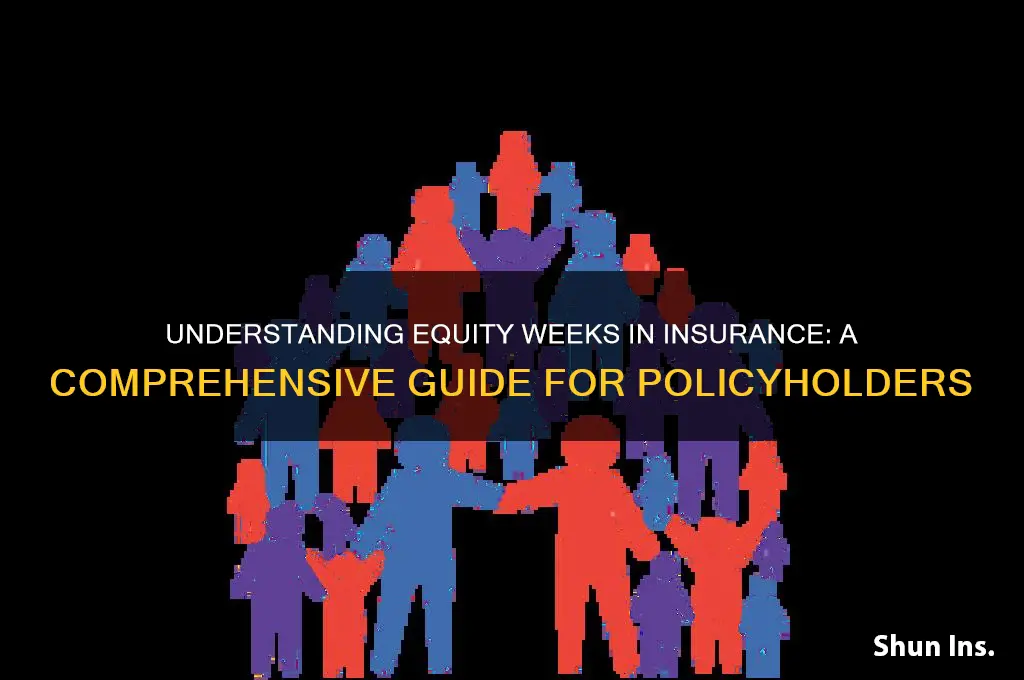

The concept of equity weeks for insurance refers to the number of weeks an individual or business must wait before their insurance policy begins to cover certain claims or benefits. This waiting period, often outlined in the policy terms, is designed to mitigate risks for insurers and ensure policyholders understand the timeline for coverage activation. The duration of equity weeks varies depending on the type of insurance, such as health, life, or property insurance, and can range from a few weeks to several months. Understanding this waiting period is crucial for policyholders to manage expectations and plan accordingly, ensuring they are not left vulnerable during the interim period.

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

What You'll Learn

- Equity Weeks Calculation Methods: Understanding different ways to compute equity weeks for insurance policies

- Impact on Premiums: How equity weeks affect insurance premium costs and coverage limits

- Policy Exclusions: Common exclusions related to equity weeks in insurance contracts

- Claims Process: Steps to file claims involving equity weeks in insurance policies

- Regulatory Guidelines: Legal and regulatory standards governing equity weeks in insurance

![]()

Equity Weeks Calculation Methods: Understanding different ways to compute equity weeks for insurance policies

Equity weeks in insurance policies represent the accumulated value of premiums paid into a policy, often used in whole life or endowment plans. Calculating these weeks is crucial for policyholders to understand their financial stake and potential benefits. Methods vary by insurer and policy type, but three primary approaches dominate: the premium accumulation method, the cash value growth method, and the policy duration adjustment method. Each offers distinct advantages and complexities, making it essential to choose the right one for accurate financial planning.

The premium accumulation method is the simplest and most straightforward. It calculates equity weeks by totaling the number of weeks for which premiums have been paid. For instance, if a policyholder pays weekly premiums for 208 weeks (4 years), their equity weeks would be 208. This method is ideal for policies with consistent premium payments and no additional contributions. However, it fails to account for interest or investment growth, making it less suitable for policies with cash value components.

