The Affordable Care Act (ACA), commonly known as Obamacare, aimed to reduce the number of uninsured Americans by expanding Medicaid, establishing health insurance marketplaces, and implementing individual mandates. While it significantly lowered uninsured rates, millions remain without coverage due to factors like eligibility gaps, affordability issues, and state-level decisions not to expand Medicaid. As of recent data, the number of non-insured individuals under Obamacare’s framework highlights ongoing challenges in achieving universal coverage, sparking debates about the effectiveness of the ACA and potential reforms needed to address remaining gaps.

Explore related products

What You'll Learn

- Impact on Uninsured Rates: Analyzes how Obamacare reduced uninsured numbers since implementation

- State-by-State Variations: Examines differences in uninsured rates across states post-Obamacare

- Demographic Changes: Explores shifts in uninsured rates by age, race, and income

- Medicaid Expansion Effects: Assesses how Medicaid expansion under Obamacare influenced uninsured numbers

- Remaining Uninsured Challenges: Identifies barriers preventing some individuals from gaining coverage despite Obamacare

![]()

Impact on Uninsured Rates: Analyzes how Obamacare reduced uninsured numbers since implementation

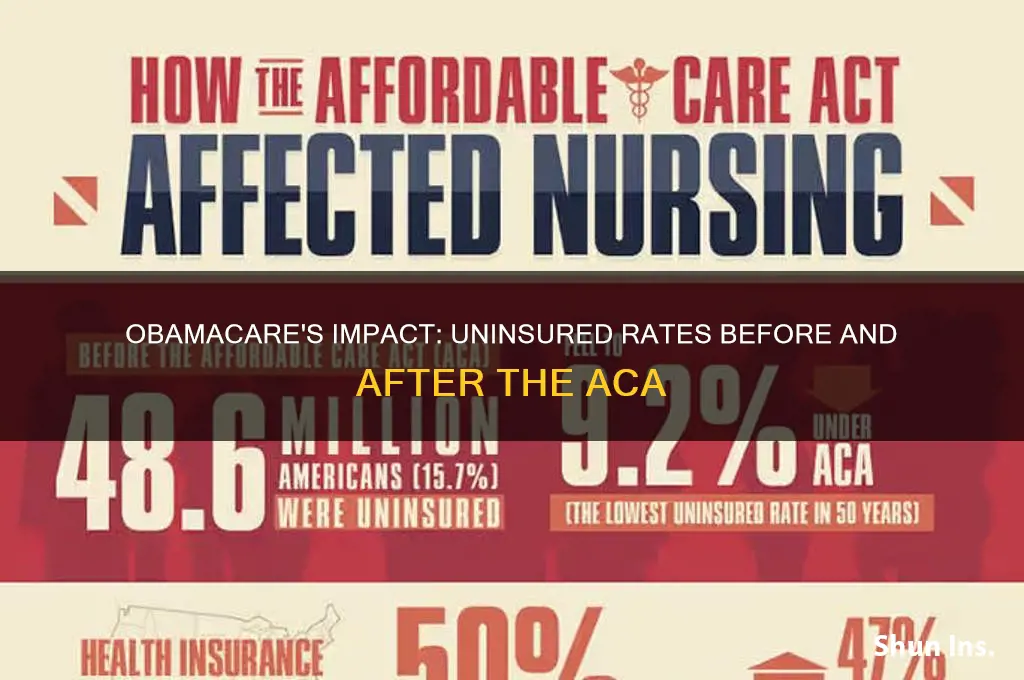

The Affordable Care Act (ACA), commonly known as Obamacare, has significantly reshaped the American healthcare landscape since its implementation in 2010. One of its most notable achievements is the substantial reduction in the number of uninsured individuals. Before the ACA, approximately 46.5 million non-elderly Americans lacked health insurance in 2010. By 2020, this number had dropped to around 29 million, marking a historic decline in uninsured rates. This reduction is a direct result of key provisions such as Medicaid expansion, the establishment of health insurance marketplaces, and the mandate for individuals to have coverage.

To understand how Obamacare achieved this, consider the mechanism of Medicaid expansion. States that expanded Medicaid eligibility saw a dramatic decrease in uninsured rates among low-income adults. For example, in Kentucky, the uninsured rate fell from 14.3% in 2013 to 5.8% in 2019 after expanding Medicaid. This expansion allowed individuals earning up to 138% of the federal poverty level to qualify for coverage, a critical step in bridging the insurance gap. Conversely, states that did not expand Medicaid experienced slower declines, highlighting the policy’s direct impact.

