How long an accident affects your auto insurance rates depends on a variety of factors, including the state you live in, whether you were at fault, the severity of the accident, and the nature of any violations. Typically, insurance companies will increase your premium after an accident, with at-fault accidents resulting in higher surcharges than not-at-fault accidents. This practice, known as surcharging, usually lasts for three to five years, though some companies may factor in accidents for longer. The surcharge will often decrease over time if you avoid future accidents.

| Characteristics | Values |

|---|---|

| How long do accidents affect insurance rates? | 3-5 years |

| How long does an accident stay on your driving record? | Varies by state and insurer |

| How much do insurance rates increase after an accident? | $840 per year on average for full coverage |

| How much do insurance rates increase after an at-fault accident? | $80 per month on average for full coverage |

| How much do insurance rates increase after an accident (as a %)? | 40%-49% on average |

Explore related products

What You'll Learn

![]()

Accident forgiveness

Accidents can affect your insurance rates for up to three to five years, depending on your insurance company, state regulations, and the nature and severity of the accident. However, accident forgiveness can help prevent your insurance rates from increasing after a car accident.

For example, Progressive offers three types of accident forgiveness: Small Accident Forgiveness, Large Accident Forgiveness, and Progressive Accident Forgiveness. Small Accident Forgiveness is automatically included for new customers in most states, where the insurance rate stays the same for the first claim that is less than or equal to $500. Large Accident Forgiveness is available to customers who have been with Progressive for at least five years and have remained accident and violation-free during this period. With Large Accident Forgiveness, your rates won't increase even if the total claim exceeds $500. Progressive Accident Forgiveness can be purchased when buying or renewing your policy, and you may have one eligible accident forgiven per policy period.

GEICO also offers Accident Forgiveness, which can be earned or purchased in states where it is available. This benefit applies per policy, not per driver, and can be used by any eligible driver on the policy once.

To be eligible for accident forgiveness, you typically need to have a clean driving record for a specified period, often three to five years. It is worth noting that accident forgiveness may not apply to drivers under a certain age, such as those under 21 years old.

Back Window Damage: What Your Auto Insurance Covers

You may want to see also

Explore related products

![]()

How to lower insurance rates

An accident on your record will generally affect your insurance rates for three to five years, depending on your insurance company and state's regulations, as well as the nature and severity of the accident. Here are some ways to lower your insurance rates after an accident:

Shop around for quotes

Compare quotes from different insurance companies to see which company is offering the best rates for you. Your accident may be treated differently by different companies, so it's worth getting multiple quotes to find the most affordable coverage.

Look for discounts

Insurance companies offer a variety of discounts that you may be eligible for, such as:

- Usage-based insurance (UBI): Many companies offer a discount for signing up for their UBI program, which monitors and rates your driving practices through your smartphone. Maintaining a good driving score can lead to further savings.

- Low-mileage discounts: If your work commute is shorter than it used to be, inform your insurance company. You may qualify for a low-mileage discount.

- Bundling policies: If you haven't already, consider consolidating your insurance policies with one company. Most companies offer multipolicy discounts if you bundle your car insurance with other policies like homeowners or renters insurance.

- Defensive driver discount: Taking a qualified defensive driving course may earn you a discount in some states.

- Driver affiliations: Some insurers offer discounts for certain occupations (e.g., first responders, military members) or memberships in specific groups such as alumni or professional associations.

- Safe vehicle discounts: If your car has safety features like airbags, anti-lock brakes, or anti-theft devices, you may be eligible for a discount.

- Hybrid/electric car discounts: Insurers are increasingly offering discounts for environmentally friendly vehicles.

- Payment discounts: Paying your premium in full or opting for an automatic payment plan can sometimes lead to savings.

- Online quote discounts: Some insurers offer discounts if you request a quote and purchase the policy online.

Adjust your coverage

While you don't want to compromise essential coverage, you may be able to increase your collision and/or comprehensive deductibles to lower your premium. Just make sure that you choose deductibles that you can comfortably afford in case of an emergency.

Improve your credit

If you live in a state that allows insurance companies to consider your credit-based insurance score when determining rates, work on improving your credit standing. This includes staying within a personal budget, paying off debts, and addressing any discrepancies on your credit report.

Auto Insurance and Bike Coverage: What Cyclists Need to Know

You may want to see also

Explore related products

![]()

At-fault vs no-fault accidents

The impact of an accident on your auto insurance rates depends on several factors, including whether you were at fault, the severity of the accident, your insurance company, and your state's regulations. Typically, at-fault accidents result in higher insurance rates compared to no-fault accidents. Here's a more detailed look at the differences between at-fault and no-fault accidents and their impact on insurance rates:

At-Fault Accidents:

