The number of people enrolled in federal health insurance programs in the United States is a critical indicator of the nation's healthcare landscape. As of recent data, millions of Americans rely on federal programs such as Medicare, Medicaid, and the Children’s Health Insurance Program (CHIP) for their health coverage. Medicare primarily serves individuals aged 65 and older, as well as certain younger people with disabilities, while Medicaid and CHIP provide coverage for low-income families, children, and pregnant women. Additionally, the Affordable Care Act (ACA) expanded Medicaid eligibility in many states, further increasing enrollment. Understanding the scale of federal health insurance participation is essential for assessing the impact of these programs on public health, healthcare costs, and policy decisions.

Explore related products

What You'll Learn

![]()

Medicaid enrollment numbers

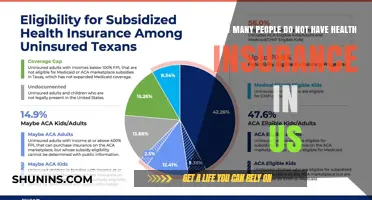

As of recent data, Medicaid, a joint federal and state program, covers over 80 million Americans, making it the largest source of health insurance in the United States. This figure represents a significant portion of the population, particularly those with low income, disabilities, or specific medical needs. Understanding Medicaid enrollment numbers is crucial, as it highlights the program’s role in addressing healthcare disparities and its impact on public health.

Analyzing enrollment trends reveals that Medicaid expansion under the Affordable Care Act (ACA) has been a driving force behind increased coverage. States that expanded Medicaid saw enrollment rise by an average of 25% compared to non-expansion states. For example, in California, over 14 million residents are enrolled in Medi-Cal (the state’s Medicaid program), accounting for nearly 35% of the state’s population. This expansion has been particularly beneficial for adults aged 19–64, who previously fell into the "coverage gap" without access to affordable insurance.

However, enrollment numbers are not static; they fluctuate due to policy changes, economic conditions, and administrative barriers. During the COVID-19 pandemic, Medicaid enrollment surged by over 20 million people nationwide, as the federal government prohibited states from disenrolling individuals during the public health emergency. As this protection ends, states are now unwinding their Medicaid rolls, with an estimated 15 million people at risk of losing coverage. This underscores the need for clear communication and streamlined processes to ensure eligible individuals remain insured.

To navigate Medicaid enrollment effectively, individuals should be aware of key eligibility criteria, which vary by state but generally include income limits (often 138% of the federal poverty level for adults in expansion states) and categorical requirements (e.g., pregnant women, children, or disabled individuals). Practical tips include using state-specific online portals for applications, keeping documentation organized, and seeking assistance from local enrollment navigators. For families, children under 19 are often eligible for coverage through the Children’s Health Insurance Program (CHIP), even if parents do not qualify for Medicaid.

In conclusion, Medicaid enrollment numbers reflect both the program’s success in expanding access to healthcare and the challenges it faces in maintaining coverage. By staying informed about eligibility rules, policy changes, and available resources, individuals and families can maximize their chances of securing this vital federal health insurance.

Get Insurance for Your Newborn with These Medicaid Tips

You may want to see also

Explore related products

![]()

Medicare beneficiary statistics

As of 2023, Medicare covers over 65 million Americans, primarily those aged 65 and older, alongside younger individuals with certain disabilities or conditions. This figure represents nearly 20% of the U.S. population, making Medicare one of the largest federal health insurance programs. Understanding the demographics and trends within Medicare beneficiary statistics is crucial for policymakers, healthcare providers, and beneficiaries themselves. For instance, while the majority of beneficiaries are seniors, approximately 15% are under 65, qualifying due to disabilities or conditions like End-Stage Renal Disease (ESRD). This highlights the program’s dual role in serving both the elderly and a significant portion of the disabled population.

Analyzing enrollment trends reveals a steady increase in Medicare beneficiaries, driven by the aging Baby Boomer population. Between 2000 and 2020, the number of beneficiaries grew by over 40%, and projections indicate this trend will continue, with an estimated 80 million enrollees by 2030. This growth has significant implications for federal spending, as Medicare accounted for 12% of the federal budget in 2022. However, it’s not just the size of the program that matters; the diversity of beneficiaries does too. For example, racial and ethnic minorities represent a growing share of enrollees, with Hispanic and Black beneficiaries expected to increase by 105% and 64%, respectively, by 2030. Tailoring healthcare services to meet the unique needs of these groups is essential for improving health outcomes.

One critical aspect of Medicare beneficiary statistics is the distribution of enrollees across different parts of the program. Approximately 57% of beneficiaries are enrolled in traditional Medicare (Part A and Part B), while 43% opt for Medicare Advantage plans. Medicare Advantage, offered by private insurers, has seen rapid growth due to its additional benefits, such as vision and dental coverage. However, beneficiaries must carefully evaluate these plans, as they often come with provider network restrictions and varying out-of-pocket costs. For instance, while Medicare Advantage may offer lower premiums, traditional Medicare provides more flexibility in choosing healthcare providers.