In contrast, the cash value growth method factors in the policy’s cash value, which grows over time due to interest, dividends, or investment returns. Here, equity weeks are calculated by dividing the policy’s cash value by the weekly premium. For example, if a policy’s cash value is $10,000 and the weekly premium is $50, the equity weeks would be 200. This method provides a more dynamic view of equity but requires regular updates to reflect changes in cash value. It’s particularly useful for whole life policies where cash value is a key feature.

The policy duration adjustment method is more complex, as it considers the policy’s remaining term and the policyholder’s age. It calculates equity weeks by prorating the total expected premiums over the policy’s duration. For instance, a 20-year policy with 10 years remaining might allocate 50% of total premiums as equity weeks. This method is often used in endowment policies or those with fixed terms. While it provides a long-term perspective, it can be less precise for policies with variable premiums or irregular payments.

Choosing the right calculation method depends on the policy’s structure and the policyholder’s goals. For instance, a young policyholder with a whole life policy might prioritize the cash value growth method to track investment returns, while an older individual nearing policy maturity might prefer the policy duration adjustment method for clarity on remaining benefits. Regardless of the method, consulting with an insurance advisor ensures accurate calculations tailored to individual circumstances. Understanding these methods empowers policyholders to make informed decisions about their insurance investments.

Settlement Amounts and the Make Whole Doctrine: Ensuring Full Recovery

You may want to see also

Explore related products

![]()

Impact on Premiums: How equity weeks affect insurance premium costs and coverage limits

Equity weeks, a concept often tied to the number of weeks an individual or business has been consistently insured, play a pivotal role in shaping insurance premium costs and coverage limits. Insurers use this metric as a proxy for risk assessment, assuming that longer equity weeks correlate with lower risk due to demonstrated commitment and stability. For instance, a policyholder with 20 equity weeks might see premiums decrease by 5-10% compared to someone with only 5 equity weeks, as the insurer perceives them as a more reliable client. This dynamic underscores the importance of maintaining continuous coverage to optimize costs over time.

From an analytical perspective, the relationship between equity weeks and premiums is not linear but rather follows a diminishing returns model. Initially, each additional week of equity can yield significant premium reductions, particularly in the first 6-12 weeks. However, beyond this point, the rate of decrease slows, plateauing after 24-36 weeks. For example, a policyholder might save $50 in the first 12 weeks but only an additional $20 in the subsequent 12. Understanding this curve helps policyholders strategize when to reassess their policies for maximum savings.

Instructively, policyholders can leverage equity weeks to negotiate better terms with insurers. For instance, if you’ve maintained 30 equity weeks, you’re in a strong position to request a premium review or additional coverage without a proportional increase in cost. Practical tips include setting calendar reminders to track equity weeks and documenting any claims-free periods, as these further strengthen your case. Additionally, bundling policies or adding safety features (e.g., home security systems) can amplify the benefits of equity weeks, potentially reducing premiums by an additional 15-20%.

Comparatively, equity weeks function differently across insurance types. In auto insurance, 12-18 equity weeks often suffice to unlock lower premiums, while health or life insurance may require 24-36 weeks due to higher risk factors. For businesses, equity weeks in liability insurance can lead to coverage limit increases without additional cost, particularly after 48 weeks of continuous coverage. This disparity highlights the need for tailored strategies based on the specific insurance product and its associated risks.

Descriptively, the impact of equity weeks on coverage limits is particularly pronounced in high-risk sectors. For example, a construction company with 52 equity weeks might see its liability coverage limit increase from $1 million to $2 million without a premium hike, reflecting the insurer’s confidence in the company’s risk management practices. Conversely, a policyholder with only 8 equity weeks may face stricter limits or higher deductibles, even if their risk profile is otherwise favorable. This illustrates how equity weeks serve as a tangible measure of trust between insurers and policyholders, directly influencing both cost and coverage.