Another pivotal factor is the creation of health insurance marketplaces, which offer subsidized plans to individuals and families. These subsidies, based on income, make coverage more affordable for millions. For instance, a family of four earning up to $104,800 in 2023 could qualify for premium tax credits, significantly reducing their monthly premiums. This financial assistance has been instrumental in encouraging enrollment, particularly among middle-income households who previously found insurance costs prohibitive.

However, the individual mandate, which required most Americans to have health insurance or pay a penalty, played a less direct but still important role. While the penalty was eliminated in 2019, the mandate initially incentivized millions to enroll in coverage. Its impact is evident in the initial years of ACA implementation, where uninsured rates dropped sharply. Despite its removal, the cultural shift toward viewing health insurance as a necessity has persisted, contributing to sustained enrollment numbers.

Despite these successes, challenges remain. Disparities in uninsured rates persist across demographics, with younger adults, racial minorities, and low-income individuals still more likely to lack coverage. Additionally, the ACA’s impact varies by state, with non-expansion states experiencing higher uninsured rates. Addressing these gaps requires targeted policies, such as further incentivizing Medicaid expansion and increasing outreach to underserved communities.

In conclusion, Obamacare’s impact on reducing uninsured rates is undeniable. Through Medicaid expansion, marketplace subsidies, and the individual mandate, millions have gained access to affordable coverage. While challenges remain, the ACA has set a foundation for continued progress in achieving universal healthcare access. Practical steps, such as advocating for Medicaid expansion in non-expansion states and simplifying enrollment processes, can further build on this success.

High Blood Pressure: Getting Term Life Insurance

You may want to see also

Explore related products

![]()

State-by-State Variations: Examines differences in uninsured rates across states post-Obamacare

The Affordable Care Act (ACA), colloquially known as Obamacare, has significantly reshaped the American healthcare landscape, yet its impact on uninsured rates varies dramatically across states. While the national uninsured rate dropped from 16% in 2010 to 8.6% in 2021, this aggregate statistic masks stark disparities. States that expanded Medicaid under the ACA, such as California and New York, saw uninsured rates plummet to below 7%. In contrast, non-expansion states like Texas and Florida continue to struggle, with rates hovering around 15% or higher. This divergence underscores the critical role of state-level policy decisions in determining access to healthcare.

To understand these variations, consider the mechanics of Medicaid expansion. States that opted in received federal funding to cover individuals earning up to 138% of the federal poverty level (FPL), approximately $18,754 for an individual in 2023. This policy disproportionately benefited Southern and Midwestern states, where poverty rates are higher. However, 10 states, primarily in the South, have yet to expand Medicaid, leaving millions of low-income adults in the "coverage gap"—earning too much for traditional Medicaid but too little for ACA subsidies. For instance, in Texas, over 1 million residents fall into this gap, contributing to its 18% uninsured rate, the highest in the nation.

Another factor driving state-by-state differences is the political climate and its influence on healthcare policy. In states with Democratic-controlled legislatures, there’s been a stronger push for ACA implementation, including robust marketing campaigns and simplified enrollment processes. Conversely, Republican-led states often face resistance to ACA-related initiatives, resulting in lower enrollment rates. For example, Kentucky, initially a success story under Democratic leadership, saw its uninsured rate rise after policy shifts reduced outreach efforts. This highlights how political volatility can undermine long-term gains in healthcare access.

Practical solutions exist to mitigate these disparities. States can leverage Section 1115 waivers to design innovative Medicaid programs tailored to their populations. Arkansas and Indiana, for instance, used waivers to introduce work requirements and health savings accounts, though these policies faced legal challenges. Additionally, states can invest in local navigators and community health workers to assist residents with enrollment, particularly in rural or underserved areas. For individuals in non-expansion states, understanding eligibility for cost-sharing reductions or catastrophic plans can provide a temporary safety net, though these options are not as comprehensive as Medicaid.

Ultimately, the state-by-state variations in uninsured rates post-Obamacare reveal both the strengths and limitations of a decentralized healthcare system. While the ACA provided a framework for expanding coverage, its success hinges on state cooperation and innovation. Policymakers, advocates, and residents must collaborate to address these gaps, ensuring that geography does not dictate access to healthcare. Until then, the map of uninsured rates will remain a patchwork of progress and persistence.

