Millions of people worldwide lack access to health insurance, leaving them vulnerable to financial hardship and limited healthcare options. The number of uninsured individuals varies significantly across countries, with factors such as socioeconomic status, employment, and government policies playing a crucial role. In the United States, for instance, despite efforts to expand coverage, a substantial portion of the population remains uninsured, often due to high costs, lack of employer-sponsored plans, or ineligibility for public programs. Globally, low-income countries face even greater challenges, with many citizens unable to afford insurance or relying on inadequate public systems. Understanding the scope of this issue is essential to addressing disparities in healthcare access and ensuring that everyone has the opportunity to lead healthier lives.

Explore related products

What You'll Learn

![]()

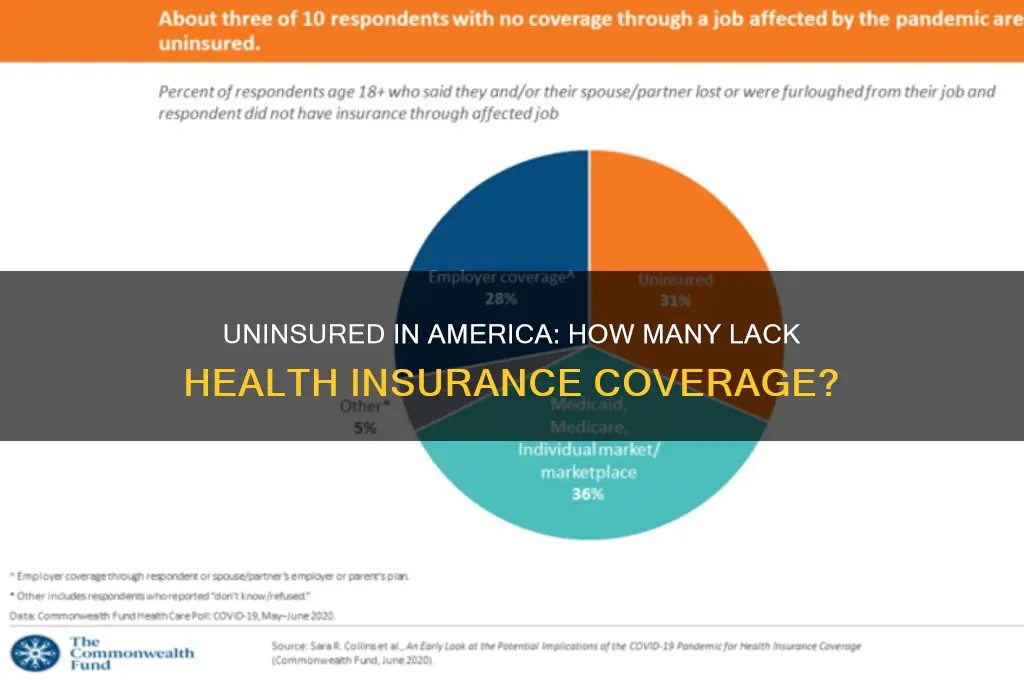

Uninsured rates by income level

Income level is a critical determinant of health insurance coverage, with uninsured rates disproportionately affecting lower-income individuals and families. Data from the U.S. Census Bureau consistently shows that households earning below the federal poverty level (FPL) are more than twice as likely to be uninsured compared to those earning above 400% of the FPL. For example, in 2022, approximately 14.5% of individuals in households earning below 100% of the FPL were uninsured, compared to just 5.8% of those in households earning 400% of the FPL or more. This stark disparity highlights the financial barriers to accessing healthcare for those with limited resources.

Analyzing the trends, the Affordable Care Act (ACA) significantly reduced uninsured rates across all income levels by expanding Medicaid and offering subsidized marketplace plans. However, gaps persist, particularly in states that have not expanded Medicaid. In these states, many low-income adults fall into the "coverage gap," earning too much to qualify for Medicaid but too little to afford private insurance. For instance, in Texas, which has not expanded Medicaid, the uninsured rate for adults in the coverage gap is nearly 25%, compared to 10% in expansion states. This underscores the role of policy decisions in exacerbating or alleviating income-based disparities in coverage.

