The question of how many Americans have insurance is a critical aspect of understanding the nation's healthcare landscape. As of recent data, approximately 91% of Americans are covered by some form of health insurance, a significant increase from previous decades due to policy changes like the Affordable Care Act (ACA). This coverage is primarily divided among employer-sponsored plans, Medicaid, Medicare, and individual market plans. However, disparities persist, with about 8.6% of the population, or roughly 28 million people, remaining uninsured, often due to factors such as affordability, eligibility gaps, and state-level policy variations. These numbers highlight both progress and ongoing challenges in achieving universal healthcare access in the United States.

Explore related products

What You'll Learn

![]()

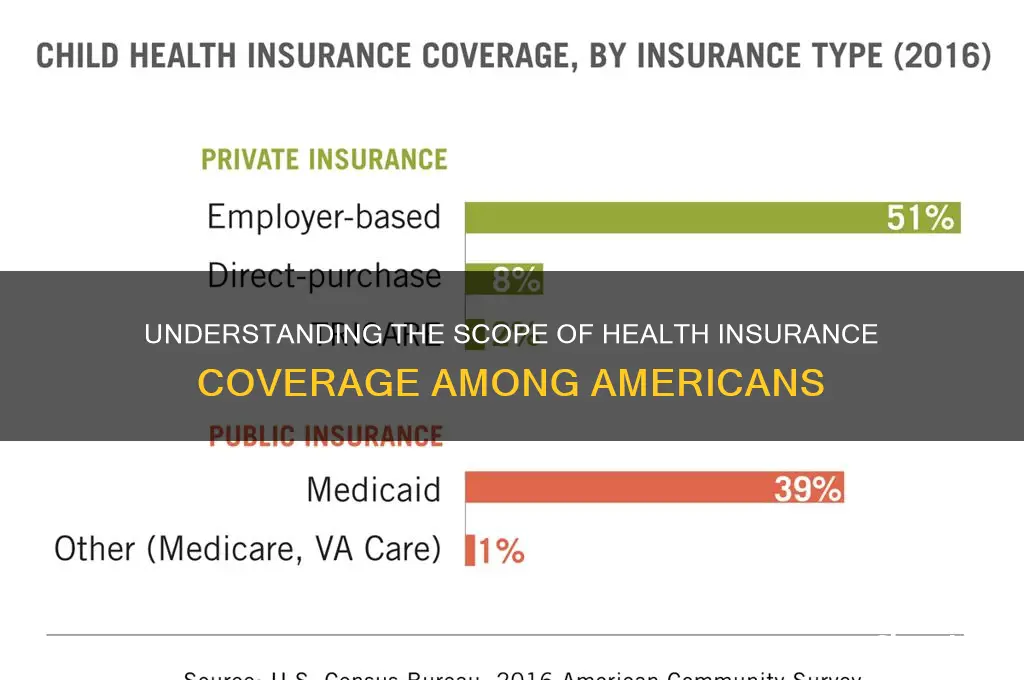

Employer-based health insurance coverage rates among Americans

Employer-based health insurance remains the cornerstone of coverage for millions of Americans, with approximately 157 million individuals, or about 57% of the insured population, relying on plans provided through their workplace. This figure, sourced from the U.S. Census Bureau’s 2022 data, underscores the dominance of this coverage type in the American healthcare landscape. For many, employer-sponsored insurance (ESI) offers a cost-effective way to access healthcare, as employers typically subsidize a significant portion of the premiums. However, this reliance on workplace coverage also highlights vulnerabilities, such as the potential loss of insurance during job transitions or economic downturns.

Analyzing the demographics of ESI reveals disparities in coverage rates. Full-time workers are far more likely to have access to employer-based insurance than part-time employees, with coverage rates of 70% and 24%, respectively. Additionally, industries like finance and professional services boast higher ESI rates, while sectors like hospitality and retail lag behind. These differences reflect broader economic inequalities, as lower-wage workers often face limited access to comprehensive benefits. Age also plays a role, with prime working-age adults (25–54) being the primary beneficiaries of ESI, while younger and older Americans rely more on alternatives like Medicaid or Medicare.

