Understanding how marketplace health insurance household income is calculated is crucial for determining eligibility for premium tax credits and cost-sharing reductions under the Affordable Care Act (ACA). Household income is computed by aggregating the modified adjusted gross income (MAGI) of all individuals who will be claimed as dependents on the tax return, including the primary taxpayer, spouse, and any dependents. This includes wages, salaries, tips, self-employment income, unemployment compensation, and other taxable income sources, while excluding certain deductions and exemptions. The ACA uses the federal poverty level (FPL) as a benchmark, with eligibility for subsidies typically ranging from 100% to 400% of the FPL, though some states have expanded Medicaid to cover individuals below 138% of the FPL. Accurate income reporting is essential, as discrepancies can affect subsidy amounts and may require repayment of excess credits during tax filing.

| Characteristics | Values |

|---|---|

| Definition | Household income is the total combined income of all members of a tax household who are required to file a tax return. |

| Purpose | Determines eligibility for premium tax credits and cost-sharing reductions on the Health Insurance Marketplace. |

| Income Sources Included | Wages, salaries, tips, self-employment income, unemployment compensation, Social Security benefits, pensions, alimony, capital gains, rental income, and other taxable income. |

| Income Sources Excluded | Child support payments, gifts, inheritances, and certain need-based benefits (e.g., SNAP, TANF). |

| Household Members | Includes the tax filer, spouse (if filing jointly), and any dependents claimed on the tax return. |

| Calculation Method | Modified Adjusted Gross Income (MAGI) is used, which is AGI plus certain deductions and exclusions. |

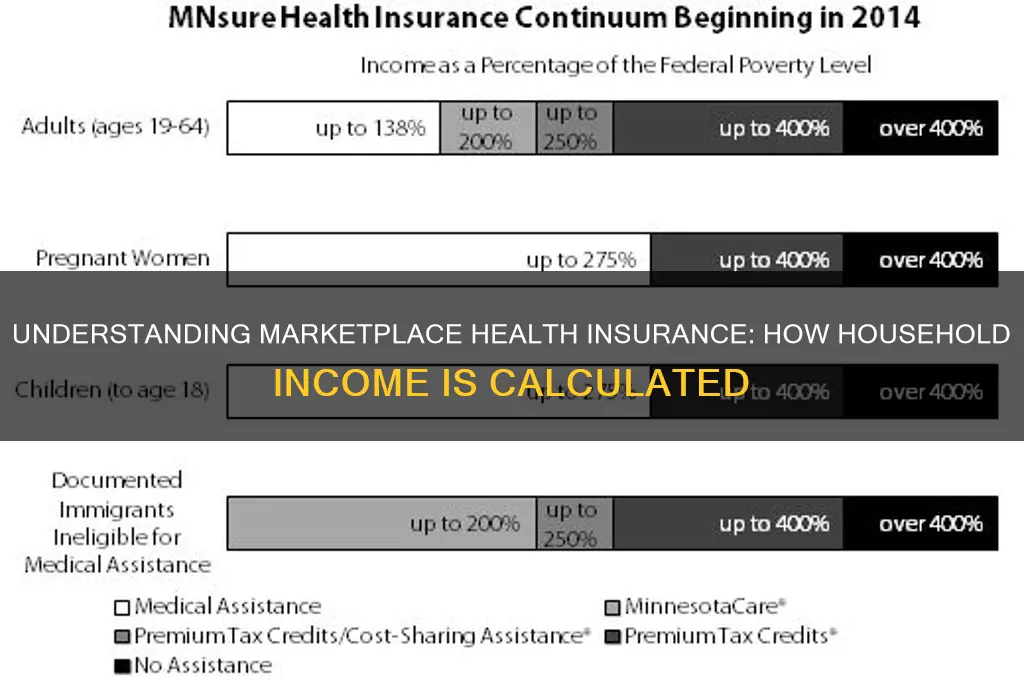

| Poverty Level Comparison | Household income is compared to the Federal Poverty Level (FPL) to determine eligibility for subsidies. |

| Eligibility Thresholds (2023) | - Premium Tax Credits: 100%-400% FPL - Cost-Sharing Reductions: 100%-250% FPL |

| Annual Updates | FPL and subsidy thresholds are updated annually based on inflation and other factors. |

| Verification | Income information is verified through tax returns, pay stubs, and other documentation during the application process. |

| Special Rules | Certain situations, like pregnancy or disability, may allow for income adjustments or special enrollment periods. |

| Reporting Changes | Changes in household income must be reported to the Marketplace to avoid incorrect subsidy amounts and potential penalties. |