A comparative perspective reveals that middle-income households (200%–400% of the FPL) often face unique challenges. While they may not qualify for Medicaid, they may still struggle to afford employer-sponsored insurance or marketplace plans, even with subsidies. For example, a family of four earning $100,000 annually (approximately 300% of the FPL) could face premiums exceeding $12,000 per year, a significant financial burden. This group is often referred to as the "forgotten middle," as they are less likely to receive public assistance but may still be priced out of private options.

To address these disparities, practical steps can be taken at both the individual and policy levels. For low-income individuals, enrolling in Medicaid (where available) or exploring subsidized marketplace plans during open enrollment is crucial. Tools like the Healthcare.gov subsidy calculator can help estimate costs. For middle-income households, negotiating employer benefits, such as health savings accounts (HSAs) or flexible spending arrangements (FSAs), can provide some financial relief. Policymakers, meanwhile, should focus on closing the Medicaid coverage gap and expanding premium subsidies to ensure affordability across all income levels.

In conclusion, uninsured rates by income level reveal a clear pattern of inequity, with lower-income individuals bearing the brunt of coverage gaps. While progress has been made, persistent barriers—such as state-level Medicaid expansion decisions and affordability challenges for middle-income households—demand targeted solutions. By addressing these issues through policy reforms and practical strategies, it is possible to move toward a more equitable healthcare system where income does not dictate access to essential coverage.

Group Term Life Insurance: What's a Fair Rate?

You may want to see also

Explore related products

![]()

Geographic disparities in health coverage

In the United States, geographic location significantly influences access to health insurance, creating stark disparities across regions. For instance, Southern states like Texas, Florida, and Georgia consistently report higher uninsured rates compared to the national average. In Texas, approximately 18% of the population lacks health coverage, partly due to the state’s decision not to expand Medicaid under the Affordable Care Act. This contrasts sharply with states like Massachusetts, where only 3% of residents are uninsured, thanks to early adoption of comprehensive health reform and Medicaid expansion. These regional differences highlight how policy decisions at the state level directly impact coverage rates, exacerbating inequalities in access to care.

Analyzing the data reveals that rural areas, regardless of region, face unique challenges in securing health insurance. Rural populations often have fewer job opportunities with employer-sponsored insurance and limited access to Affordable Care Act marketplaces. For example, in states like Mississippi and Alabama, rural counties have uninsured rates exceeding 20%, compared to urban areas within the same states. Additionally, healthcare infrastructure in rural regions is often inadequate, with fewer providers accepting uninsured patients. This double burden of lower insurance rates and reduced healthcare access creates a cycle of poor health outcomes for rural residents, underscoring the need for targeted interventions in these areas.

To address geographic disparities, policymakers must consider region-specific strategies. In states with high uninsured rates, expanding Medicaid could immediately reduce the uninsured population by providing coverage to low-income adults. For example, if Oklahoma were to expand Medicaid, an estimated 150,000 residents could gain coverage. In rural areas, investing in telehealth services and mobile clinics could bridge the gap in healthcare access, while incentivizing providers to practice in underserved regions could improve insurance utilization. Practical steps include increasing funding for community health centers and offering subsidies to rural employers to provide health insurance to workers.

Comparing international models offers additional insights. Countries like Canada and the UK, with universal healthcare systems, eliminate geographic disparities by ensuring coverage regardless of location. While implementing such a system in the U.S. is politically complex, lessons can be drawn from state-level successes. For instance, California’s robust Medicaid program and subsidized insurance marketplace have reduced uninsured rates to 7%, demonstrating the impact of comprehensive policy action. By studying these examples, U.S. policymakers can craft solutions that mitigate geographic disparities and improve health equity nationwide.