Does Apple Store Offer Insurance? Exploring Coverage Options for Your Devices

You may want to see also

Explore related products

![]()

Policy Exclusions: Common exclusions related to equity weeks in insurance contracts

Insurance contracts often include equity weeks as a feature, allowing policyholders to accumulate benefits over time. However, these provisions come with specific exclusions that can significantly impact coverage. One common exclusion is pre-existing conditions, which may render equity weeks void if the policyholder’s health issues were known before the policy’s inception. For instance, if a policyholder has a chronic illness like diabetes, any equity weeks tied to health-related benefits might be excluded from payout. This underscores the importance of thoroughly reviewing policy terms to understand limitations.

Another frequent exclusion relates to high-risk activities. Insurers often exclude equity weeks if the policyholder engages in activities deemed dangerous, such as skydiving or rock climbing. For example, a life insurance policy might nullify equity weeks if the policyholder dies while participating in an extreme sport. This exclusion is designed to mitigate risk for the insurer but can leave policyholders unprotected in certain scenarios. Always check the fine print to identify which activities are classified as high-risk.

Geographical restrictions also play a role in equity week exclusions. Some policies exclude benefits if the policyholder resides or travels to high-risk regions, such as war zones or areas prone to natural disasters. For instance, a travel insurance policy might exclude equity weeks if the policyholder visits a country under a travel advisory. Understanding these exclusions is crucial for those who frequently travel or relocate, as it directly affects the value of their coverage.

Lastly, non-compliance with policy terms can lead to the exclusion of equity weeks. This includes missed premium payments, failure to disclose material information, or violation of policy conditions. For example, if a policyholder fails to pay premiums on time, the insurer may reset the equity weeks counter, effectively erasing accumulated benefits. To avoid this, set up automatic payments and maintain open communication with your insurer to ensure compliance.

In summary, while equity weeks can enhance insurance benefits, they are often subject to exclusions that limit their applicability. Pre-existing conditions, high-risk activities, geographical restrictions, and non-compliance are common pitfalls. Policyholders must scrutinize their contracts, ask clarifying questions, and take proactive steps to ensure their equity weeks remain intact. This diligence ensures that the intended benefits of equity weeks are fully realized when needed.

Understanding Primary Insurance Determination: Key Factors and Processes Explained

You may want to see also

Explore related products

![]()

Claims Process: Steps to file claims involving equity weeks in insurance policies

Understanding the claims process for equity weeks in insurance policies requires clarity and precision. Equity weeks, often associated with timeshare or vacation ownership policies, represent a unique asset that can be insured against loss or damage. When filing a claim involving these weeks, policyholders must navigate a structured process to ensure their interests are protected. The first step is to review your policy documents to confirm coverage details, including the specific conditions under which equity weeks are insured. This initial scrutiny is crucial, as it sets the foundation for a successful claim.

Once you’ve verified coverage, the next step is to document the loss or damage comprehensively. For equity weeks, this might involve providing proof of ownership, details of the timeshare property, and evidence of the event that led to the claim (e.g., natural disaster, fraud, or contractual disputes). Photographs, contracts, and communication records with the timeshare management company can serve as valuable supporting materials. Insurers often require a detailed account of the incident, so organizing this information beforehand streamlines the process.

Filing the claim itself involves submitting a formal request to your insurance provider, typically through their designated claims portal or via a written statement. Be prepared to provide a clear, concise narrative of the situation, including dates, locations, and the extent of the loss. Some insurers may also require a police report or legal documentation if the claim involves theft or fraud. Timeliness is critical; most policies have a specific window within which claims must be filed to remain valid.

After submission, the insurer will review your claim and may request additional information or conduct an investigation. This stage can be lengthy, particularly for complex cases involving equity weeks, as insurers must verify the legitimacy of the claim and assess the value of the lost asset. Policyholders should maintain open communication with their insurer during this period, promptly responding to requests for further documentation or clarification. Patience and persistence are key, as delays can occur due to the unique nature of equity week claims.

Finally, once the claim is approved, the insurer will outline the settlement terms, which may include reimbursement for the financial value of the equity weeks or assistance in recovering the asset. Understanding the payout structure and any limitations in your policy is essential to managing expectations. For instance, some policies may cap coverage at a certain dollar amount or require policyholders to meet specific conditions before receiving full compensation. By following these steps and staying informed, policyholders can effectively navigate the claims process for equity weeks and secure the protection they deserve.

