risk going uninsured.

Consider the interplay between premiums and deductibles. A policy with a lower monthly premium might seem attractive at first glance, but it often comes with a higher deductible—sometimes as high as $6,000 for an individual or $12,000 for a family under high-deductible plans. For a 30-year-old earning $40,000 annually, a $400 monthly premium paired with a $5,000 deductible could mean delaying necessary care until costs surpass that threshold, effectively rendering the insurance unusable for routine or minor health issues. Conversely, a plan with a $600 monthly premium and a $1,000 deductible might encourage timely medical visits, improving health outcomes but at a steeper upfront cost.

Out-of-pocket expenses, including copays and coinsurance, further complicate enrollment decisions. A family with chronic conditions, such as diabetes or asthma, must calculate not just the premium but also the cumulative cost of frequent doctor visits, prescriptions, and specialist referrals. For example, a plan with 20% coinsurance on hospital stays could result in a $5,000 bill for a three-day admission, even after meeting the deductible. Such unpredictability often leads to underinsurance, where individuals select plans with inadequate coverage to minimize monthly costs, only to face financial hardship during emergencies.

To optimize enrollment decisions, consumers should prioritize policies that align with their anticipated healthcare needs. For healthy individuals under 40, a high-deductible plan paired with a Health Savings Account (HSA) can reduce premiums while offering tax advantages. Conversely, families with children or older adults should consider plans with lower deductibles and comprehensive prescription coverage, even if premiums are higher. Tools like healthcare.gov’s plan comparison feature allow users to estimate annual costs based on expected services, providing a clearer picture of total expenses beyond the premium.

Ultimately, policy costs serve as both a barrier and an incentive to health insurance participation. Policymakers and insurers must balance affordability with comprehensiveness, ensuring that premiums, deductibles, and out-of-pocket costs do not deter enrollment while still maintaining financial sustainability. For consumers, understanding these cost components and their implications is essential to making informed decisions that protect both health and financial well-being.

Understanding Your Medical Insurance Bill: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Employer Coverage: Availability of employer-sponsored plans is a key determinant of participation

Employer-sponsored health insurance plans are a cornerstone of healthcare coverage in many countries, particularly in the United States, where they account for approximately 49% of the population's health insurance. The availability of these plans significantly influences health insurance participation rates, as they often provide a cost-effective and accessible option for employees. When employers offer health insurance as part of their benefits package, it creates a structured pathway for individuals to obtain coverage, thereby increasing overall participation.

Consider the mechanics of employer-sponsored plans: they typically involve group policies, which allow for lower premiums due to risk pooling across a large number of employees. For instance, a small business with 50 employees might negotiate a plan where the employer covers 70-80% of the premium cost, leaving employees to pay only 20-30%. This shared cost model makes health insurance more affordable for workers, especially those in lower-wage positions. Studies show that employees are 25-30% more likely to enroll in health insurance when their employer offers a subsidized plan compared to when no such option is available.

However, the availability of employer-sponsored plans is not uniform across industries or company sizes. Large corporations (500+ employees) are nearly twice as likely to offer health insurance as small businesses (1-49 employees). This disparity creates a coverage gap, with workers in smaller firms or part-time positions often left without access to employer-based plans. For example, in the retail sector, only 35% of workers are offered health insurance through their employer, compared to 75% in the finance industry. Policymakers and employers must address this imbalance to improve participation rates among underserved populations.

To maximize participation, employers can implement strategies such as auto-enrollment with opt-out provisions, which have been shown to increase enrollment by 15-20%. Additionally, offering multiple plan options (e.g., HMO, PPO, high-deductible plans) caters to diverse employee needs and preferences. For instance, a 30-year-old single employee might prefer a low-premium, high-deductible plan, while a 45-year-old with a family may opt for a more comprehensive PPO. Employers should also provide clear, accessible information about plan benefits and costs, as confusion is a common barrier to enrollment.

In conclusion, the availability of employer-sponsored health insurance plans is a critical determinant of participation rates, offering a structured and often subsidized pathway to coverage. However, disparities in access across industries and company sizes highlight the need for targeted solutions. By adopting inclusive policies and proactive enrollment strategies, employers can significantly enhance health insurance participation, ultimately contributing to better health outcomes for their workforce.

Pre-Tax or Post-Tax Medical Insurance: Which is the Smarter Choice?

You may want to see also

Explore related products

![]()

Government Policies: Subsidies, mandates, and public programs like Medicaid affect enrollment rates

Government policies wield significant influence over health insurance participation rates, acting as both catalysts and barriers to enrollment. Subsidies, mandates, and public programs like Medicaid are among the most potent tools in this arsenal. By reducing financial barriers, these policies make coverage more accessible to individuals and families who might otherwise forgo insurance due to cost concerns. For instance, the Affordable Care Act’s premium tax credits, which subsidize marketplace plans for eligible individuals earning up to 400% of the federal poverty level, have been instrumental in increasing enrollment among low- and middle-income populations. Similarly, Medicaid expansion under the ACA extended eligibility to millions of previously uninsured adults, particularly in states that adopted the expansion, demonstrating how policy decisions directly correlate with participation rates.

