Speeding tickets are some of the most common traffic violations, and they can have a significant impact on your insurance rates and your ability to get insured. The impact of a speeding ticket on your insurance depends on a number of factors, including the state in which the violation occurred, the speed you were travelling at, and your insurance company and history. In most states, speeding tickets will stay on your record for three to five years, but this can differ between states and insurers.

| Characteristics | Values |

|---|---|

| How long before a ticket goes away on insurance | 3-5 years |

| How long before a ticket is removed from a driving record | 3-5 years |

| How long before points are removed from a driving record | 3 years |

| How to remove a ticket from a driving record | Take a defensive driving course, wait until the points expire |

| How to reduce the number of points on a driving record | Take a traffic school course, don't get another violation for three years |

| How long before a ticket is removed from an MVR | Varies, but it can be removed after three years |

| How long before a ticket affects insurance rates | Immediately, for 3-5 years, or until the points on the driving record expire |

| How much insurance rates increase after a ticket | $320-$460 per year, $342 for speeding in a school zone, $767 for an at-fault collision claim, 13% in Texas, 52% in Michigan |

Explore related products

What You'll Learn

- Speeding tickets can remain on your record for up to five years

- The cost of insurance increases after a speeding ticket

- Non-moving violations, like parking tickets, typically don't affect insurance rates

- Insurance companies may consider you a high-risk driver after multiple tickets

- Taking a defensive driving course can help reduce the negative impact of a ticket

![]()

Speeding tickets can remain on your record for up to five years

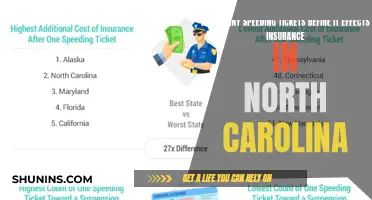

Speeding tickets are some of the most common traffic violations issued each year, and they can also be among the most expensive. The impact of a speeding ticket on your insurance depends on the law in your state. In most of the U.S., speeding tickets and the associated points will stay on your record for three to five years, depending on the state and the severity of the violation. Each state has a different point system and requirements for the amount of time that must pass before points expire.

Some states, like Delaware and New Jersey, allow drivers to take a traffic school or defensive driving course to reduce the number of points on their record or remove them entirely. In Delaware, for example, completing a defensive driving course will earn you three credits that can reduce the negative consequences of moving violations, such as higher insurance costs. In other states, the only way to remove points from your record is to avoid getting another violation for a certain period, typically three years.

The more speeding tickets you accumulate, the more likely your car insurance rates will increase, and the higher that increase will be. If you get two or more speeding tickets within three years, you are likely to see an insurance rate increase. However, if you only receive one speeding ticket during this period, your insurance rate may not be affected at all.

In addition to the number of tickets, several other factors influence the price of insurance after a speeding ticket, including the state in which the violation occurred, the speed at which you were travelling, and your insurance company, driving record, and insurance history. For example, in Texas, car insurance rates increase by about 13% on average after a speeding ticket, while in Michigan, drivers can expect a much higher increase of approximately 52%.

U.S.A.A. Auto Insurance: Understanding Vandalism Coverage

You may want to see also

Explore related products

![]()

The cost of insurance increases after a speeding ticket

Speeding tickets are some of the most common traffic violations, but they can also be the most expensive. The cost of insurance will likely increase after a speeding ticket, and this increase can last for several years. The exact amount that insurance goes up depends on several factors, including your driving history, where you live, and your insurance company's rules.

On average, a speeding ticket will increase your insurance rates by around 20% or $41 per month. However, this can vary significantly depending on your state. For example, California has the largest increase in insurance rates after a speeding ticket, with rates going up by 43%. Drivers in Missouri, New York, and West Virginia see the smallest increase in rates, at just 15%. Texas drivers also get a relatively low increase of 13%, while Michigan drivers experience a much higher increase of about 52-54%.

The number of speeding tickets you have also affects the cost of insurance. The more tickets you get, the more your insurance rates will increase. For example, drivers with two tickets pay 67% more for full coverage, while those with three tickets pay twice as much as drivers with a clean record.

There are ways to mitigate the impact of a speeding ticket on your insurance costs. You can shop around for a cheaper insurance company or take a driver education or defensive driving course to reduce your rates. Some states, like Delaware and New Jersey, allow you to take a traffic school course to reduce the number of points on your record. In some cases, you may even be able to fight the ticket in court or ask the judge for ways to keep it off your record.

Foreign Visitors: Are They Covered by My Auto Insurance?