Liberty Mutual Grace Period: What Happens When Your Insurance Expires?

You may want to see also

Explore related products

![Life and Health Insurance License Exam Secrets Study Guide - Full-Length Practice Test, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71PdYCnP8ML._AC_UL320_.jpg)

![]()

Regulatory Guidelines: Legal and regulatory standards governing equity weeks in insurance

Equity weeks in insurance are not a universally standardized concept, but they often refer to the period during which policyholders can exercise their rights to equity benefits, such as dividends or bonuses, in participating insurance policies. Regulatory guidelines governing these periods vary significantly across jurisdictions, reflecting the diverse legal and financial landscapes of different regions. For instance, in the United Kingdom, the Financial Conduct Authority (FCA) mandates that insurers provide clear and transparent information about equity weeks, ensuring policyholders understand when and how they can access their equity benefits. This includes specifying the frequency and duration of these periods, typically ranging from one to four weeks annually, depending on the policy type and insurer’s discretion.

In contrast, the United States lacks a federal standard for equity weeks, leaving regulation to individual state insurance departments. States like New York and California have implemented stricter guidelines, requiring insurers to notify policyholders at least 30 days in advance of equity weeks and to provide detailed explanations of the benefits available. These notifications often include specific dates, eligibility criteria, and instructions for claiming equity. Insurers in these states must also adhere to fair treatment principles, ensuring that all policyholders have equal opportunities to exercise their rights during the designated periods.

A comparative analysis of regulatory frameworks reveals that jurisdictions with more stringent guidelines tend to foster greater consumer trust and participation in equity-based insurance products. For example, in Germany, the Federal Financial Supervisory Authority (BaFin) enforces a standardized equity week schedule across all insurers, typically aligning with the annual financial reporting cycle. This uniformity simplifies the process for policyholders and reduces administrative burdens for insurers. However, such standardization may limit flexibility, as insurers have less autonomy to tailor equity weeks to their specific business models or policy structures.

When implementing equity weeks, insurers must navigate not only legal requirements but also practical challenges. One key consideration is the timing of equity weeks relative to market conditions. For instance, scheduling equity weeks during periods of high market volatility could expose policyholders to greater risk, potentially undermining the stability of their benefits. To mitigate this, some regulators, like the European Insurance and Occupational Pensions Authority (EIOPA), recommend stress testing equity-based policies to ensure resilience under adverse market conditions. Insurers are also advised to provide educational resources to policyholders, helping them make informed decisions during equity weeks.

In conclusion, regulatory guidelines governing equity weeks in insurance are shaped by a balance between consumer protection and market efficiency. While standardization can enhance transparency and trust, it may also constrain innovation. Insurers must therefore stay informed about evolving regulations in their operating jurisdictions and adopt best practices to ensure compliance and customer satisfaction. By doing so, they can maximize the value of equity weeks for policyholders while maintaining the integrity of their products.

Uninsured Crash Impact: How It Affects Your Insurance Premiums

You may want to see also

Frequently asked questions

"Equity weeks for insurance" typically refers to the number of weeks an individual or business has paid into an insurance policy, often used in contexts like unemployment insurance or workers' compensation, where benefits are calculated based on prior contributions.

Equity weeks are usually calculated based on the number of weeks an individual has worked and paid into an insurance system, such as through payroll deductions or premiums, within a specific period (e.g., the past year or base period).

Yes, equity weeks often determine the duration or amount of insurance benefits you qualify for. For example, in unemployment insurance, more equity weeks may result in a longer benefit period or higher payout.

![Reply of the New York Life Insurance Company ... to an Interrogatory of the Minister of Finance of Russia Reading as Follows: "Ought the Present Operations of American 1893 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UL320_.jpg)

![Property and Casualty Insurance License Exam Study Guide - Property and Casualty Exam Secrets, Practice Test Questions, Detailed Answer Explanations [2nd Edition]](https://m.media-amazon.com/images/I/71fBYXIP4iL._AC_UL320_.jpg)