Lloyds Insurance Coverage for Notre Dame: Facts and Clarifications

You may want to see also

Explore related products

![]()

Uninsured children statistics globally

Globally, an estimated 78 million children under the age of 18 lack health insurance, according to recent data from the World Health Organization (WHO) and UNICEF. This staggering figure represents a significant barrier to accessing essential healthcare services, including vaccinations, preventive care, and treatment for illnesses. The majority of these uninsured children reside in low- and middle-income countries, where healthcare systems are often underfunded and fragmented. For instance, in sub-Saharan Africa, nearly 40% of children are uninsured, compared to less than 5% in high-income countries like those in Western Europe. This disparity highlights the urgent need for targeted interventions to address the root causes of health inequity.

Analyzing the data further, the lack of insurance among children is closely tied to socioeconomic factors such as poverty, education, and geographic location. In rural areas, where infrastructure is limited and healthcare facilities are scarce, children are twice as likely to be uninsured compared to their urban counterparts. Additionally, children from households with lower educational attainment are disproportionately affected, as parents may lack awareness of available health programs or struggle to navigate complex enrollment processes. For example, in India, children from households where the primary caregiver has no formal education are 50% more likely to be uninsured than those with caregivers who have completed secondary education.

To address this crisis, policymakers and global health organizations must prioritize scalable solutions tailored to local contexts. One effective strategy is the expansion of community-based health insurance schemes, which have shown promise in countries like Rwanda and Ghana. These programs pool resources at the community level, making healthcare more affordable and accessible for families. Another critical step is integrating health insurance enrollment with existing social welfare programs, such as school feeding initiatives or cash transfer schemes. For instance, Mexico’s *Seguro Popular* program successfully reduced uninsured rates among children by linking insurance enrollment to poverty alleviation efforts.

A comparative analysis of successful models reveals that political will and sustainable funding are essential for long-term impact. Countries like Thailand and Sri Lanka have achieved near-universal health coverage for children through consistent government investment and public-private partnerships. In contrast, nations with fragmented healthcare systems and reliance on out-of-pocket payments, such as the United States, continue to struggle with high uninsured rates among children, particularly in marginalized communities. This underscores the importance of holistic policy approaches that address both supply-side (healthcare infrastructure) and demand-side (affordability and awareness) challenges.

Finally, raising awareness and empowering communities are vital components of any strategy to reduce uninsured rates among children. Public health campaigns can educate parents about the benefits of insurance and simplify enrollment processes through digital platforms or local health workers. For example, in Kenya, the use of mobile technology has streamlined insurance registration, increasing coverage among children by 25% in pilot districts. By combining innovative solutions with sustained commitment, the global community can make significant strides in ensuring that every child, regardless of where they are born, has access to the healthcare they need to thrive.

Step-by-Step Guide to Enrolling in Government Insurance Programs

You may want to see also

Explore related products

![]()

Impact of employment on insurance status

Employment status is a critical determinant of insurance coverage, with a direct correlation between job security and access to health benefits. According to the U.S. Census Bureau, approximately 8.6% of the population, or 28 million people, were uninsured in 2022. Among these, a disproportionate number are individuals who are unemployed, work part-time, or are employed in low-wage jobs that do not offer health insurance as a benefit. For instance, workers in the retail, hospitality, and gig economy sectors often face gaps in coverage due to the nature of their employment. Understanding this link is essential for addressing the uninsured rate, as employment policies and job market trends significantly influence insurance accessibility.

Consider the mechanics of employer-sponsored insurance (ESI), which covers about 56% of the U.S. population. Full-time workers are more likely to receive ESI, while part-time or temporary workers are frequently excluded. For example, a study by the Kaiser Family Foundation found that only 24% of part-time workers have access to employer-based insurance compared to 71% of full-time workers. This disparity highlights the need for policy interventions, such as expanding eligibility for public programs like Medicaid or subsidizing private insurance for low-income workers. Practical steps include advocating for portable benefits that move with workers across jobs and encouraging employers to extend coverage to part-time staff.

