In the United States, the percentage of people with health insurance has been a critical indicator of the nation's healthcare access and overall well-being. As of recent data, approximately 91% of the U.S. population is covered by some form of health insurance, reflecting significant progress since the implementation of the Affordable Care Act (ACA) in 2010. This coverage is primarily divided among employer-sponsored plans, Medicaid, Medicare, and individual market plans. Despite this high coverage rate, disparities persist, with uninsured rates varying by factors such as income, race, ethnicity, and geographic location. Understanding these statistics is essential for policymakers, healthcare providers, and advocates working to address gaps in coverage and improve health equity across the country.

Explore related products

What You'll Learn

![]()

Employer-based coverage trends

Employer-based health insurance remains the cornerstone of coverage for millions of Americans, but its landscape is shifting. As of 2023, approximately 54% of the U.S. population relies on employer-sponsored plans, a figure that has held relatively steady over the past decade. However, beneath this stability lies a complex interplay of trends reshaping how employers and employees approach health benefits.

One notable trend is the rise of high-deductible health plans (HDHPs), which now account for over 50% of employer-offered coverage. Paired with Health Savings Accounts (HSAs), these plans incentivize cost-consciousness but often leave employees vulnerable to out-of-pocket expenses. For instance, the average deductible for a single-coverage HDHP in 2023 is $2,200, a 5% increase from the previous year. Employers are increasingly adopting these plans to manage costs, but employees, particularly those in lower-wage jobs, face financial strain when accessing care.

Another shift is the growing emphasis on wellness and preventive care programs. Over 80% of large employers now offer wellness initiatives, ranging from gym reimbursements to mental health apps. While these programs aim to improve employee health and reduce long-term costs, their effectiveness varies. Studies show that participation rates are often low, and benefits are unevenly distributed, with younger, healthier employees more likely to engage. Employers must refine these programs to ensure inclusivity and measurable outcomes.

The gig economy’s expansion has also impacted employer-based coverage. With an estimated 10.3 million independent contractors in the U.S., traditional employer-sponsored insurance excludes a growing segment of the workforce. Some companies are experimenting with portable benefits models, allowing gig workers to carry health coverage across jobs. However, these solutions remain fragmented and insufficient to address the broader gap in access.

Finally, the COVID-19 pandemic accelerated the adoption of telehealth services, now integrated into 96% of employer-sponsored plans. This shift has improved access to care, particularly for remote or rural employees. However, concerns persist about over-reliance on virtual care for conditions requiring in-person treatment. Employers must strike a balance between convenience and comprehensive care delivery.

In navigating these trends, employers face a dual challenge: controlling costs while ensuring meaningful coverage for a diverse workforce. Employees, meanwhile, must become savvy consumers, understanding plan details and advocating for their health needs. As the employer-based system evolves, its success will hinge on adaptability, equity, and a commitment to holistic well-being.

Obtaining Your Medical Insurance Number: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Medicare and Medicaid enrollment

As of recent data, approximately 91% of Americans have health insurance, a figure that reflects the combined efforts of private insurance, employer-sponsored plans, and government programs like Medicare and Medicaid. Among these, Medicare and Medicaid play a pivotal role, covering millions of individuals across different age groups and socioeconomic statuses. Understanding their enrollment dynamics is crucial for grasping the broader landscape of health insurance coverage in the U.S.

Analytical Perspective:

Medicare, primarily serving individuals aged 65 and older, along with certain younger people with disabilities, covers over 65 million Americans. Its enrollment has steadily increased due to the aging population, with projections indicating further growth as Baby Boomers reach eligibility age. Medicaid, on the other hand, serves as a safety net for low-income individuals, families, pregnant women, and children, covering approximately 84 million people. Its enrollment surged following the Affordable Care Act’s expansion, which allowed states to extend eligibility to more adults. Together, these programs account for nearly 45% of the insured population, highlighting their central role in the U.S. healthcare system.

Instructive Approach:

To enroll in Medicare, individuals typically become eligible at age 65, though those with specific disabilities or conditions like End-Stage Renal Disease can qualify earlier. The initial enrollment period begins three months before the month of your 65th birthday and ends three months after. Missing this window can result in penalties, so timely application is critical. For Medicaid, eligibility varies by state, but generally includes individuals with incomes up to 138% of the federal poverty level in expansion states. Applications can be submitted year-round through state agencies or the Health Insurance Marketplace, with coverage often beginning immediately upon approval.

Comparative Insight:

While Medicare is federally standardized, Medicaid’s variability across states creates disparities in coverage and access. For instance, states that expanded Medicaid under the ACA have significantly lower uninsured rates compared to non-expansion states. Additionally, Medicare’s structured benefit packages contrast with Medicaid’s flexible state-determined benefits, which can include services like dental and vision care not covered by Medicare. These differences underscore the importance of understanding each program’s nuances when assessing overall health insurance coverage.

