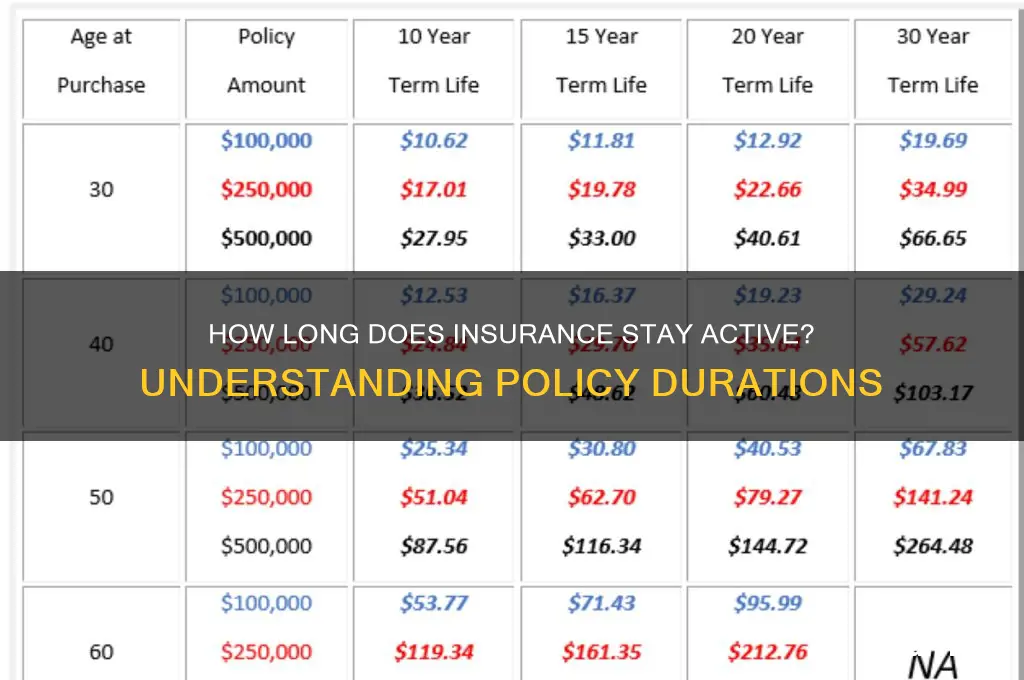

Understanding how long insurance stays active is crucial for policyholders to ensure continuous coverage and avoid gaps in protection. The duration of an insurance policy’s active status varies depending on the type of insurance, such as health, auto, life, or homeowners, and the terms outlined in the policy agreement. Typically, policies are active for a specified term, ranging from six months to a year for auto and homeowners insurance, while health insurance often aligns with annual enrollment periods. Life insurance policies may remain active for the insured’s lifetime or a predetermined term. It’s essential to review policy details, including renewal dates and conditions for cancellation or lapse, to maintain active coverage and address any changes in circumstances that might affect the policy’s status.

Explore related products

What You'll Learn

- Policy Expiration Dates: Understand when your insurance coverage ends based on policy terms

- Grace Periods: Learn how long coverage remains active after missing a premium payment

- Lapsed Policies: Discover how long a policy stays active after lapsing before termination

- Renewal Processes: Explore how renewing on time keeps your insurance continuously active

- Cancellation Terms: Know how long coverage lasts after initiating a policy cancellation

![]()

Policy Expiration Dates: Understand when your insurance coverage ends based on policy terms

Insurance policies are not eternal; they come with a predefined lifespan, and understanding this timeline is crucial for policyholders. The duration of an insurance policy's active status varies significantly depending on the type of insurance and the terms agreed upon at the time of purchase. For instance, auto insurance policies typically last for six months or a year, after which they require renewal. In contrast, life insurance policies can span decades, often tailored to cover specific periods of an individual's life, such as until retirement or the maturity of dependents. Health insurance plans, especially in regions with annual enrollment periods, usually align with a calendar year, expiring on December 31st unless renewed.