Explore related products

What You'll Learn

- Income Sources Included: Wages, self-employment, investments, Social Security, and other taxable/non-taxable income

- Household Size Definition: Includes tax dependents, spouse, and children claimed on taxes

- Income Calculation Period: Based on current or projected annual income at enrollment

- Modified Adjusted Gross Income (MAGI): Used to determine eligibility for subsidies

- Income Verification Process: IRS data, pay stubs, and tax returns confirm accuracy

![]()

Income Sources Included: Wages, self-employment, investments, Social Security, and other taxable/non-taxable income

Understanding which income sources factor into your household income for health insurance calculations is crucial for accurate premium estimates and subsidy eligibility. The Affordable Care Act (ACA) marketplace considers a broad spectrum of income types, ensuring a comprehensive view of your financial situation. This includes not just your regular paycheck but also earnings from self-employment, investment returns, Social Security benefits, and other taxable or non-taxable income streams. Each of these sources plays a distinct role in determining your Modified Adjusted Gross Income (MAGI), the metric used to assess your eligibility for premium tax credits and cost-sharing reductions.

For instance, wages from traditional employment are straightforward—they’re reported on your W-2 form and directly added to your household income. Self-employment income, however, requires more scrutiny. If you’re a freelancer, contractor, or small business owner, your net profit (revenue minus business expenses) is included. Keep meticulous records of both income and deductible expenses, as overestimating or underestimating can skew your MAGI. For example, a self-employed graphic designer earning $60,000 annually but claiming $10,000 in legitimate business expenses would report $50,000 as income for marketplace purposes.

Investment income, such as dividends, capital gains, and interest, is also factored in, even if it’s not your primary income source. For retirees or individuals with substantial investments, this can significantly impact MAGI. Social Security benefits, including retirement, disability, and survivor benefits, are generally included as well, though certain exclusions may apply. For example, Supplemental Security Income (SSI) is not counted, as it’s considered a needs-based benefit. Understanding these nuances ensures you’re not overpaying for coverage or missing out on subsidies.

Non-taxable income sources, like child support payments or worker’s compensation, are often overlooked but still count toward your household income. Even tax-exempt interest from municipal bonds or foster care payments are included. To avoid surprises, gather all relevant documentation—tax returns, 1099 forms, Social Security statements, and records of non-taxable income—before applying for marketplace insurance. A miscalculation could lead to incorrect premium subsidies, potentially resulting in repayment of excess credits during tax season.

Finally, consider consulting a tax professional or using the marketplace’s income estimation tools if you have complex income sources. For example, a household with one spouse earning wages, another with self-employment income, and investment dividends would benefit from professional guidance to ensure accuracy. By meticulously accounting for all income sources, you’ll secure the most appropriate health insurance plan at the best possible price, tailored to your financial reality.

Health Insurance Coverage in Eugene, Oregon: Who's Protected?

You may want to see also

Explore related products

![]()

Household Size Definition: Includes tax dependents, spouse, and children claimed on taxes

Understanding how household size is defined is crucial when calculating income for marketplace health insurance. The definition goes beyond just counting heads; it specifically includes individuals who are tax dependents, a spouse, and children claimed on taxes. This precise categorization ensures that the financial assessment accurately reflects the economic unit being insured. For instance, a single parent with two children claimed as dependents would count as a household of three, even if other relatives live in the same home but are not claimed on taxes.

When determining household size, the IRS guidelines play a pivotal role. Tax dependents, as defined by the IRS, are individuals for whom you provide more than half of their financial support and who meet specific criteria, such as age or relationship. A spouse, whether married filing jointly or separately, is automatically included. Children claimed on taxes, regardless of age, are also part of the household size. For example, a college student who is financially dependent and claimed by their parents would be included, even if they live away from home.