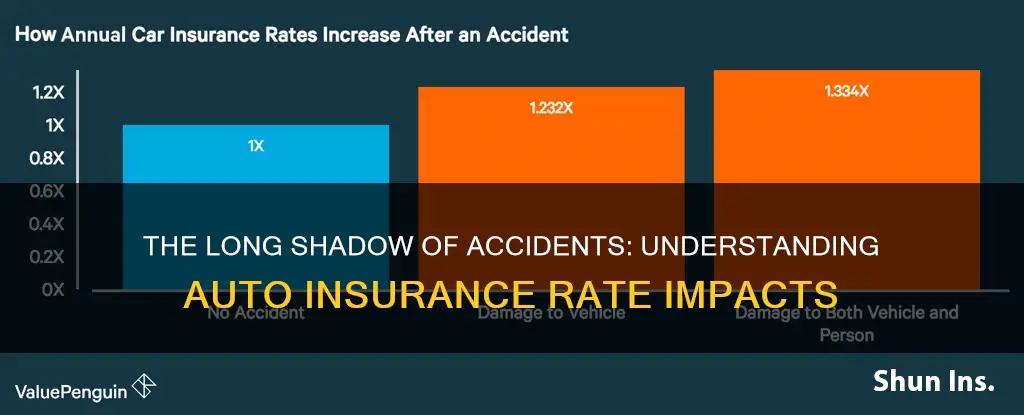

In most states, when an accident occurs, one party is considered "at-fault." This means they are responsible for covering the injuries and property damage of the other driver and their passengers, usually through their liability insurance. At-fault accidents almost always lead to an increase in insurance rates, and the severity of the accident will impact the surcharge. For example, a major accident will result in a higher surcharge than a minor one. The surcharge will typically appear as an additional charge on your billing statement when you renew your policy after the accident.

No-Fault Accidents:

In some states, known as "no-fault" states, medical bills resulting from an accident are covered by each driver's individual Personal Injury Protection (PIP) coverage, regardless of who is at fault. In these states, drivers must purchase car insurance with PIP coverage to pay for their own injuries. No-fault insurance typically covers a portion of the driver's medical bills and lost income, but it does not include compensation for non-economic damages, such as pain and suffering. While no-fault accidents may not impact your insurance rates as significantly as at-fault accidents, they can still result in an increase, depending on your state and insurer. Additionally, in no-fault states, drivers who suffer severe injuries may have the right to sue the at-fault driver under certain conditions.

Duration of Rate Impact:

Accidents generally affect your insurance rates for three to five years, depending on your insurance company and state regulations. After this period, your rates should return to normal, provided you avoid any further accidents or violations.

U-Turn: USAA Auto Insurance and SR22 Forms

You may want to see also

Explore related products

![]()

How long accidents stay on your record

Accidents will typically stay on your record for three to five years, but this can vary depending on your location and insurance provider.

In the US, insurance companies in most states will look back at three to five years of your driving history when determining your car insurance rate. However, this timeframe can differ depending on your specific location and insurer. For example, in California, accidents and minor violations stay on your driving record for three years, while in Florida, they remain on your record for three to five years.

The length of time an accident stays on your record also depends on the violations associated with the incident. For instance, in California, accidents involving more serious violations, such as a DUI conviction, will stay on your record for ten years. In Florida, alcohol-related violations are tracked for 75 years.

It's important to note that even if you weren't at fault for the accident, it might still count against you and affect your insurance rates. This varies by company and state. Checking your state's department of motor vehicles website can provide more specific information on how long accidents stay on your record in your location.

Does Towing a Boat Affect Your Auto Insurance?

You may want to see also

Explore related products

![]()

Insurance rates by state

The cost of car insurance varies significantly from state to state, with the average annual premium for full coverage ranging from $1,385 in Vermont to $8,232 in New York. The national average for full coverage is $2,278 per year, and $621 per year for minimum coverage.

The cost of car insurance in each state is influenced by a range of factors, including road conditions, the number of licensed drivers, traffic density, the cost of living, and the percentage of uninsured drivers.

- Alabama: $1,965

- Alaska: $2,292

- Arizona: $2,547

- Arkansas: $2,154

- California: $2,554

- Colorado: $2,937

- Connecticut: $2,411

- Delaware: $2,337

- Florida: $3,220

- Georgia: $2,469

- Hawaii: $1,581

- Idaho: $1,588

- Illinois: $2,100

- Indiana: $1,606

- Iowa: $1,775

- Kansas: $2,524

- Kentucky: $2,613

- Louisiana: $4,357

- Maine: $1,460

- Maryland: $2,533

- Massachusetts: $1,640

- Michigan: $4,067

- Minnesota: $2,349

- Mississippi: $2,010

- Missouri: $2,575

- Montana: $2,493

- Nebraska: $2,306

- Nevada: $3,870

- New Hampshire: $1,805

- New Jersey: $2,452

- New Mexico: $2,177

- New York: $4,112

- North Carolina: $1,827

- North Dakota: $1,781

- Ohio: $1,482

- Oklahoma: $2,535

- Oregon: $1,872

- Pennsylvania: $3,909

- Rhode Island: $2,667

- South Carolina: $2,223

- South Dakota: $1,701

- Tennessee: $2,003

- Texas: $2,386

- Utah: $2,000

- Vermont: $1,539

- Virginia: $2,000

- Washington: $1,564

- Washington, D.C.: $2,348

- West Virginia: $1,952

- Wisconsin: $1,718

- Wyoming: $1,695

U.S. Civilian Auto Insurance: Can You Join USAA?

You may want to see also

Frequently asked questions

Accidents generally affect your insurance rates for three to five years, depending on your insurance company and state's regulations, as well as the nature and severity of the accident.

The main factors are the insurance company and state regulations, as well as the nature and severity of the accident. Some states limit how long insurers can consider at-fault accidents when calculating premiums.

Here are some strategies to lower your insurance rates:

- Compare quotes from different insurance companies and switch providers if you find a better rate.

- Improve your credit score, as it is considered in most states when determining insurance rates.

- Increase your deductible. While this will result in higher out-of-pocket expenses if you file a claim, it can lower your premium.

- Look for discounts offered by insurance companies, such as good student discounts, multi-policy discounts, or usage-based telematics programs.