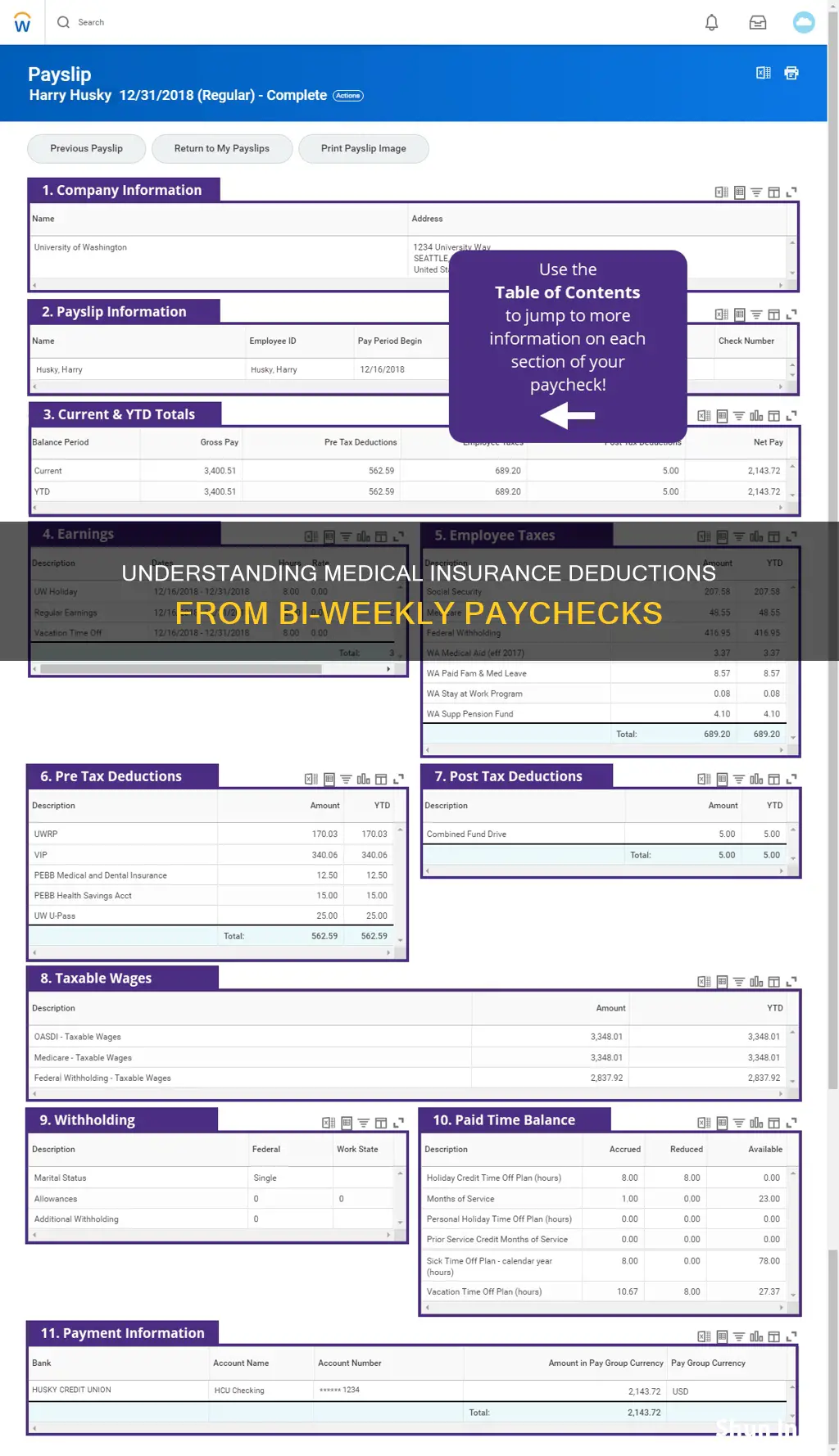

Understanding how medical insurance is deducted from paychecks can be confusing, especially when considering the different options available, such as pre-tax or post-tax deductions, and the impact of pay frequency. When an individual is paid bi-weekly, the annual cost of insurance is typically divided by 26, resulting in an equal deduction from each paycheck. This ensures that employees contribute during the month their coverage is active. Pre-tax deductions, which are common for employer-sponsored plans, involve deducting the employee-paid portion of insurance premiums before withholding taxes. On the other hand, post-tax deductions, also known as after-tax, are calculated differently, affecting tax payments and eligibility for other benefits.