The expiration date of a policy is more than just a deadline; it’s a critical component of your financial and risk management strategy. Missing this date can lead to a lapse in coverage, leaving you vulnerable to unforeseen expenses. For example, a homeowner without active insurance during a natural disaster could face catastrophic financial losses. To avoid such scenarios, policyholders should mark their calendars well in advance of the expiration date and initiate the renewal process early. Some insurers offer grace periods, typically 30 days, during which coverage remains active even if the premium hasn’t been paid, but relying on this is risky and not universally applicable.

Renewing a policy isn’t always a passive process. Insurers may reassess your risk profile, leading to changes in premiums or coverage terms. For instance, a driver with multiple traffic violations may face higher auto insurance rates upon renewal. Similarly, health insurance premiums can increase based on age or changes in health status. It’s essential to review the renewal terms carefully and compare them with other available options. Some policies, like term life insurance, may allow conversion to a permanent policy before expiration, providing an opportunity to extend coverage without reapplying.

Proactive management of policy expiration dates involves more than just paying attention to deadlines. It requires a strategic approach to ensure continuous coverage at the best possible terms. For example, bundling multiple policies with the same insurer can sometimes lead to discounts and synchronized renewal dates, simplifying management. Additionally, setting up automatic payments or enrolling in paperless notifications can help prevent oversight. For those with complex insurance needs, consulting an insurance broker can provide tailored advice on optimizing coverage and managing expirations effectively.

In conclusion, understanding policy expiration dates is a cornerstone of responsible insurance management. It’s not just about knowing when coverage ends but also about anticipating changes, exploring options, and taking proactive steps to maintain uninterrupted protection. By staying informed and organized, policyholders can navigate the complexities of insurance expirations with confidence, ensuring they remain covered when it matters most.

Life Insurance Exam Results: How Long to Wait?

You may want to see also

Explore related products

$45.59 $59.99

![Life Assurance, Validity and Non-Validity of Life Policies. [Repr., with Additions, from Life Assurance, an Historical Account. Followed By] Opinions of the Press [On This 1849 Leather Bound](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Grace Periods: Learn how long coverage remains active after missing a premium payment

Missing a premium payment doesn’t immediately void your insurance coverage. Most policies include a grace period, a temporary safety net that keeps your coverage active even after the payment due date has passed. This period typically lasts between 10 and 30 days, depending on the insurer, policy type, and state regulations. For example, health insurance plans under the Affordable Care Act (ACA) mandate a minimum 90-day grace period for individuals receiving subsidies, while auto insurance policies often offer a shorter 10- to 15-day window. Understanding your policy’s grace period is critical to avoiding unintended lapses in coverage.

During the grace period, your insurance remains active, but it’s not a free pass. Insurers may charge late fees or interest on the overdue amount, and failure to pay within this window can result in policy cancellation. For instance, life insurance policies often revert to a "lapse status" after the grace period ends, requiring reinstatement, which may involve medical exams or higher premiums. Similarly, auto insurance cancellations can lead to legal penalties for driving uninsured and potential rate increases when you reapply. Proactive communication with your insurer during this time can sometimes lead to payment extensions or alternative arrangements.

Grace periods vary significantly by policy type and jurisdiction. Health insurance often has the longest grace periods due to regulatory protections, while homeowners and renters insurance typically offer shorter windows. State laws also play a role; California, for example, requires a 30-day grace period for health and auto insurance, whereas Texas mandates only 10 days for auto policies. Always review your policy documents or contact your insurer to confirm the exact duration and terms of your grace period. Ignoring this detail could leave you unprotected when you need coverage most.

To maximize the benefit of a grace period, act swiftly. Set payment reminders, automate payments if possible, and prioritize settling the overdue amount before the grace period expires. If financial hardship prevents timely payment, reach out to your insurer immediately. Many companies offer hardship programs or payment plans to help policyholders avoid cancellation. Additionally, keep detailed records of all communications and payments to dispute any wrongful terminations. A grace period is a temporary solution, not a long-term strategy, so use it wisely to maintain continuous coverage.

