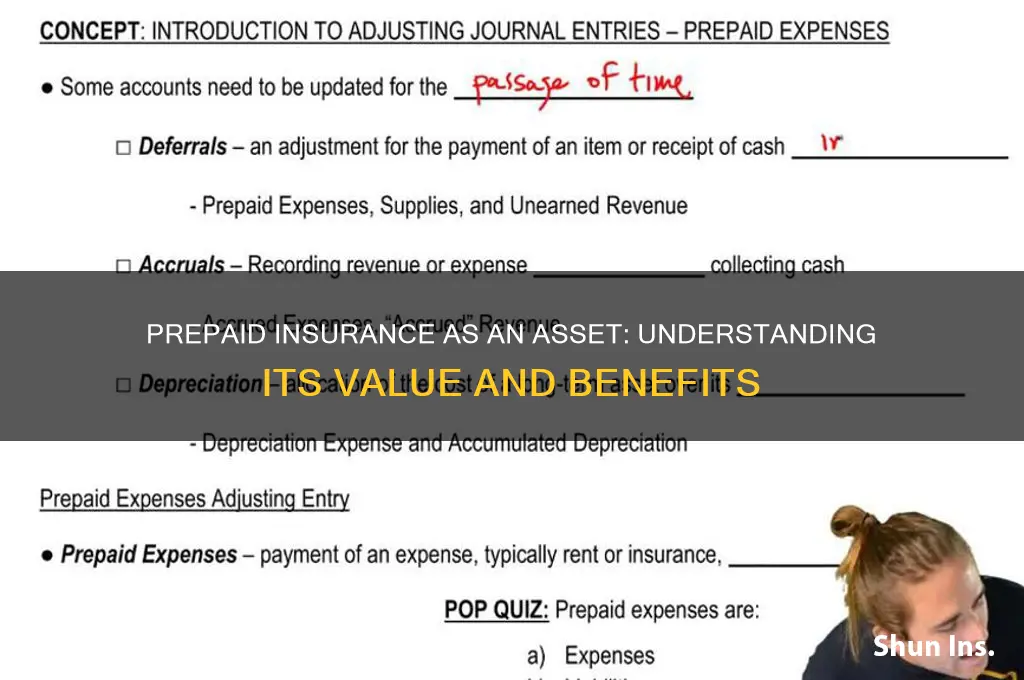

Prepaid insurance is considered an asset because it represents a prepaid expense that provides future economic benefits to a business. When a company purchases an insurance policy and pays the premium in advance, it records the amount as a prepaid asset on its balance sheet. This is because the insurance coverage has not yet been fully consumed and will provide protection over a specified period, typically a year. As time passes and the insurance coverage is utilized, the prepaid insurance is gradually expensed, reducing the asset balance. This treatment aligns with the accounting principle of matching expenses with the periods in which they are incurred, ensuring that the financial statements accurately reflect the company’s financial position and performance. Thus, prepaid insurance is classified as a current asset, as it is expected to be fully utilized within one year or the operating cycle, whichever is longer.

| Characteristics | Values |

|---|---|

| Definition | Prepaid insurance is a current asset account that represents the amount of insurance premium paid in advance for coverage that has not yet been used or expired. |

| Recognition | Recorded as an asset on the balance sheet when the insurance premium is paid upfront for a future period. |

| Classification | Classified as a current asset because it is expected to be consumed or used within one year or the operating cycle, whichever is longer. |

| Amortization | The prepaid insurance is amortized (expensed) over the period of coverage, typically on a monthly basis, to reflect the usage of the insurance. |

| Journal Entry | When prepaid: Debit Prepaid Insurance (asset), Credit Cash (or Accounts Payable). When amortized: Debit Insurance Expense, Credit Prepaid Insurance. |

| Financial Impact | Reduces cash at the time of payment but does not immediately affect the income statement. The expense is recognized over time as the insurance coverage is used. |

| Example | A company pays $12,000 for a 12-month insurance policy on January 1. Each month, $1,000 is expensed as insurance expense, reducing the prepaid insurance balance. |

| Reporting | Reported on the balance sheet under current assets until fully amortized. |

| Tax Treatment | Generally, prepaid insurance is deductible for tax purposes in the period the expense is recognized, not when paid. |

| Relevance | Important for accurate financial reporting and matching expenses with the period in which they are incurred (matching principle). |

Explore related products

What You'll Learn

![]()

Definition of Prepaid Insurance

Prepaid insurance is a financial concept that transforms a routine expense into a tangible asset on a company's balance sheet. At its core, prepaid insurance refers to the advance payment made by a business for insurance coverage that extends beyond the current accounting period. This means that when a company pays for a year's worth of insurance upfront, only the portion of the coverage that applies to the current period is considered an expense, while the remaining amount is recorded as a prepaid asset. This distinction is crucial for accurate financial reporting and reflects the principle of matching expenses with the periods they benefit.