Geographic disparities also play a significant role in Medicare beneficiary statistics. Rural areas face unique challenges, including limited access to healthcare providers and higher rates of chronic conditions among beneficiaries. In contrast, urban areas often have greater access to specialists and healthcare facilities but may experience higher costs. For example, beneficiaries in rural counties are 20% more likely to have diabetes than their urban counterparts, underscoring the need for targeted interventions in these regions. Policymakers can address these disparities by expanding telehealth services and incentivizing providers to practice in underserved areas.

Finally, understanding Medicare beneficiary statistics requires examining the financial burden on enrollees. While Medicare covers a significant portion of healthcare costs, beneficiaries still face substantial out-of-pocket expenses, particularly for prescription drugs and long-term care. In 2022, the average Medicare beneficiary spent $6,000 annually on healthcare, with those in poor health spending significantly more. To mitigate these costs, beneficiaries should explore supplemental coverage options, such as Medigap policies or employer-sponsored retiree plans. Additionally, enrolling in Medicare Part D for prescription drug coverage can provide substantial savings, especially for those with chronic conditions requiring expensive medications. By leveraging these tools, beneficiaries can better navigate the complexities of Medicare and reduce their financial strain.

Online Medical Insurance: Check Your Personal Policy Easily

You may want to see also

Explore related products

![]()

Children’s Health Insurance Program (CHIP) coverage

As of recent data, approximately 12 million children in the United States are enrolled in the Children’s Health Insurance Program (CHIP), a federal-state partnership designed to provide low-cost health coverage to children in families who earn too much to qualify for Medicaid but cannot afford private insurance. This program, established in 1997, has been a cornerstone of pediatric healthcare access, ensuring that eligible children up to age 19 receive comprehensive benefits, including doctor visits, immunizations, dental care, and emergency services. CHIP’s success lies in its ability to bridge the gap between Medicaid and private insurance, offering a safety net for millions of families.

CHIP’s eligibility criteria vary by state, but generally, families with incomes up to 200% of the federal poverty level (FPL) qualify, though some states extend coverage to higher income thresholds. For example, in 2023, a family of four earning up to $55,500 annually could be eligible in many states. Notably, CHIP covers pregnant women in some states, ensuring prenatal care for expectant mothers. The program’s affordability is a key feature: families pay minimal premiums, copays, or enrollment fees, with costs capped to ensure accessibility. This structure has been instrumental in reducing the uninsured rate among children to historic lows.

One of CHIP’s standout features is its comprehensive benefit package, tailored to meet the unique needs of children. Services include well-child visits, vision and dental care, mental health services, and prescriptions. For instance, CHIP covers vaccinations according to the CDC’s recommended schedule, ensuring children are protected against preventable diseases. Additionally, the program emphasizes preventive care, such as regular check-ups and developmental screenings, which are critical for early detection of health issues. This focus on prevention not only improves health outcomes but also reduces long-term healthcare costs.

Despite its successes, CHIP faces challenges, including funding stability and enrollment barriers. The program is periodically reauthorized by Congress, creating uncertainty for states and families. Advocacy efforts have been crucial in securing long-term funding, such as the 10-year extension passed in 2018. Enrollment barriers, such as complex application processes or lack of awareness, persist in some communities. States have implemented strategies like streamlined online applications and outreach campaigns to address these issues. For families, practical tips include checking eligibility annually, as income thresholds may change, and utilizing state-specific resources to navigate the enrollment process.

In comparison to other federal health insurance programs, CHIP stands out for its targeted focus on children and its flexibility in state implementation. While Medicaid serves a broader population, including low-income adults and children, CHIP specifically addresses the needs of families who fall into the coverage gap. Unlike private insurance, CHIP ensures that cost is not a barrier to care, making it a vital component of the federal health insurance landscape. Its impact is evident in the millions of children who have accessed care through the program, underscoring its role in promoting healthier futures for America’s youth.

Accident Insurance: Protecting Your Family's Future

You may want to see also

Explore related products

![]()

Federal Employee Health Benefits (FEHB) data

Analyzing FEHB enrollment trends over the past decade shows steady growth, driven by both an aging federal workforce and increased family member participation. For instance, retiree enrollment has risen by 12% since 2013, reflecting the demographic shift within the federal sector. Notably, FEHB offers over 200 health plan options across the country, including Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and High-Deductible Health Plans (HDHPs). This diversity allows enrollees to select plans based on their health needs, geographic location, and financial preferences, a flexibility not always available in private-sector insurance.