Incentive Life Insurance: Understanding the Basics

You may want to see also

Explore related products

$8.27 $12.99

![]()

Lapsed Policies: Discover how long a policy stays active after lapsing before termination

A lapsed insurance policy doesn’t immediately vanish into thin air. Most insurers build in a grace period, typically 30 to 60 days, during which the policy remains technically active despite missed payments. This window is designed to give policyholders a chance to catch up on premiums and avoid termination. For example, a life insurance policy with a 31-day grace period would still provide coverage if the policyholder dies within that timeframe, even if the premium was overdue. However, this grace period varies by insurer, policy type, and state regulations, so it’s crucial to review your policy’s terms.

The grace period isn’t a free pass—it’s a temporary reprieve. During this time, the insurer may charge interest on the unpaid premium, and coverage remains contingent on payment before the grace period expires. If the policyholder fails to pay by the end deadline, the policy officially terminates. For instance, a health insurance policy might lapse after 30 days of non-payment, but the insurer could still reinstate it within the grace period if the premium is settled. Beyond this point, reinstatement may require reapplication, medical underwriting, or higher premiums, depending on the insurer’s rules.

Not all policies handle lapses uniformly. Permanent life insurance, like whole life, often includes a cash value that can be used to cover premiums temporarily, potentially extending the active period beyond the grace period. In contrast, term life insurance typically terminates immediately after the grace period ends. Similarly, auto insurance policies may lapse faster, sometimes within 10 to 30 days, due to higher risk exposure. Understanding these differences is key to managing your coverage effectively.

To avoid the pitfalls of a lapsed policy, take proactive steps. Set up automatic payments to ensure premiums are paid on time. If financial hardship strikes, contact your insurer immediately—some offer payment plans or temporary reductions in coverage to keep the policy active. For example, reducing the death benefit on a life insurance policy can lower premiums temporarily. Additionally, keep an eye on policy expiration dates and renewal notices to prevent accidental lapses.

In conclusion, a lapsed policy doesn’t mean immediate termination. The grace period offers a critical buffer, but its duration and consequences vary widely. By understanding your policy’s specifics and taking preventive measures, you can protect your coverage and avoid the complications of reinstatement or loss of benefits. Always read the fine print and act swiftly if payments are missed—your policy’s survival depends on it.

Beating Nicotine Tests for Life Insurance

You may want to see also

Explore related products

![]()

Renewal Processes: Explore how renewing on time keeps your insurance continuously active

Insurance policies are not perpetual; they require timely renewal to maintain uninterrupted coverage. Missing a renewal deadline can lead to a lapse in your policy, leaving you vulnerable to financial risks. For instance, auto insurance typically requires annual renewal, while health insurance may follow a calendar year cycle. Understanding your policy’s renewal period is the first step in ensuring continuous protection. Most insurers send reminders 30 to 60 days before expiration, but relying solely on these notifications can be risky, especially if they’re delayed or overlooked.

Renewing on time isn’t just about avoiding a gap in coverage—it’s also about preserving policy benefits. Many insurance plans, such as life or health insurance, accumulate value or benefits over time. A lapse could reset these advantages, forcing you to start over. For example, a health insurance policy with a pre-existing condition clause might require a new waiting period if coverage lapses. Similarly, term life insurance premiums often increase with age, so a lapse could result in higher costs upon reinstatement. Timely renewal ensures you retain these long-term benefits without additional financial burden.

The renewal process itself varies by insurer and policy type. Some companies offer automatic renewal with payment via a saved credit card or bank account, while others require manual submission of forms and payments. For instance, renters insurance often allows autopay, but certain specialty policies, like flood insurance, may demand annual re-evaluation and manual renewal. Familiarize yourself with your insurer’s process and set personal reminders to avoid last-minute complications. Pro tip: Schedule renewal tasks in your calendar 45 days before expiration to allow time for processing and potential issues.