To illustrate, consider a small business that pays $12,000 annually for property insurance in January. In the first month, only $1,000 (1/12th of the total) is recognized as an insurance expense, while the remaining $11,000 is classified as prepaid insurance—an asset. This asset is gradually reduced each month as the insurance coverage is consumed. This approach ensures that the company's financial statements accurately reflect its financial health by deferring the recognition of expenses to the periods they actually provide benefits.

From an analytical perspective, prepaid insurance serves as a buffer against future expenses, enhancing a company's liquidity and financial stability. It is treated as a current asset because it represents a resource that will be used within the next 12 months. For instance, if a company faces unexpected cash flow challenges, having prepaid insurance means it doesn’t need to allocate additional funds for insurance premiums in the near term. This strategic financial management allows businesses to allocate resources more efficiently, focusing on growth and operational needs.

A comparative analysis reveals that prepaid insurance differs from other prepaid expenses, such as rent or supplies, in its specific purpose and treatment. While all prepaid expenses are assets, insurance stands out because it directly mitigates risk—a critical function for businesses. For example, a manufacturing company with prepaid liability insurance not only ensures compliance with legal requirements but also protects itself against potential lawsuits or claims. This dual benefit underscores the value of prepaid insurance as both a financial asset and a risk management tool.

In practical terms, businesses should meticulously track prepaid insurance to ensure compliance with accounting standards like GAAP or IFRS. This involves regular adjustments through journal entries to transfer the appropriate portion of the prepaid asset to an expense account each period. For instance, using accounting software can automate this process, reducing the risk of errors and ensuring accuracy. Additionally, companies should review their insurance policies annually to optimize coverage and avoid overpaying, thereby maximizing the asset’s value. By understanding and effectively managing prepaid insurance, businesses can strengthen their financial position and operational resilience.

Dog Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Balance Sheet Classification

Prepaid insurance is classified as a current asset on the balance sheet because it represents a resource that will provide future economic benefits within one year or the operating cycle, whichever is longer. This classification aligns with accounting principles that require assets to be categorized based on their liquidity and expected conversion into cash. Unlike long-term assets, prepaid insurance is short-term in nature, as it covers expenses for a defined period, typically 12 months or less. For instance, if a company pays $12,000 annually for property insurance in January, $1,000 is expensed monthly, while the remaining balance is recorded as a prepaid asset until it is fully utilized.

The balance sheet classification of prepaid insurance is crucial for accurately reflecting a company’s financial health. By listing it as a current asset, businesses ensure that their short-term liquidity is not understated. This is particularly important for stakeholders, such as investors and creditors, who rely on the balance sheet to assess a company’s ability to meet its obligations. For example, a startup with $50,000 in prepaid insurance alongside $100,000 in cash would show a stronger liquidity position than if the prepaid amount were omitted or misclassified. Proper classification also ensures compliance with accounting standards like GAAP or IFRS, avoiding potential audit issues.

One practical tip for managing prepaid insurance is to regularly reconcile the prepaid account to ensure accuracy. This involves tracking the portion of the prepaid expense that has been consumed over time and adjusting the balance accordingly. For instance, if a company has $6,000 in prepaid rent for six months, $1,000 should be moved from the asset account to an expense account each month. This practice not only maintains the integrity of the balance sheet but also provides a clear picture of cash outflows and remaining coverage. Software tools like QuickBooks or Excel templates can automate this process, reducing the risk of errors.

A comparative analysis highlights the difference between prepaid insurance and other current assets, such as inventory or accounts receivable. While inventory and receivables are directly tied to operations and revenue generation, prepaid insurance is a protective measure that ensures business continuity. For example, a manufacturing company might have $200,000 in inventory and $50,000 in prepaid insurance. Both are current assets, but the prepaid insurance serves a distinct purpose—safeguarding against potential losses rather than generating income. This distinction underscores the importance of categorizing assets based on their function and time horizon.