From a policy perspective, the prevalence of employer-based insurance shapes debates about healthcare reform. Advocates argue that ESI provides stability and affordability for many, but critics point to its limitations, such as "job lock," where employees stay in positions solely to retain coverage. The Affordable Care Act (ACA) sought to address some of these issues by expanding individual market options and Medicaid, yet ESI remains the dominant coverage source. Policymakers must balance strengthening ESI with creating viable alternatives to ensure universal access.

For individuals navigating employer-based insurance, understanding plan details is crucial. Key factors to consider include premiums, deductibles, and out-of-pocket maximums, as these vary widely across plans. Employees should also assess network coverage and prescription drug benefits, which can significantly impact overall costs. Open enrollment periods are critical times to review and adjust coverage, especially if life circumstances (e.g., marriage, childbirth) have changed. Practical tips include comparing ESI plans to marketplace options during life transitions and leveraging Health Savings Accounts (HSAs) if available, as they offer tax advantages for medical expenses.

In conclusion, employer-based health insurance is a vital yet complex component of the American healthcare system. Its widespread use reflects both its strengths and weaknesses, from affordability for many to accessibility gaps for others. As the workforce evolves, with the rise of gig economy jobs and remote work, the future of ESI may require adaptation to meet changing needs. For now, it remains a critical lifeline for millions, making informed decision-making essential for maximizing its benefits.

Understanding Life Insurance Coverage: What You Need to Know

You may want to see also

Explore related products

![]()

Percentage of Americans covered by Medicaid or Medicare

As of recent data, approximately 38% of Americans are covered by either Medicaid or Medicare, making these two programs the largest sources of public health insurance in the United States. Medicaid, a joint federal and state program, primarily serves low-income individuals, families, pregnant women, children, and people with disabilities. Medicare, on the other hand, is a federal program designed for individuals aged 65 and older, as well as certain younger people with disabilities. Together, these programs ensure that a significant portion of the population has access to essential healthcare services.

To understand the impact of Medicaid and Medicare, consider the demographics they serve. Medicaid covers about 78 million Americans, including 37 million children, making it a critical safety net for vulnerable populations. Eligibility varies by state, but the Affordable Care Act’s expansion has increased access in many regions. Medicare, covering over 65 million seniors and younger disabled individuals, is divided into parts: Part A (hospital insurance), Part B (medical insurance), and Part D (prescription drug coverage). For those aged 65 and older, Medicare is often the primary source of health insurance, with many supplementing it with private plans or Medicaid for additional coverage.

A comparative analysis reveals the programs’ distinct roles. Medicaid’s eligibility is income-based, with benefits tailored to state policies, while Medicare is age- and disability-based with standardized federal benefits. For example, a 60-year-old with a disability might qualify for Medicare, whereas a low-income family with children would rely on Medicaid. This duality ensures that both short-term financial hardships and long-term health needs are addressed. However, gaps remain, such as the “Medicaid coverage gap” in states that did not expand the program, leaving some low-income adults ineligible for both Medicaid and subsidized marketplace plans.

Practical tips for navigating these programs include understanding enrollment periods. Medicare has specific enrollment windows, such as the Initial Enrollment Period around one’s 65th birthday, while Medicaid allows year-round enrollment for eligible individuals. Beneficiaries should also explore additional coverage options, like Medicare Advantage plans or Medicaid waivers, to address specific health needs. For families, checking state-specific Medicaid guidelines is crucial, as income limits and covered services vary.

In conclusion, Medicaid and Medicare collectively cover nearly 40% of Americans, forming the backbone of the nation’s public health insurance system. By serving distinct populations—low-income individuals and seniors/disabled persons—these programs address diverse healthcare needs. However, awareness of eligibility criteria, enrollment processes, and supplemental options is essential to maximize their benefits. As healthcare policies evolve, staying informed ensures that individuals can leverage these programs effectively.