Practical tips can simplify this process. First, review your most recent tax return to identify who was claimed as a dependent or included as a spouse. Second, ensure consistency between your tax filings and health insurance application to avoid discrepancies. If a family member’s status changes mid-year—such as a child turning 18 but remaining a dependent—update your information promptly. This ensures accurate premium tax credits and avoids potential repayment issues.

Comparatively, household size definitions can vary across programs, but for marketplace health insurance, the tax-based approach provides clarity. Unlike some assistance programs that consider all individuals living under one roof, this definition focuses on financial interdependence. For example, a grandparent living with their adult child’s family might not be included in the household size if they file taxes separately and are not claimed as a dependent. This distinction highlights the importance of aligning tax and insurance information.

In conclusion, mastering the household size definition is key to accurately calculating income for marketplace health insurance. By focusing on tax dependents, spouses, and claimed children, individuals can ensure their application reflects their true financial and familial structure. This precision not only streamlines the enrollment process but also maximizes eligibility for subsidies, making healthcare more accessible and affordable.

Renters Insurance: Medical Liability Explained

You may want to see also

Explore related products

![]()

Income Calculation Period: Based on current or projected annual income at enrollment

The income calculation period for Marketplace health insurance is a critical factor in determining eligibility for subsidies and the cost of your plan. It hinges on whether you use current or projected annual income at the time of enrollment. This decision isn’t arbitrary—it’s a strategic choice that can significantly impact your financial outlay for healthcare. For instance, if you anticipate a raise or bonus later in the year, projecting your income could position you for lower premiums or higher tax credits. Conversely, underestimating could lead to unexpected repayments at tax time.

To navigate this, start by gathering recent pay stubs, tax returns, or other income documentation. If your income fluctuates—perhaps due to self-employment or seasonal work—average your earnings over the past few months to estimate your annual income. The Marketplace typically requires you to report income in two categories: Modified Adjusted Gross Income (MAGI) and any non-taxable income, such as Social Security benefits. For families, combine all household income sources, including those of dependents who file taxes separately.

A common pitfall is failing to account for life changes that could alter your income mid-year. For example, a job loss, marriage, or the birth of a child can drastically shift your financial landscape. If such changes occur after enrollment, you’re required to update your income information through the Marketplace to avoid discrepancies. Failure to do so might result in over-subsidization, which would need to be repaid, or under-subsidization, leaving you with higher monthly premiums than necessary.

When projecting income, be realistic but thorough. Include all expected sources, such as wages, tips, investment income, and alimony. Exclude non-income items like child support payments or one-time gifts. If you’re unsure, err on the side of caution—overestimating slightly is safer than underestimating. Tools like the Marketplace’s income estimator can help, but always cross-reference with your own calculations.

Finally, remember that the income calculation period isn’t just about the present—it’s about foresight. By accurately assessing your current or projected income, you can optimize your health insurance costs and avoid financial surprises. Take the time to review and update your information regularly, especially during open enrollment or after significant life events. This proactive approach ensures you’re not only compliant with Marketplace rules but also maximizing your benefits.

How Governments Verify Uninsured Status: Methods and Implications

You may want to see also

Explore related products

![]()

Modified Adjusted Gross Income (MAGI): Used to determine eligibility for subsidies

Understanding how household income is calculated for marketplace health insurance is crucial for determining eligibility for subsidies. At the heart of this calculation lies the Modified Adjusted Gross Income (MAGI), a figure that serves as the primary metric for assessing financial need. Unlike standard Adjusted Gross Income (AGI), MAGI includes certain deductions and exclusions, such as foreign earned income and tax-exempt interest, to provide a more comprehensive view of a household’s financial situation. This nuanced approach ensures that subsidies are allocated fairly, reflecting both income and specific financial circumstances.