In conclusion, the balance sheet classification of prepaid insurance as a current asset is a critical aspect of financial reporting. It ensures transparency, compliance, and an accurate representation of a company’s short-term resources. By understanding this classification and implementing practical management strategies, businesses can maintain financial integrity and provide stakeholders with reliable information. Whether through manual tracking or automated tools, proper handling of prepaid insurance reinforces the balance sheet’s role as a cornerstone of financial analysis.

Navigating Insurance After a Spouse's Death: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Amortization Process

Prepaid insurance is recognized as an asset because it represents a future economic benefit—specifically, coverage for a period that hasn’t yet occurred. When a business pays for insurance upfront, it doesn’t immediately expense the full amount. Instead, it records the payment as an asset on the balance sheet, gradually recognizing the expense over the policy’s coverage period. This aligns with the matching principle in accounting, ensuring expenses are matched with the revenues they help generate. The process of allocating this prepaid asset over time is called amortization, and it’s a critical step in accurately reflecting a company’s financial health.

Amortization of prepaid insurance involves systematically reducing the asset’s value as the coverage period progresses. For example, if a company pays $12,000 for a one-year insurance policy in January, it wouldn’t record a $12,000 expense immediately. Instead, it would recognize $1,000 as an expense each month, with the remaining $11,000 (and then $10,000, $9,000, etc.) staying on the balance sheet as a prepaid asset. This is typically done through a journal entry: debiting Insurance Expense and crediting Prepaid Insurance for the monthly amount. By December, the prepaid asset would be fully expensed, and the balance sheet would reflect $0 for that policy.

The amortization process requires careful tracking to ensure accuracy. Small businesses often use accounting software to automate this, but manual calculations are straightforward. Divide the total prepaid amount by the number of months (or periods) covered by the policy. For instance, a $6,000 six-month policy would amortize at $1,000 per month. Caution is advised when policies span different accounting periods, as misalignment can lead to over- or under-expensing. Regularly reviewing the prepaid insurance schedule helps catch errors and ensures compliance with accounting standards like GAAP or IFRS.

A key takeaway is that amortization transforms a lump-sum payment into a series of manageable expenses, providing a clearer picture of a company’s financial obligations. It also prevents distortion in income statements, where expensing the full amount upfront would overstate costs in one period and understate them in others. For businesses with multiple prepaid policies, organizing them by expiration date and coverage period streamlines the amortization process. This not only improves financial reporting but also aids in budgeting and cash flow management, as future expenses are predictable and evenly distributed.

In practice, the amortization of prepaid insurance is a simple yet powerful tool for maintaining financial accuracy. It underscores the principle that assets should reflect their actual usage over time, not just their initial cost. By mastering this process, businesses can ensure their financial statements are both compliant and informative, supporting better decision-making and stakeholder trust. Whether handled manually or through software, the consistency and precision of amortization are non-negotiable in sound accounting practices.

Choosing the Right Umbrella Insurance Coverage: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Impact on Financial Statements

Prepaid insurance is classified as a current asset on the balance sheet because it represents a future economic benefit that will be realized within one year or the operating cycle, whichever is longer. This classification directly impacts financial statements by affecting both the balance sheet and the income statement. When a company pays for insurance coverage in advance, the initial payment is recorded as a prepaid expense, increasing the asset account. This entry ensures that the company’s financial position reflects the value of the unused portion of the insurance policy, which will provide benefits over time.

Consider the example of a company that pays $12,000 for a one-year insurance policy upfront. At the time of payment, the journal entry would debit Prepaid Insurance (an asset) and credit Cash for $12,000. As each month passes, $1,000 of the prepaid insurance is recognized as an expense, reducing the asset account and increasing Insurance Expense on the income statement. This systematic allocation ensures that expenses are matched with the revenue they help generate, adhering to the matching principle of accounting.

The impact on the income statement is gradual but significant. By spreading the cost of insurance over the coverage period, the company avoids distorting its financial performance in any single period. For instance, if the entire $12,000 were expensed immediately, it would overstate expenses in the month of payment and understate them in subsequent months. Instead, the monthly recognition of $1,000 as an expense provides a more accurate representation of the company’s financial health and operational efficiency.