From a comparative perspective, countries with universal healthcare systems, such as Canada and the UK, demonstrate how decoupling insurance from employment can reduce uninsured rates. In contrast, the U.S. system relies heavily on ESI, leaving millions vulnerable during job transitions or periods of unemployment. For instance, during the 2020 pandemic, an estimated 14.6 million workers lost their employer-based insurance, underscoring the fragility of this model. A persuasive argument can be made for restructuring the system to ensure coverage continuity, such as through a public option or automatic enrollment in subsidized plans during unemployment.

Descriptively, the impact of employment on insurance status varies by age and industry. Younger workers aged 18–24, often in entry-level or part-time roles, have an uninsured rate of 13.9%, compared to 7.3% for those aged 25–34. Similarly, industries like construction and agriculture, which rely on seasonal or contract labor, report higher uninsured rates. To address this, targeted initiatives such as industry-specific insurance pools or state-level mandates for small businesses could be implemented. For individuals, practical tips include exploring Affordable Care Act (ACA) marketplace plans, which offer subsidies based on income, or utilizing COBRA to extend coverage temporarily after job loss.

In conclusion, the relationship between employment and insurance status is multifaceted, requiring both systemic changes and individual strategies. By analyzing trends, advocating for policy reforms, and adopting practical solutions, it is possible to mitigate the impact of employment instability on insurance coverage. This approach not only reduces the uninsured rate but also fosters a more equitable healthcare system.

Oregon Minimum Personal Injury Insurance: Does It Cover Death Benefits?

You may want to see also

Explore related products

![]()

Racial/ethnic gaps in coverage rates

Racial and ethnic disparities in health insurance coverage persist as a stark reminder of systemic inequalities. According to the U.S. Census Bureau, in 2022, 8.8% of Hispanics and 9.3% of American Indians/Alaska Natives were uninsured, compared to 5.4% of non-Hispanic Whites. These gaps highlight how socioeconomic factors, such as income and employment opportunities, intersect with race and ethnicity to determine access to healthcare. For instance, Hispanics are more likely to work in industries that do not offer employer-sponsored insurance, leaving them disproportionately reliant on public programs like Medicaid, which vary widely in eligibility across states.

To address these disparities, policymakers must consider targeted interventions. Expanding Medicaid in the 10 states that have not yet done so under the Affordable Care Act would immediately reduce uninsured rates among low-income populations, particularly in communities of color. Additionally, culturally tailored outreach programs can improve enrollment by addressing language barriers and mistrust of healthcare systems. For example, community health workers who speak Spanish or Indigenous languages can serve as liaisons, helping individuals navigate enrollment processes and understand their coverage options.

A comparative analysis reveals that racial gaps in coverage are not inevitable but are shaped by policy choices. In states like California, which invested heavily in outreach and simplified enrollment for diverse populations, uninsured rates among Hispanics dropped to 7.2% in 2022. Conversely, states with stricter Medicaid eligibility criteria, such as Texas, saw uninsured rates for Hispanics remain above 18%. This contrast underscores the impact of proactive measures in reducing disparities and suggests a roadmap for other states to follow.

Finally, the moral and economic imperatives for closing these gaps cannot be overstated. Uninsured individuals are more likely to delay care, leading to worse health outcomes and higher long-term costs for the healthcare system. By ensuring equitable access to insurance, we not only address a fundamental injustice but also create a healthier, more productive society. Practical steps include advocating for federal policies that standardize Medicaid expansion and supporting local initiatives that empower marginalized communities to demand better healthcare access.

Understanding Your Insurance: Am I the Cardholder?

You may want to see also

Frequently asked questions

As of recent data, approximately 8-10% of the U.S. population, or around 26-30 million people, do not have health insurance.

Globally, it’s estimated that over half of the world’s population, roughly 4 billion people, lack access to essential health services, including insurance.

Approximately 4 million children in the United States are uninsured, representing about 5% of all children.

Low-income individuals, young adults (ages 18-34), and people of color, particularly Hispanic and Native American populations, are disproportionately uninsured in the U.S.

According to the International Labour Organization (ILO), about 55% of the global population, or over 4 billion people, lack any form of social protection, including health insurance.