To calculate MAGI, start with your AGI, which is reported on your federal tax return. Then, add back specific items that were previously deducted, such as foreign earned income, housing expenses for qualified individuals living abroad, and tax-exempt interest. For example, if your AGI is $50,000 and you have $5,000 in foreign earned income, your MAGI would be $55,000. This adjusted figure is then used to determine eligibility for premium tax credits and cost-sharing reductions under the Affordable Care Act (ACA). It’s important to note that MAGI calculations apply to all members of a tax household, including dependents, so include their income and deductions as well.

One common misconception is that MAGI is solely based on taxable income. However, it accounts for a broader range of financial factors, making it a more accurate tool for assessing subsidy eligibility. For instance, if you’re self-employed, your MAGI will include your business income after deductions for half of your self-employment tax. Similarly, if you’re retired, pension income and Social Security benefits are factored into your MAGI. Understanding these inclusions ensures you provide accurate information when applying for marketplace health insurance, avoiding potential overpayments or underpayments in subsidies.

Practical tips for managing MAGI calculations include keeping detailed records of all income sources and deductions throughout the year. Use tax software or consult a tax professional to ensure accuracy, especially if your financial situation involves complexities like foreign income or self-employment. Additionally, estimate your MAGI for the upcoming year when enrolling in marketplace insurance, as subsidies are based on projected income. If your actual income differs significantly, you may need to reconcile the difference during tax filing, so plan accordingly to avoid surprises.

In conclusion, MAGI is a critical component in determining eligibility for health insurance subsidies, offering a tailored view of household income. By understanding its calculation and nuances, you can navigate the marketplace with confidence, ensuring you receive the appropriate level of financial assistance. Whether you’re self-employed, retired, or have foreign income, accurate MAGI reporting is key to maximizing your benefits while staying compliant with ACA guidelines.

Affordable Medical Plans: Options for the Uninsured

You may want to see also

Explore related products

![]()

Income Verification Process: IRS data, pay stubs, and tax returns confirm accuracy

Accurate income reporting is the cornerstone of determining eligibility for marketplace health insurance subsidies. The process isn't a simple declaration; it's a meticulous verification system relying on a trifecta of evidence: IRS data, pay stubs, and tax returns. This multi-layered approach ensures fairness and prevents fraudulent claims, safeguarding the integrity of the system.

Imagine relying solely on self-reported income. It would be a recipe for abuse, with individuals potentially underreporting to qualify for higher subsidies. The inclusion of IRS data acts as a powerful deterrent. The IRS, with its vast database and auditing capabilities, provides a reliable source of income information, cross-referencing tax filings and employer reports. This data forms the backbone of the verification process, offering a comprehensive snapshot of an individual's or household's financial situation.

However, IRS data isn't infallible. It reflects past income, which may not accurately represent current earnings, especially for those with fluctuating incomes or recent job changes. This is where pay stubs come in. These documents provide real-time evidence of current earnings, allowing for adjustments to be made based on recent changes in employment or income levels.

Think of it as a dynamic duo: IRS data provides the historical context, while pay stubs offer the present-day reality. Together, they paint a more complete picture of an individual's financial landscape. But what about self-employed individuals or those with non-traditional income sources? This is where tax returns become crucial. They provide a detailed breakdown of income from various sources, including investments, rental properties, and business profits. By scrutinizing tax returns, the marketplace can accurately assess the total household income, ensuring a fair and equitable distribution of subsidies.

The income verification process isn't just about catching discrepancies; it's about ensuring access to affordable healthcare for those who truly need it. By meticulously cross-referencing IRS data, pay stubs, and tax returns, the marketplace can confidently determine eligibility, preventing abuse while providing vital support to those who qualify.

Insurance Companies: Can They Deny Coverage for Pain Medication?

You may want to see also

Frequently asked questions

Household income for marketplace health insurance is calculated using the Modified Adjusted Gross Income (MAGI), which includes taxable income from all household members, such as wages, salaries, tips, and investment income, adjusted for certain deductions.

The household includes the tax filer, their spouse (if filing jointly), and any dependents claimed on the tax return, regardless of whether they need health coverage.

Yes, unemployment benefits and taxable Social Security income are included in the household income calculation for marketplace health insurance.

No, financial assistance from family or friends that is not taxable income is not included in the household income calculation for marketplace health insurance.