Does Germany Offer Separate Eye Insurance? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Demographic Changes: Explores shifts in uninsured rates by age, race, and income

The Affordable Care Act (ACA), often referred to as Obamacare, has significantly reshaped the landscape of health insurance coverage in the United States. One of the most striking changes has been the reduction in uninsured rates across various demographic groups. However, these reductions have not been uniform, revealing important shifts by age, race, and income. Understanding these changes is crucial for policymakers, healthcare providers, and individuals navigating the system.

Consider the age-based disparities in uninsured rates. Before the ACA, young adults aged 18–24 were among the most likely to be uninsured due to factors like part-time employment and lack of employer-sponsored insurance. Post-ACA, this group saw a dramatic drop in uninsured rates, thanks to provisions allowing them to stay on their parents’ plans until age 26. For example, the uninsured rate among 19- to 25-year-olds fell from 34% in 2010 to 12% in 2020. In contrast, older adults, particularly those nearing Medicare eligibility (ages 55–64), still face higher uninsured rates due to gaps in affordability and access to employer-based coverage. This highlights the need for targeted solutions, such as expanding subsidies for this age group.

Racial and ethnic disparities in uninsured rates have also shifted under the ACA, though gaps persist. Hispanic and Black Americans historically faced higher uninsured rates due to systemic barriers like lower incomes and limited access to employer-sponsored insurance. The ACA’s Medicaid expansion reduced these disparities significantly, with uninsured rates among Hispanic adults dropping from 32% in 2013 to 19% in 2020. However, these groups still lag behind non-Hispanic whites, whose uninsured rate fell to 7% in the same period. Addressing these gaps requires addressing root causes, such as expanding Medicaid in holdout states and improving cultural competency in healthcare delivery.

Income remains a critical determinant of insurance status, with low-income individuals benefiting the most from the ACA’s provisions. For households earning below 200% of the federal poverty level (FPL), uninsured rates dropped by nearly half post-ACA, largely due to Medicaid expansion. However, those in the “coverage gap”—residing in non-expansion states with incomes too high for Medicaid but too low for marketplace subsidies—continue to struggle. For instance, in states like Texas and Florida, over 1 million people fall into this gap. Practical steps to address this include advocating for state-level Medicaid expansion and exploring alternative coverage options like community health centers.

In conclusion, the ACA has driven significant reductions in uninsured rates, but demographic shifts reveal persistent challenges. By focusing on age-specific policies, addressing racial disparities, and closing income-based gaps, stakeholders can build on the ACA’s progress. For individuals, staying informed about eligibility criteria and available resources is key. For policymakers, targeted interventions are essential to ensure equitable access to care across all demographics.

Ordinary Life Insurance: Understanding Accumulated Value Benefits

You may want to see also

Explore related products

![]()

Medicaid Expansion Effects: Assesses how Medicaid expansion under Obamacare influenced uninsured numbers

The Affordable Care Act (ACA), commonly known as Obamacare, introduced a significant policy lever to reduce the uninsured rate: Medicaid expansion. By allowing states to extend Medicaid eligibility to adults earning up to 138% of the federal poverty level (FPL), the ACA aimed to close coverage gaps for low-income populations. As of 2023, 40 states and the District of Columbia have adopted this expansion, while 10 states remain holdouts. This divide provides a natural experiment to assess the direct impact of Medicaid expansion on uninsured numbers. States that expanded Medicaid saw an average reduction in their uninsured rate of 9.3 percentage points between 2013 and 2021, compared to a 4.7-point drop in non-expansion states, according to the Kaiser Family Foundation. This disparity underscores the policy’s effectiveness in reaching its target population.

Consider the case of Kentucky, a state that expanded Medicaid in 2014. Within two years, its uninsured rate plummeted from 14.3% to 5.8%, as reported by the Commonwealth Fund. This dramatic shift was not merely statistical; it translated into tangible health improvements. Emergency department visits for preventable conditions decreased by 11%, and self-reported health status improved among low-income adults. Conversely, in Texas, which has not expanded Medicaid, the uninsured rate remains stubbornly high at 18%, the highest in the nation. This comparison highlights the critical role of state-level policy decisions in shaping health coverage outcomes.