Mandates, another critical policy lever, create a floor for insurance participation by requiring individuals to obtain coverage or face penalties. The ACA’s individual mandate, though its penalty was reduced to $0 in 2019, initially drove enrollment by embedding insurance as a societal norm. Employer mandates, which require businesses with 50 or more employees to offer health insurance, further bolster participation rates by ensuring coverage for a significant portion of the workforce. However, mandates alone are insufficient without complementary policies like subsidies, as evidenced by the slight dip in enrollment after the individual mandate penalty was eliminated. This underscores the importance of a multi-pronged policy approach to sustain high participation rates.

Public programs like Medicaid and the Children’s Health Insurance Program (CHIP) play a dual role in shaping participation rates. First, they provide a safety net for vulnerable populations, including low-income adults, children, pregnant women, and individuals with disabilities. Second, they serve as a benchmark for private insurance, influencing market dynamics and consumer expectations. For example, Medicaid’s comprehensive benefits package often sets the standard for essential health benefits in private plans. However, the effectiveness of these programs in increasing participation hinges on state-level implementation. States that have expanded Medicaid under the ACA have seen significantly higher enrollment rates compared to non-expansion states, highlighting the critical role of state policy decisions in amplifying federal initiatives.

To maximize the impact of government policies on health insurance participation, policymakers must consider both design and execution. Subsidies should be structured to minimize out-of-pocket costs for low-income individuals while avoiding cliff effects that discourage income growth. Mandates must be paired with robust enforcement mechanisms and public awareness campaigns to ensure compliance. Public programs should be designed with flexibility to adapt to changing demographic and economic conditions, and states should be incentivized to adopt policies that align with federal goals. By strategically leveraging subsidies, mandates, and public programs, governments can create an environment where health insurance participation becomes not just a choice, but a feasible and desirable option for all.

Will Insurance Cover Roof Replacement for Blown-Off Shingles?

You may want to see also

Explore related products

$34.99

![]()

Awareness & Education: Knowledge of benefits and application processes boosts participation levels

Health insurance participation rates are significantly influenced by how well individuals understand the benefits available to them and the steps required to enroll. Without clear knowledge of what a plan covers—such as preventive care, prescription drugs, or mental health services—potential enrollees may underestimate its value. Similarly, complex application processes, often involving jargon-filled forms and multiple deadlines, can deter even those who recognize the need for coverage. A 2021 study by the Kaiser Family Foundation found that 40% of uninsured adults cited confusion about eligibility and enrollment as a barrier to obtaining health insurance. This highlights the critical role that awareness and education play in bridging the gap between available plans and actual participation.

To address this, targeted educational campaigns can demystify both the benefits and the application process. For instance, workshops or webinars that break down plan options—HMO vs. PPO, deductibles vs. copays—can empower individuals to make informed decisions. Practical tips, such as creating a checklist of required documents (e.g., proof of income, identification) or setting reminders for open enrollment dates, can streamline the application process. For younger demographics, leveraging social media platforms with concise, visually engaging content—infographics, short videos, or interactive quizzes—can increase engagement. Employers can also play a pivotal role by offering in-person or virtual sessions during benefits enrollment periods, ensuring employees understand their options and how to enroll.

A comparative analysis of successful awareness campaigns reveals that personalized communication yields higher participation rates. For example, Medicaid expansion states that utilized multilingual materials and community health workers saw enrollment increases of up to 25%. Similarly, campaigns that segment audiences—such as targeting low-income families with information on subsidies or seniors with details on Medicare Advantage plans—are more effective than one-size-fits-all approaches. Pairing education with actionable steps, like providing direct links to online applications or offering on-site assistance, further reduces barriers to participation.

However, education alone is not enough; it must be paired with ongoing support. Common pitfalls include assuming one-time outreach suffices or failing to address cultural or linguistic barriers. For instance, translating materials into multiple languages is essential in diverse communities, but ensuring cultural relevance—such as addressing specific health concerns prevalent in certain groups—can deepen trust and engagement. Additionally, follow-up reminders and simplified post-enrollment guidance, such as how to use insurance once enrolled, can prevent attrition and foster long-term participation.

In conclusion, boosting health insurance participation rates requires more than just making plans available—it demands proactive efforts to educate and guide individuals through the process. By combining clear, tailored communication with practical tools and ongoing support, stakeholders can transform awareness into action. This approach not only increases enrollment but also ensures that participants fully utilize their benefits, ultimately improving health outcomes and reducing financial strain.

Does Health Insurance End When You Quit Your Job?

You may want to see also

Frequently asked questions

The health insurance participation rate is influenced by factors such as affordability, awareness of available plans, government policies (e.g., mandates or subsidies), employer-sponsored coverage options, and individual perceptions of health risk and need for insurance.

The participation rate is typically calculated by dividing the number of individuals enrolled in health insurance plans by the total eligible population, then multiplying by 100 to express it as a percentage.

Yes, the participation rate often varies by demographic factors such as age, income level, employment status, geographic location, and education. For example, higher-income groups and those with employer-sponsored options tend to have higher participation rates.