Understanding CSL in Insurance: Coverage, Limits, and Importance Explained

You may want to see also

Explore related products

![]()

Uninsured rates by age, income, and state

The uninsured rate among Americans varies significantly by age, with younger adults facing higher barriers to coverage. According to the latest data, approximately 14% of adults aged 19 to 25 are uninsured, compared to only 1% of adults aged 65 and older. This disparity is largely due to the availability of Medicare for seniors, while younger adults often struggle with affordability or lack access to employer-sponsored plans. For those in their late teens and early twenties, staying on a parent’s insurance plan until age 26 under the Affordable Care Act (ACA) is a critical option, but many fail to utilize it due to lack of awareness or administrative hurdles.

Income plays a pivotal role in determining insurance status, with lower-income households disproportionately affected. Among individuals living below the federal poverty level, nearly 20% are uninsured, compared to just 5% of those with incomes above 400% of the poverty level. This gap persists despite the ACA’s Medicaid expansion, as 11 states have yet to adopt it, leaving millions of low-income adults in a coverage gap. For those earning slightly above poverty wages, subsidies through the ACA marketplace can reduce premiums, but navigating the application process remains a challenge. Practical tips include using state-based marketplaces for simplified enrollment and seeking assistance from certified navigators.

Geography is another critical factor, as uninsured rates vary widely by state. Texas leads the nation with an uninsured rate of 18%, while Massachusetts boasts the lowest at 3%. Southern and Western states generally have higher uninsured populations, often correlating with non-expansion of Medicaid and lower rates of employer-sponsored coverage. State policies, such as Medicaid work requirements or restrictive eligibility criteria, further exacerbate disparities. For residents in high-uninsured states, exploring community health centers or short-term health plans can provide temporary relief, though these options often lack comprehensive benefits.

Addressing these disparities requires targeted interventions. For younger adults, educational campaigns about ACA provisions and simplified enrollment processes could increase coverage. Expanding Medicaid in non-expansion states would significantly reduce uninsured rates among low-income populations. Policymakers in high-uninsured states should consider state-specific solutions, such as reinsurance programs to lower premiums or public awareness initiatives. Ultimately, understanding these demographic and geographic trends is essential for crafting effective strategies to reduce the number of uninsured Americans.

Cobra Coverage: Life Insurance Benefits Explained

You may want to see also

Explore related products

![]()

Impact of the Affordable Care Act on insurance rates

The Affordable Care Act (ACA), often referred to as Obamacare, has significantly reshaped the American health insurance landscape since its enactment in 2010. One of its primary goals was to reduce the number of uninsured Americans, and it achieved this by expanding Medicaid eligibility and creating health insurance marketplaces. By 2021, the uninsured rate had dropped to approximately 8.6%, a notable decline from the pre-ACA era when over 16% of Americans lacked coverage. This reduction is a direct result of the ACA’s provisions, which made insurance more accessible and affordable for millions.

However, the impact of the ACA on insurance rates is a nuanced issue. While the law aimed to lower costs through mechanisms like subsidies and the elimination of lifetime coverage limits, premiums have continued to rise, albeit at a slower pace than before the ACA. For instance, between 2010 and 2020, average annual premiums for employer-sponsored family coverage increased by about 55%, compared to a 68% increase in the decade prior. This suggests the ACA has had a moderating effect on premium growth, though it hasn’t eliminated cost concerns entirely. Subsidies available through the marketplaces have been crucial in offsetting these increases for eligible individuals, with nearly 90% of marketplace enrollees receiving financial assistance in 2023.

A critical aspect of the ACA’s impact is its role in standardizing insurance benefits and protecting consumers. Before the ACA, insurers could deny coverage based on pre-existing conditions or charge higher rates for women and older adults. The law’s prohibition on these practices has made insurance more equitable but has also contributed to rate adjustments as insurers account for broader risk pools. For example, young and healthy individuals may have experienced premium increases, while those with pre-existing conditions have benefited from guaranteed coverage at standard rates. This redistribution of costs highlights the ACA’s trade-offs in achieving its goals.

