Mortgage insurance is an insurance policy that protects the lender in the event of the borrower defaulting on payments. It is usually required when the borrower makes a down payment of less than 20% and is calculated based on the loan amount, credit score, down payment amount, and debt-to-income ratio. The cost of private mortgage insurance (PMI) is typically between 0.5% to 1.5% of the loan amount per year, paid in monthly installments as part of the borrower's regular mortgage payment. Lender-paid mortgage insurance, on the other hand, results in a higher interest rate on the loan. Various online calculators can be used to estimate monthly mortgage payments, including mortgage insurance, property taxes, and homeowners' fees.

| Characteristics | Values |

|---|---|

| Purpose of mortgage insurance | Protects the lender in case the borrower defaults on the loan |

| Who pays for it | The borrower pays for it, but it is arranged by the lender |

| When is it paid | Monthly, with little or no initial payment required at closing |

| How is it calculated | Based on the loan amount, credit score, down payment amount, and debt-to-income ratio |

| Average monthly cost | 0.46% to 1.5% of the loan amount |

| Cancellation | Can be cancelled when the mortgage balance drops to 78% of the home's original value or halfway through the loan term |

| Types | Private mortgage insurance (PMI), qualified mortgage insurance premium (MIP), mortgage title insurance |

Explore related products

What You'll Learn

![]()

The impact of PMI on monthly payments

Private Mortgage Insurance (PMI) is an additional expense for borrowers who make a down payment of less than 20% of the property value. It is calculated as a percentage of the mortgage loan amount, typically ranging from 0.5% to 1.5% of the total loan amount per year. This annual premium is then divided into 12 monthly instalments, which are added to the borrower's monthly mortgage payment. The cost of PMI depends on the loan size, credit score, down payment amount, and debt-to-income ratio. Borrowers with lower credit scores tend to pay higher PMI rates on conventional loans, but this doesn't apply to government-backed mortgages.

The benefit of PMI is that it enables individuals to buy a house sooner by allowing for a lower down payment. Without PMI, homebuyers may have to wait years to save for a larger down payment, delaying their transition from renting to building home equity. While PMI increases the cost of the loan, it can be more affordable in the long run compared to higher interest rates associated with a larger loan.

There are different options for paying PMI. Borrower-paid PMI is the most common, with premiums included in the monthly mortgage payment. Lender-paid PMI, on the other hand, results in a higher interest rate on the loan, and it is more challenging to cancel. Single-premium PMI involves paying the entire cost of the premiums as a lump sum, leading to lower monthly payments but requiring significant upfront funds. A split-premium PMI combines the benefits of borrower-paid and single-premium PMI, with a larger upfront fee and lower monthly payments.

When considering the impact of PMI on monthly payments, it's essential to factor in property taxes, homeowners insurance, and other associated costs, which vary depending on the property's location. Online mortgage calculators can assist in understanding the total estimated monthly mortgage payment, including PMI, taxes, and insurance. These tools allow for adjustments based on down payment percentages, loan terms, home prices, and other variables, providing a comprehensive view of the financial commitment involved in purchasing a home.

Transforming Your Drive Insurance Report: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

How to cancel PMI

Private mortgage insurance (PMI) is an additional expense for conventional mortgage borrowers who make a down payment of less than 20%. While the borrower pays for it, PMI protects the lender since they take on more risk when lending a larger loan with a lower down payment.

- Wait for automatic cancellation: Lenders are required to automatically cancel PMI when your mortgage balance reaches 78% of your home's original value or once you are halfway through your loan term, whichever comes first.

- Request early cancellation: You can request to cancel PMI when your loan-to-original-value (LTOV) ratio falls below 80%. To calculate your LTOV, divide your current unpaid principal balance by the purchase price or appraised value of your home at closing, whichever is lower. Make your request in writing and ensure you are current on your mortgage payments.

- Refinance: With rising home values, you may have the equity needed to refinance your loan and avoid paying PMI. For example, you could refinance from an FHA loan to a conventional loan, eliminating your mortgage insurance premium (MIP).

- Pay extra towards your principal: Paying extra can help you reach 20% equity faster and become eligible for PMI cancellation. Check with your lender to ensure that extra payments go towards the loan's principal and not your next payment or interest.

It is important to note that the rules for PMI cancellation may vary depending on the lender and the type of loan. For example, mortgages through the Federal Housing Administration (FHA) or Department of Veterans Affairs (VA) have different requirements. Therefore, it is always a good idea to consult your lender or servicer for specific information regarding your loan.

Insuring Half-Million Dollar Homes

You may want to see also

Explore related products

![]()

How your credit score affects PMI

Your credit score has a significant impact on the cost of your Private Mortgage Insurance (PMI). The higher your credit score, the lower your PMI cost. A credit score of 760 or above generally attracts the lowest PMI rates.

Borrowers with lower credit scores tend to pay higher PMI rates on conventional loans. However, this isn't always the case with government-backed mortgages, such as FHA loans, where borrowers with lower credit scores can often save money.

The size of your down payment will also influence your PMI. The larger the down payment, the less you'll pay for PMI. A down payment of 20% is considered the norm, and anything lower than this will usually require PMI. However, even if you can't reach 20%, a down payment of 7% will still lower your PMI charges compared to a minimum down payment of 3%.