From a practical standpoint, FEHB’s cost structure is a key differentiator. The federal government contributes an average of 72% of the premium cost, significantly reducing out-of-pocket expenses for enrollees. For example, in 2023, the average annual premium for self-only coverage was $7,200, with the employee paying approximately $2,000. This generous subsidy makes FEHB one of the most affordable health insurance options in the U.S., particularly for families. However, beneficiaries should be aware of open season periods (typically November to December) to review and adjust their plans, as changes in healthcare needs or family status may warrant a switch.

Comparatively, FEHB stands out when juxtaposed with private-sector health insurance. While private plans often limit provider networks or impose higher deductibles, FEHB plans generally offer broader access to specialists and lower out-of-pocket maximums. For instance, the average deductible for an FEHB PPO plan is $500, compared to $1,500 for a similar private-sector plan. This advantage is particularly beneficial for individuals with chronic conditions or those requiring specialized care. However, FEHB’s complexity—with its myriad plan options and enrollment rules—can be daunting for new federal employees, emphasizing the need for clear, accessible guidance during onboarding.

In conclusion, FEHB data not only highlights the program’s scale but also its unique features and benefits. With millions relying on it for healthcare coverage, FEHB serves as a benchmark for employer-sponsored insurance, offering affordability, flexibility, and comprehensive care. For federal employees and their families, maximizing FEHB’s potential requires proactive plan management and an understanding of its nuances. As the program continues to evolve, staying informed about enrollment trends, cost structures, and plan options will remain essential for optimizing this valuable benefit.

Canada's Medical Insurance: What's Covered and How It Works

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61ilSrOeMoL._AC_UY218_.jpg)

![]()

Affordable Care Act (ACA) marketplace enrollment figures

The Affordable Care Act (ACA) marketplace has been a cornerstone of federal health insurance, providing coverage to millions of Americans since its inception. As of the most recent enrollment period, approximately 14.5 million people signed up for health insurance through the ACA marketplace, marking a steady increase from previous years. This figure underscores the continued reliance on the ACA as a vital source of coverage, particularly for individuals and families who do not have access to employer-sponsored insurance or other public programs like Medicaid.

Analyzing the enrollment trends reveals a nuanced picture. For instance, states that expanded Medicaid under the ACA have seen lower marketplace enrollment, as more residents qualify for Medicaid coverage. Conversely, non-expansion states have higher marketplace enrollment, as individuals with incomes above Medicaid eligibility thresholds turn to the ACA for affordable options. Additionally, subsidies provided through the ACA, such as Advanced Premium Tax Credits (APTCs), have been instrumental in driving enrollment. These subsidies, which reduce monthly premiums for eligible enrollees, have made coverage more accessible, particularly for low- and middle-income households.

From a practical standpoint, understanding ACA marketplace enrollment figures is crucial for policymakers, insurers, and consumers alike. For individuals, knowing the enrollment trends can help in making informed decisions during open enrollment periods. For example, enrollees should be aware of income thresholds for subsidies, which are based on the federal poverty level (FPL). In 2023, a family of four earning up to $106,000 annually could qualify for APTCs, significantly lowering their premium costs. It’s also important to note that special enrollment periods (SEPs) are available for those experiencing qualifying life events, such as job loss or marriage, allowing them to enroll outside the standard open enrollment window.

Comparatively, the ACA marketplace stands out when juxtaposed with other federal health insurance programs. While Medicare serves primarily older adults and certain disabled individuals, and Medicaid targets low-income populations, the ACA marketplace fills a critical gap for those who fall outside these categories. Its enrollment figures highlight its role as a safety net for the underinsured and uninsured, particularly in states with limited Medicaid expansion. However, challenges remain, including premium affordability for those just above subsidy eligibility and the complexity of plan choices, which can deter potential enrollees.

In conclusion, ACA marketplace enrollment figures are more than just numbers—they reflect the program’s impact on access to healthcare. With millions relying on this federal health insurance option, efforts to stabilize and improve the marketplace are essential. Policymakers must address affordability concerns, simplify enrollment processes, and expand outreach to ensure that eligible individuals are aware of their options. For consumers, staying informed about enrollment periods, subsidy eligibility, and available plans can maximize the benefits of this critical program. As the healthcare landscape evolves, the ACA marketplace remains a key pillar in the federal health insurance framework.

Health Insurance Companies and Racial Bias: Uncovering Systemic Inequities

You may want to see also

Frequently asked questions

As of recent data, approximately 150 million people are enrolled in federal health insurance programs, including Medicare, Medicaid, and the Children’s Health Insurance Program (CHIP).

About 45% of the U.S. population is covered by federal health insurance programs, primarily through Medicare, Medicaid, and CHIP.

Medicaid is the largest federal health insurance program, covering over 80 million individuals, followed by Medicare with about 65 million enrollees.

Medicare covers approximately 65 million Americans, primarily seniors aged 65 and older, as well as some younger individuals with disabilities.