However, the effects of Medicaid expansion extend beyond raw numbers. Expanded coverage has alleviated financial strain on individuals and families. A 2020 study in *Health Affairs* found that Medicaid expansion reduced the likelihood of individuals reporting difficulty paying medical bills by 20%. For households earning between 100% and 138% of the FPL, this protection is particularly vital, as they often fall into the "coverage gap" in non-expansion states—earning too much for traditional Medicaid but too little to afford private insurance. Expansion effectively bridges this gap, offering a safety net to millions.

Critics argue that Medicaid expansion strains state budgets, but evidence suggests otherwise. Federal funding covers 90% of expansion costs, and states like Michigan have reported net savings due to reduced uncompensated care costs. Moreover, the economic benefits of expansion are substantial. A 2019 study by the Georgetown University Center for Children and Families estimated that expansion states gained $84 billion in federal funding in 2019 alone, supporting jobs and local economies. This economic infusion underscores the policy’s dual role in improving health and bolstering financial stability.

For policymakers and advocates, the lesson is clear: Medicaid expansion is a powerful tool to reduce uninsured rates and improve health outcomes. States that have not yet expanded Medicaid should reconsider their stance, weighing the proven benefits against ideological opposition. For individuals, understanding the eligibility criteria—typically up to $18,754 for a single adult in 2023—can be the first step toward accessing affordable coverage. As the debate over healthcare continues, the evidence from Medicaid expansion states provides a compelling case for its expansion nationwide.

Securing Peace of Mind: Insuring Older Parents with Care and Confidence

You may want to see also

Explore related products

![]()

Remaining Uninsured Challenges: Identifies barriers preventing some individuals from gaining coverage despite Obamacare

Despite the Affordable Care Act's (ACA) significant strides in expanding healthcare coverage, millions of Americans remain uninsured. A 2022 Census Bureau report reveals that approximately 8.3% of the population, or around 27 million people, lacked health insurance in 2021. While this represents a substantial decrease from pre-ACA levels, it highlights persistent challenges in achieving universal coverage.

Financial Barriers Persist:

For many, the cost of health insurance remains a formidable obstacle. Even with subsidies available through the ACA marketplaces, premiums, deductibles, and out-of-pocket costs can be prohibitively expensive for low-income individuals and families. A 2021 Commonwealth Fund survey found that 43% of uninsured adults cited cost as the primary reason for lacking coverage. This is particularly acute for those who fall into the "coverage gap" – earning too much to qualify for Medicaid in their state but too little to afford marketplace plans.

Expanding Medicaid in all states would significantly reduce this gap, providing coverage to an estimated 2.2 million uninsured individuals.

Navigating Complexity:

The ACA's complexity can be a barrier in itself. Understanding eligibility requirements, plan options, and enrollment processes can be daunting, especially for those with limited health literacy or language barriers. A 2019 study published in *Health Affairs* found that individuals with lower health literacy were less likely to enroll in ACA plans, even when eligible for subsidies.

Simplifying enrollment processes, providing multilingual resources, and offering personalized assistance through navigators and community health workers could improve access for these populations.

Immigration Status and Fear:

Undocumented immigrants are ineligible for ACA marketplace plans and Medicaid, leaving them particularly vulnerable to being uninsured. Fear of immigration enforcement can also deter eligible family members from enrolling, even if they are citizens or legal residents. Addressing these fears and exploring alternative coverage options for undocumented individuals, such as state-funded programs or community health centers, is crucial for achieving more equitable coverage.

The Role of Policy and Politics:

Political opposition to the ACA has led to ongoing efforts to undermine the law, creating uncertainty and potentially discouraging enrollment. Expanding Medicaid in holdout states, strengthening outreach and education efforts, and protecting the ACA from further erosion are essential steps towards reducing the number of uninsured Americans.

Understanding Aleatory Contracts: Key Concepts in Insurance Policies Explained

You may want to see also

Frequently asked questions

Before the Affordable Care Act (ACA) was fully implemented in 2014, approximately 44 million non-elderly Americans were uninsured in 2013, according to the U.S. Census Bureau.

As of 2022, the number of uninsured non-elderly Americans has decreased significantly, with estimates ranging between 25 to 30 million, depending on the source.

Yes, Obamacare has substantially reduced the uninsured rate. Since its implementation, the uninsured rate has dropped from approximately 18% in 2013 to around 9-10% in recent years.

Some individuals remain uninsured due to factors like affordability issues, gaps in Medicaid expansion (in states that did not expand Medicaid), undocumented immigrants being ineligible for coverage, and personal choices to opt out of insurance.