| Characteristics | Values |

|---|---|

| Insurance billing | The employee's insurance deductions occur in the month they are receiving insurance coverage. |

| Deduction amount | The amount deducted depends on the plan the employee has enrolled in. |

| Deduction frequency | If paid bi-weekly, the deduction is taken from 26 paychecks per year. |

| Pre-tax or post-tax | Pre-tax health insurance premiums may not be deducted before certain taxes are withheld or contributed. |

| Employer contribution | The employer pays the full cost of insurance upfront during the month prior to coverage. |

Explore related products

What You'll Learn

![]()

Pre-tax and after-tax health insurance options

The distinction between pre-tax and after-tax health insurance options is important as it determines how much employees pay in taxes and their eligibility for other employer-sponsored benefits. Pre-tax health insurance plans are those where the employer deducts the cost of the insurance from the employee's gross pay before withholding any taxes. This reduces the employee's tax liability. Employer-sponsored plans are typically pre-tax deductions for employees. In some states, however, a pre-tax health premium may not be pre-tax for certain taxes, such as state unemployment tax.

One of the most common types of medical insurance plans for employers is a Section 125 cafeteria plan. According to the IRS, Section 125 plans are written plans maintained by employers where all participants are employees, and participants can choose between two or more benefits. The benefits consist of cash and qualified benefits, and they are not included in gross income. Typically, you cannot include benefits that defer an employee's pay in a cafeteria plan.

After-tax medical premiums are an alternative option if an individual does not want to participate in their employer's pre-tax plan or if their employer does not offer a pre-tax plan. When filing income taxes, you may be able to deduct these premiums as an itemized deduction for all medical expenses and premiums that exceed 7.5% of your income. Additionally, most self-employed taxpayers can deduct health insurance premiums using Schedule 1 for Line 162 on Form 1040. It is important to note that if you are eligible for an employer-sponsored, pre-tax health plan and decline that coverage, you cannot deduct your insurance premium.

Health reimbursement arrangements (HRAs) offer pre-tax benefits, allowing employees to pay for their premiums with post-tax dollars. An employer can reimburse employees for medical costs, including payments on premiums, using non-taxable funds. With HRAs, employees can choose the health plan they want or need. A Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) is available for small employers who are not required to purchase company health insurance under the Affordable Care Act (ACA). A small employer under the ACA is one with fewer than 50 full-time equivalent (FTE) employees.

Medical Insurance Coverage for Torus Massa Removal Surgery

You may want to see also

Explore related products

![]()

Calculating employee-only premiums

The process of calculating employee-only premiums for medical insurance involves several steps and considerations. Firstly, it's important to determine the total employee-only premium cost. This amount can vary depending on the specific insurance plan chosen and the employee's coverage needs. For example, let's assume the total employee-only premium is $359.03.

The next step is to subtract the amount that the employer contributes to the insurance plan. Employers often cover a portion of the insurance costs for their employees. In our example, let's say the employer contributes $200 towards the total employee-only cost. If the contribution is a percentage rather than a fixed amount, be sure to calculate the percentage and subtract that value.

At this point, it's important to consider whether the employee has any dependents, as this will impact the total cost. The dependent care costs should be added to the remaining amount after subtracting the employer's contribution.

Additionally, there may be other benefits or additional coverages that need to be included. These could include dental insurance, vision insurance, or other supplemental insurance plans. These additional benefits will increase the total cost.

Now, we have calculated the total amount to be paid by the employee. To determine the bi-weekly deduction, we need to divide this amount by the number of pay periods in a year. Since bi-weekly means being paid every two weeks, there will be 26 pay periods in a year. So, in our example, the remaining cost of $159.03 would be divided by 26, resulting in a bi-weekly deduction of approximately $73.39.

It's worth noting that the frequency of paychecks can vary, and the calculation should be adjusted accordingly. For instance, if paychecks are issued bi-monthly (twice a month), the number of pay periods in a year would be 24, and the calculation would be adjusted to reflect that.

Lastly, it's important to understand the distinction between pre-tax and post-tax health insurance options. Pre-tax deductions are typically made before any taxes are withheld, which can reduce the overall tax burden for employees. On the other hand, post-tax deductions are made after taxes have been calculated and withheld. Consulting with a payroll specialist or tax advisor can help ensure that the correct calculations and considerations are made for employee-only premiums and tax implications.

Medical Insurance and IRS Reporting: What You Need to Know

You may want to see also

Explore related products

![]()

Health reimbursement arrangements (HRAs)

There are different types of HRAs, including the Excepted Benefit Health Reimbursement Arrangement (EBHRA). Any employer, regardless of size, can set up an EBHRA, but it must be in addition to a traditional health insurance plan. It cannot be offered as a replacement. EBHRAs cover any premiums not included in the traditional plan, such as dental insurance, as well as copays and deductibles.