To navigate the ACA’s impact on insurance rates, consumers should take proactive steps. First, explore all available options, including employer-sponsored plans, ACA marketplaces, and Medicaid, to find the best value. Second, utilize the subsidies and tax credits available through the marketplaces, which can significantly reduce out-of-pocket costs. For instance, individuals earning up to 400% of the federal poverty level (approximately $54,000 for a single person in 2023) may qualify for premium tax credits. Finally, consider high-deductible health plans paired with health savings accounts (HSAs) for long-term savings, especially if you’re in good health and rarely require medical services.

In conclusion, the ACA has undeniably expanded insurance coverage in the U.S., but its effect on insurance rates is complex. While it has slowed premium growth and introduced consumer protections, costs remain a challenge for many. By understanding the ACA’s mechanisms and leveraging its tools, individuals can make informed decisions to maximize their coverage while managing expenses.

Calculating Your Life Insurance Maturity: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Trends in private health insurance enrollment over the past decade

Over the past decade, private health insurance enrollment in the United States has experienced notable fluctuations, influenced by policy changes, economic shifts, and evolving consumer preferences. According to the Centers for Disease Control and Prevention (CDC), in 2010, approximately 67.3% of Americans under age 65 had private health insurance. By 2020, this figure had dipped slightly to 66.5%, despite the implementation of the Affordable Care Act (ACA), which aimed to expand coverage. This marginal decline underscores the complexity of factors affecting enrollment, including rising premiums and shifting employer-sponsored plans.

One significant trend is the gradual erosion of employer-sponsored insurance (ESI), which remains the primary source of private coverage. Between 2010 and 2020, the percentage of Americans with ESI dropped from 58.9% to 54.4%. This shift can be attributed to employers reducing benefits, increasing employee cost-sharing, and small businesses opting out of providing coverage. Conversely, the individual market, bolstered by ACA’s marketplaces, saw modest growth, particularly among younger adults aged 18–34, who increasingly turned to private plans due to improved affordability and accessibility.

Another critical trend is the impact of Medicaid expansion under the ACA. States that expanded Medicaid saw a reduction in private insurance enrollment among low-income populations, as individuals opted for the more cost-effective public option. For example, in expansion states, private insurance rates among adults aged 18–64 decreased by 2.2 percentage points between 2013 and 2019, compared to a 0.8 percentage point decline in non-expansion states. This dynamic highlights the interplay between public and private coverage and its influence on enrollment trends.

Persuasively, the rise of high-deductible health plans (HDHPs) paired with health savings accounts (HSAs) has reshaped private insurance enrollment. By 2020, over 50% of workers with ESI were enrolled in HDHPs, up from 17% in 2010. While these plans offer lower premiums, they shift more financial risk to consumers, potentially deterring enrollment among those with limited savings. Policymakers and employers must balance cost containment with ensuring plans remain attractive and accessible to a diverse workforce.

In conclusion, the past decade’s trends in private health insurance enrollment reflect a shifting landscape shaped by policy, economic pressures, and consumer behavior. While the ACA expanded coverage options, challenges like declining ESI and the rise of HDHPs highlight persistent gaps. To stabilize enrollment, stakeholders must address affordability, simplify plan choices, and incentivize employers to maintain robust benefits. Practical steps include capping premium increases, expanding subsidies for individual plans, and promoting health literacy to empower consumers to make informed choices.

Eaglesoft Insurance App: Running Claims Against Clients Made Easy

You may want to see also

Frequently asked questions

As of recent data, approximately 91% of Americans have some form of health insurance, covering about 300 million people.

About 66% of Americans with health insurance have private coverage, often through employer-sponsored plans or individual purchases.

Around 8% of Americans, or roughly 28 million people, are uninsured. Common reasons include high costs, lack of employer-provided options, and ineligibility for public programs like Medicaid.