You may want to see also

Explore related products

![]()

Non-moving violations, like parking tickets, typically don't affect insurance rates

However, non-moving violations may affect your insurance rates if you fail to address them. For example, failing to pay several parking tickets could lead to a rate increase. Additionally, insurance companies treat violations differently, so while one insurer may not raise your rates due to several non-moving violations, another may consider it a sign of risky behaviour and adjust your car insurance costs accordingly.

It's important to note that moving violations, such as speeding tickets, can impact your insurance premiums. The degree to which your rates may be affected depends on the severity of the infraction, your driving record, and other factors such as your age and location. Speeding tickets can stay on your record for three to five years in most of the US, affecting your driver's license status and car insurance premiums. The more speeding tickets you get, the more likely your car insurance rates will increase, and the higher that increase will be.

To mitigate the impact of a speeding ticket on your insurance rates, you can shop around for insurance quotes from different providers, as each company calculates premiums using its own individual system. Additionally, taking a defensive driving course or a traffic school course (available in some states like Delaware and New Jersey) can help reduce the negative impact of moving violations and lower your insurance costs.

Auto Insurance: Stacked vs. Non-Stacked, What's the Difference?

You may want to see also

Explore related products

![]()

Insurance companies may consider you a high-risk driver after multiple tickets

Multiple traffic tickets can cause insurance companies to consider you a high-risk driver, which can result in higher insurance premiums or even denial of coverage. The number of violations or citations you've received is typically the first thing insurers look at when assessing your risk level. Each infraction usually results in a rate hike, and the type and number of violations push you further into high-risk territory.

In most states, speeding tickets and the associated points will remain on your record for three to five years, after which they will no longer affect your insurance rates. However, the length of time a ticket stays on your record can vary depending on the state you live in and the severity of the violation. For example, a DUI conviction may remain on your record for longer than a speeding ticket, affecting your insurance costs accordingly.

If you're considered a high-risk driver, you have a few options for obtaining insurance coverage. You can stick with a standard insurance company, but you'll likely pay higher rates for better coverage and service. Alternatively, you can turn to a non-standard carrier that caters to high-risk customers, although they may have poorer reviews and fewer perks. Some of the best insurance companies for high-risk drivers include USAA, State Farm, Erie, Geico, Progressive, and Nationwide.

To mitigate the impact of multiple tickets on your insurance rates, you can take a defensive driving course, which can help reduce the number of points on your record and demonstrate to insurers that you're taking steps to improve your driving. Improving your credit score can also help lower your insurance costs, as those with poor credit are often deemed high-risk. Additionally, shopping around and comparing quotes from multiple insurers can help you find the most affordable coverage as a high-risk driver.

Understanding Auto Insurance: Exploring Coverage Categories

You may want to see also

Explore related products

![]()

Taking a defensive driving course can help reduce the negative impact of a ticket

In most US states, speeding tickets and the points associated with them will remain on your record for three to five years. The exact number varies from state to state and depends on the severity of the violation. Speeding tickets are some of the most common traffic violations, and they can significantly impact your insurance rates and driver's license status.

For example, in Texas, a driving safety course, also known as a defensive driving class, can be used to dismiss a traffic citation or obtain insurance discounts. Similarly, in Georgia, a Driver Improvement course (which is equivalent to a Defensive Driving course) can be taken for points reduction, driver's license reinstatement, or insurance premium reduction.

It's important to note that each state has its own system for handling speeding tickets and defensive driving courses. While some states, like Delaware and New Jersey, allow the reduction of points through traffic school or defensive driving courses, others may require a certain period without any violations to remove points from your record. Additionally, the impact of an out-of-state ticket may vary depending on the state where the violation occurred and your home state's regulations.

To summarise, taking a defensive driving course can be a valuable tool to mitigate the negative consequences of a speeding ticket. It can help reduce points on your license, lower insurance rates, prevent future accidents, and even keep your driving record clean in some states. However, it's essential to understand the specific regulations and options available in your state to make an informed decision.

Auto Insurance and Stolen Wheels: What's the Verdict?

You may want to see also

Frequently asked questions

Speeding tickets can remain on your record for up to three to five years, depending on the state. During this time, your insurance rates may increase, and the more tickets you accumulate, the higher the increase will be.

The consequences of receiving a ticket vary depending on the state and the insurer. In some cases, your insurer may consider you a high-risk driver and increase your rates or even refuse to write you a policy.

Yes, in some states, you can take a defensive driving or traffic school course to reduce the number of points on your record or remove a speeding ticket from your permanent record. Shopping around for insurance quotes can also help you find a more affordable rate after receiving a ticket.

In addition to the number of tickets, the speed at which you were travelling, your driving record, insurance history, and the policies of your specific insurance company and state can all impact your insurance rates after receiving a ticket.