Another type of HRA is the Qualified Small Employer Health Reimbursement Arrangement (QSEHRA). This is available for small employers who are not required to purchase company health insurance under the Affordable Care Act (ACA). A small employer, in this case, is defined as having fewer than 50 full-time equivalent (FTE) employees.

In terms of payroll, deductions for insurance typically occur in the month an employee is receiving coverage. For those paid bi-weekly, the cost of insurance is usually divided by the number of paychecks received in a year. So, if an employee is paid bi-weekly, the cost is divided by 26, and this amount is deducted from each paycheck.

Spend Down Life Insurance: Planning for Medicaid Eligibility

You may want to see also

Explore related products

![]()

Deductions for employees with dependents

When it comes to deductions for employees with dependents, the calculation becomes a little more intricate. The total cost of the insurance plan, including the employee's premium and the employer's contribution, serves as the foundation.

Firstly, determine the total employee-only premium. This figure represents the cost of coverage solely for the employee, excluding any dependents. Then, subtract the amount that the employer contributes to the total employee-only cost. If the employer contributes a percentage of the premium, be sure to calculate and subtract that percentage.

The next step is crucial for employees with dependents. You must add the total dependent cost to the equation. This amount will vary depending on the number and type of dependents covered under the employee's plan. Once you have calculated the total dependent cost, you can proceed with the remainder of the formula.

For instance, consider an employee with a premium of $359.03, and the employer contributes $200 towards the total employee-only cost. After subtracting the employer's contribution, you are left with $159.03. Now, factor in the total dependent cost, assuming it amounts to $50 per dependent. If this employee has two dependents, you would add $100 to the $159.03, resulting in $259.03.

Finally, since the employee is paid bi-weekly, you must adjust the amount for the pay frequency. To do this, take the total amount after adding the dependent cost ($259.03 in our example) and multiply it by 12 (months in the year) and then divide it by 26 (the number of pay periods in a bi-weekly pay structure). This calculation will give you the deduction amount for each bi-weekly paycheck.

How to Access Your Medical Insurance Statement

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Monthly vs bi-weekly payments

When it comes to insurance payments, there are a few options for how often you can make them. The most common options are monthly and bi-weekly payments. So, what's the difference between the two?

Monthly payments are typically smaller amounts that are deducted from your paycheck once a month. This option can be great if you're looking for a more affordable choice with a smaller commitment. It can help you budget better and spread the cost of insurance throughout the year. Additionally, paying monthly can improve your credit score by making payments on time. If you're looking to take out a loan or finance a large purchase, a good credit score can help you secure more favourable terms. In some cases, insurers may even offer a discount for choosing to pay monthly, which can result in you paying less overall. However, it's important to note that paying monthly may require more time and attention to ensure you're making the payment each month, and you may end up paying more in processing fees.

On the other hand, bi-weekly payments are made every two weeks, which means you'll be making more frequent payments. The amount deducted for insurance is typically calculated by dividing the annual cost by the number of paychecks you receive in a year. For those paid bi-weekly, this usually works out to be 1/26 of the annual premium deducted from each paycheck. One advantage of bi-weekly payments is that you're paying towards your insurance more often, which can result in lower monthly costs. Additionally, if there is a month where you receive three paychecks instead of two, you won't have any insurance deductions from that third paycheck. However, the frequent payments may be harder to keep track of, and you'll need to ensure you have the funds available more often.

Ultimately, the decision between monthly and bi-weekly payments depends on your personal preferences and financial situation. Monthly payments can provide more flexibility and affordability, while bi-weekly payments can help reduce the overall cost of insurance by spreading it out over more paychecks. It's important to consider your income, expenses, and financial goals when deciding which payment option is right for you.

Additionally, it's worth noting that some insurance providers may offer discounts for paying in larger instalments, such as bi-annually. Paying a larger sum upfront can save you money on interest over time, but it may not be feasible if you're working with a tight budget or unpredictable income.

Best Medical Insurance Options in California

You may want to see also

Frequently asked questions

The employer pays the full cost of insurance upfront during the month before coverage, and the employees contribute during the month their coverage is active. The annual premium is typically divided by 26 pay periods. This means that if an employee is paid bi-weekly, 1/26 of the annual premium is deducted from each paycheck.

If an employee is paid bi-monthly, 1/24 of the annual premium is deducted from each paycheck.

The formula to calculate the deductions for an employee's health insurance is as follows: Take the total employee-only premium and subtract the amount that the employer contributes. If the employee has dependents, add in the total dependent cost. If there are additional benefits, add them in and follow the formula. Multiply the final amount by 12 (months in the year) and divide by 26 (number of pay periods).

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)