Your debt-to-income (DTI) ratio is another factor that determines your PMI. The DTI ratio measures your monthly debt payments against your monthly pre-tax income. The lower your DTI ratio, the lower your PMI will be.

PMI rates can vary from 0.25% to 1.5% of the total loan amount annually. For example, a $300,000 loan could cost between $750 and $4,500 per year in PMI, or between $60 and $375 per month.

It's worth noting that PMI isn't a permanent expense. Lenders are required to cancel PMI when your mortgage balance drops to 78% of your home's original value or when you're halfway through your loan term, whichever comes first.

Rabbit Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Mortgage insurance for government-backed loans

Mortgage insurance, also known as Private Mortgage Insurance (PMI), is an extra expense for conventional mortgage borrowers who make a down payment of less than 20%. The average monthly cost of PMI is 0.46% to 1.5% of the loan amount, according to the Urban Institute. Your credit score plays a major role in the cost of PMI—the higher your score, the lower your PMI cost.

Government-backed loans are insured by federal agencies, which reduces the risk for lenders, allowing them to be more lenient with credit scores and down payments. The three types of government-backed loans are Federal Housing Administration (FHA) loans, USDA loans, and VA loans.

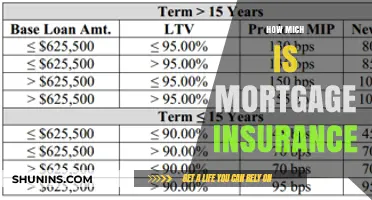

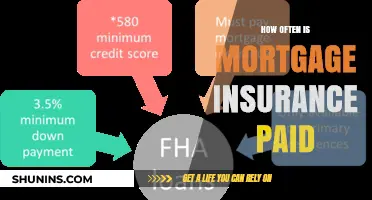

FHA loans are designed to help first-time homebuyers and those with lower incomes achieve homeownership. They often have lower down payments and closing costs than conventional loans, with more relaxed credit criteria. FHA loans require borrowers to pay for mortgage insurance premiums (MIP) for the life of the loan if they make a down payment of less than 10%. You'll typically pay an upfront premium of 1.75% of the loan amount, plus an annual premium of 0.15% to 0.75%.

USDA loans offer up to 100% financing, making it possible to buy a home with no down payment. They are restricted to eligible rural areas and are designed to help low-to-moderate-income individuals in those areas become homeowners.

VA loans are the most restrictive government-backed loans in terms of accessibility. To qualify, you must be an active-duty service member, a veteran, an eligible spouse of a veteran, or a US citizen who served in the armed forces of a government allied with the US during World War II. VA loans do not require mortgage insurance, but they include a funding fee that varies depending on the type of loan, the size of the down payment, and whether it's the borrower's first VA loan.

Insurance: When Your House Is Under Contract

You may want to see also

Explore related products

![]()

Mortgage insurance for conventional loans

Private mortgage insurance (PMI) is a type of mortgage insurance that is usually required with a conventional loan when the buyer makes a down payment of less than 20% of the home's value. PMI is calculated as a percentage of your mortgage loan amount and protects the lender if the buyer stops making loan payments. The cost of PMI is affected by factors like your credit score and the amount of your down payment. Generally, the higher your credit score, the lower your PMI cost. The average monthly cost of PMI is 0.46% to 1.5% of the loan amount, although in 2022 it typically ranged from 0.58% to 1.86% annually.

PMI can be removed from your monthly mortgage payment when you've reached 20% equity in your home or paid your loan balance low enough. It is an additional monthly cost that is rolled into your mortgage payment and protects only the lender, not the buyer. Lenders sometimes offer conventional loans with smaller down payments that do not require PMI. As a trade-off, you usually pay a higher interest rate for these loans.

Borrower-paid PMI is the most common type of PMI, where the premiums are part of your monthly mortgage payment. You can request to cancel these when you reach 20% equity in your home. Lender-paid mortgage insurance, on the other hand, is paid by the lender, but you will pay a higher interest rate on the loan. Single-premium PMI bundles the entire cost of the premiums into one lump payment, which can be paid in full at closing or rolled into the loan for a higher balance.

Mortgage insurance can help you buy a house sooner. While you might pay more than $100 per month for PMI, you could start gaining tens of thousands per year in home equity. Mortgage insurance costs vary by loan program, but in general, the cost of PMI is about 0.5% to 1.5% of the loan amount per year. This annual premium is broken into monthly instalments, which are added to your monthly mortgage payment.

Protect Your Priceless: Insure Your Engagement Ring

You may want to see also

Frequently asked questions

PMI stands for Private Mortgage Insurance. It is an additional insurance policy that protects the lender if the borrower is unable to pay their mortgage.

If you pay less than a 20% down payment on your home, you will have to pay PMI. Lenders usually require PMI if you put down less than 20% on a conventional home loan.

The amount you'll pay for PMI depends on several factors, including the size of your loan, your down payment amount, debt-to-income ratio, and credit score. The larger your down payment, the less your PMI will cost. Your total PMI amount will always be a percentage of your total mortgage.