Renewing on time also impacts your relationship with the insurer. Consistent renewal demonstrates reliability, which can lead to loyalty discounts or smoother claim processing. Conversely, frequent lapses may flag you as a high-risk policyholder, potentially resulting in higher premiums or denied coverage. For example, auto insurers often view lapsed policies as a red flag, assuming the driver may be uninsured or financially unstable. By renewing promptly, you maintain a positive insurance history, which can translate to long-term savings and better policy terms.

Finally, consider the broader implications of continuous coverage. In some cases, such as auto or health insurance, maintaining an active policy is legally required. Lapses can result in fines, license suspension, or difficulty securing future coverage. For instance, the Affordable Care Act imposes penalties for gaps in health insurance exceeding 3 months. Beyond legal consequences, continuous coverage provides peace of mind, ensuring you’re protected against unforeseen events. Renewing on time is a small but critical action that safeguards your financial and legal well-being.

Mastering Insurance Updates: A Step-by-Step Guide to Accurate Filing

You may want to see also

Explore related products

![]()

Cancellation Terms: Know how long coverage lasts after initiating a policy cancellation

Understanding the duration of insurance coverage after initiating a policy cancellation is crucial for avoiding gaps in protection or unnecessary expenses. Once you request cancellation, the policy typically remains active until the end of the billing cycle or a specific date outlined in the cancellation terms. For instance, auto insurance policies often provide coverage until the last day of the paid period, even if you cancel mid-month. However, health insurance plans might terminate coverage immediately upon cancellation, depending on the insurer’s policies and state regulations. Always review your policy’s fine print to confirm the exact timeline.

The cancellation process varies by insurer and policy type, making it essential to act strategically. For example, if you’re switching providers, coordinate the cancellation of your old policy with the activation of the new one to ensure continuous coverage. Some insurers offer a grace period, typically 30 days, during which you can reverse the cancellation if you change your mind. However, this grace period is not universal, so don’t assume it applies without verifying. Life insurance policies, particularly term life, may allow you to reinstate coverage within a specific timeframe if you cancel due to missed payments, but this often requires additional fees or proof of insurability.

One critical aspect often overlooked is the impact of cancellation on future premiums and eligibility. Canceling a policy mid-term can sometimes result in a short-rate penalty, where the insurer charges a higher rate for the time the policy was active. Additionally, frequent cancellations or gaps in coverage may signal risk to future insurers, potentially increasing premiums or limiting options. For example, canceling a homeowners insurance policy mid-term might raise red flags for future providers, who may question the stability of your coverage history. To mitigate this, consider exhausting the paid period before canceling or discussing alternatives with your insurer.

Practical tips can help navigate the cancellation process smoothly. First, notify your insurer in writing to document your request and avoid disputes over the cancellation date. Second, if you’re canceling due to dissatisfaction, explore options like adjusting coverage limits or deductibles before terminating the policy entirely. Third, for policies tied to loans or leases (e.g., auto or mortgage insurance), ensure compliance with lender requirements to avoid forced coverage at higher rates. Finally, keep a record of all communications and confirmations related to the cancellation for future reference.

In conclusion, knowing how long your insurance remains active after initiating cancellation is a matter of diligence and planning. By understanding your policy’s specific terms, coordinating transitions carefully, and considering the long-term implications, you can avoid pitfalls and maintain financial security. Always treat cancellation as a structured process rather than a spontaneous decision, and leverage available resources, such as customer service representatives or insurance brokers, to clarify uncertainties.

What to Do When You Forget to Exchange Insurance Info After an Accident

You may want to see also

Frequently asked questions

Car insurance typically stays active for the policy term, which is usually 6 or 12 months, depending on your agreement. As long as you continue to pay your premiums on time, your coverage remains active for the duration of the term.

Health insurance usually has a grace period, often 30 days, after a missed payment. If you don’t pay within this period, your coverage may lapse. Check your policy or contact your insurer for specific details.

For term life insurance, coverage ends immediately if you stop paying premiums. Whole life insurance may have a cash value that can keep the policy active for a limited time, but it varies by policy. Always review your policy terms for specifics.