Another critical aspect is the effect on liquidity ratios. Since prepaid insurance is a current asset, it contributes to metrics like the current ratio and working capital. For example, a company with $50,000 in current assets (including $5,000 in prepaid insurance) and $40,000 in current liabilities would have a current ratio of 1.25. Excluding prepaid insurance would reduce current assets to $45,000, lowering the ratio to 1.125. This highlights how prepaid insurance can influence perceptions of a company’s short-term financial stability and ability to meet obligations.

In summary, prepaid insurance impacts financial statements by enhancing asset representation on the balance sheet and ensuring expense recognition aligns with the benefits received. Its treatment as a current asset affects liquidity ratios, offering stakeholders a clearer view of the company’s financial position. Proper management of prepaid insurance entries is essential for accurate financial reporting and informed decision-making.

Navigating Insurance Coverage: A Guide to Requesting Your Breast Pump

You may want to see also

Explore related products

![]()

Difference from Expenses

Prepaid insurance is classified as an asset because it represents a future benefit that has already been paid for, distinguishing it from expenses, which reflect immediate consumption or use. While expenses are recognized in the period they are incurred, prepaid insurance is recorded as an asset on the balance sheet and gradually expensed over time as the coverage period elapses. This accounting treatment aligns with the matching principle, ensuring that costs are matched with the revenues they help generate. For instance, a company paying $12,000 annually for insurance in January would initially record this as a prepaid asset. Each month, $1,000 is expensed, reflecting the portion of insurance consumed, while the remaining balance stays on the balance sheet as an asset.

The distinction between prepaid insurance and expenses becomes clearer when examining their impact on financial statements. Expenses directly reduce net income on the income statement, whereas prepaid insurance initially increases assets without affecting income. Over time, as the prepaid insurance is expensed, it gradually reduces the asset account and shifts the cost to the income statement. This staggered recognition ensures that financial statements accurately reflect the economic reality of the transaction. For example, a small business owner who prepays $6,000 for six months of insurance would see an asset of $6,000 initially, with $1,000 expensed monthly, preserving the integrity of both the balance sheet and income statement.

From a practical standpoint, understanding this difference is crucial for accurate financial planning and reporting. Misclassifying prepaid insurance as an expense can distort a company’s financial health, making it appear less profitable or liquid than it actually is. For instance, a startup with limited cash flow might prepay $10,000 for a year of liability insurance. If this is incorrectly expensed in the first month, the company’s net income would plummet, and its cash reserves would appear depleted. Proper classification ensures that stakeholders, including investors and lenders, receive a true and fair view of the company’s financial position.

A comparative analysis highlights the temporal nature of prepaid insurance versus expenses. Expenses are transient, reflecting costs incurred and benefits received within a single accounting period. Prepaid insurance, however, spans multiple periods, embodying a long-term benefit. Consider a retail store that prepays $24,000 for two years of property insurance. This payment is not an immediate expense but an investment in future protection. Each month, $1,000 is expensed, aligning the cost with the period it benefits. This approach contrasts sharply with operational expenses like rent or utilities, which are fully recognized in the month they are paid.

In conclusion, the difference between prepaid insurance and expenses lies in their timing and treatment. Prepaid insurance is an asset because it provides future benefits, while expenses represent immediate costs. By recognizing prepaid insurance as an asset and expensing it over time, businesses adhere to accounting principles that enhance financial transparency and accuracy. This distinction is not merely theoretical but has tangible implications for financial management, reporting, and decision-making. Whether you’re a business owner, accountant, or investor, grasping this concept is essential for interpreting financial statements correctly and making informed choices.

Understanding Insurance 1099: Tax Implications and Reporting Requirements

You may want to see also

Frequently asked questions

Prepaid insurance refers to insurance premiums paid in advance for coverage that extends into future accounting periods. It is considered an asset because it represents a future economic benefit that the company has already paid for but has not yet fully utilized.

Prepaid insurance is recorded as a current asset on the balance sheet because it provides benefits within the next 12 months. It is reported under the "Prepaid Expenses" or "Other Current Assets" section.

Prepaid insurance is not treated as an expense immediately because it follows the matching principle of accounting. The expense is recognized over the period the insurance coverage is active, not at the time of payment.

As the insurance coverage period progresses, the prepaid insurance asset is reduced, and the corresponding amount is recognized as an insurance expense. This is typically done through monthly adjusting entries.

Once the coverage period ends, the prepaid insurance asset is fully expensed, and its balance on the balance sheet is reduced to zero. No further adjustments are needed.