Persuasive Argument:

Expanding Medicaid in the remaining non-expansion states could reduce the uninsured rate by an estimated 40%, providing coverage to millions of low-income adults currently in the "coverage gap." Similarly, addressing Medicare’s gaps, such as limited dental and vision benefits, could improve health outcomes for seniors. Policymakers must prioritize strengthening these programs to ensure equitable access to care. By doing so, the U.S. can move closer to universal coverage, reducing the financial and health burdens on vulnerable populations.

Practical Tips:

For those nearing Medicare eligibility, consider enrolling in Part B during the initial period to avoid late penalties, which increase premiums by 10% for each 12-month period you delay. Medicaid applicants should gather proof of income, citizenship, and residency to streamline the process. Additionally, dual-eligible individuals (qualifying for both Medicare and Medicaid) can benefit from coordinated care through special programs, ensuring comprehensive coverage without out-of-pocket costs. Staying informed about policy changes and state-specific rules is essential for maximizing benefits.

Apply for Insurance Collection in Pennsylvania: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Uninsured rates by state

As of recent data, Texas leads the nation with the highest uninsured rate, hovering around 18%, significantly above the national average of approximately 9%. This disparity highlights the stark differences in healthcare access across states, influenced by factors such as Medicaid expansion, income levels, and policy decisions. For instance, states that have expanded Medicaid under the Affordable Care Act (ACA) tend to have lower uninsured rates, while those that have not, like Texas, see higher percentages of uninsured residents. Understanding these state-by-state variations is crucial for policymakers and advocates aiming to reduce the uninsured population.

Consider Massachusetts, which boasts one of the lowest uninsured rates in the country, at around 3%. This success can be attributed to its early adoption of health reform in 2006, which served as a model for the ACA. The state’s approach included mandates for individuals to have insurance and for employers to offer coverage, coupled with subsidies for low-income residents. This example illustrates how proactive policy measures can dramatically reduce uninsured rates, even in a diverse economic landscape. Other states could emulate such strategies to improve their own healthcare coverage outcomes.

In contrast, Southern states like Mississippi and Georgia, with uninsured rates of 13% and 12% respectively, face persistent challenges. These states have not expanded Medicaid, leaving a coverage gap for low-income adults who earn too much to qualify for traditional Medicaid but too little to afford private insurance. This gap disproportionately affects rural and minority populations, exacerbating health disparities. Addressing this issue requires not only policy changes but also community-based initiatives to educate residents about available resources and enrollment processes.

For individuals living in states with high uninsured rates, practical steps can make a difference. First, explore state-run health insurance marketplaces, which offer subsidized plans based on income. Second, check eligibility for Medicaid, even if your state hasn’t expanded it, as children and some low-income adults may still qualify. Third, consider community health centers, which provide care on a sliding fee scale regardless of insurance status. Finally, stay informed about legislative changes, as shifts in policy can open new opportunities for coverage.

In conclusion, uninsured rates by state reveal a patchwork of access to healthcare across the U.S., shaped by policy decisions, economic factors, and demographic trends. While some states have achieved near-universal coverage, others continue to struggle with significant gaps. By examining successful models and addressing barriers in high-uninsured states, there is potential to reduce disparities and improve health outcomes nationwide. This requires a combination of policy reform, community engagement, and individual action to ensure that healthcare becomes a reality for all Americans.

Why Insurance Companies Invest in Luxurious Skyscrapers: Unveiling the Strategy

You may want to see also

Explore related products

![]()

Impact of Affordable Care Act

The Affordable Care Act (ACA), often referred to as Obamacare, has significantly reshaped the landscape of health insurance coverage in the United States. Since its implementation in 2010, the percentage of uninsured Americans has dropped dramatically. According to the Centers for Disease Control and Prevention (CDC), the uninsured rate fell from 16% in 2010 to 8.6% in 2016, marking a historic low. This reduction is largely attributed to the ACA’s key provisions, such as the expansion of Medicaid and the establishment of health insurance marketplaces, which made coverage more accessible and affordable for millions.

One of the most impactful aspects of the ACA has been Medicaid expansion. States that expanded Medicaid eligibility saw a more substantial decrease in uninsured rates compared to those that did not. For example, in Kentucky, which embraced expansion, the uninsured rate plummeted from 14.3% in 2013 to 5.1% in 2016. In contrast, states like Texas, which opted out of expansion, experienced slower progress. This disparity highlights the critical role state-level decisions play in maximizing the ACA’s potential to increase coverage.

Beyond Medicaid, the ACA introduced subsidies to help lower-income individuals purchase private insurance through marketplaces. These subsidies, available to those earning between 100% and 400% of the federal poverty level, have made health insurance affordable for millions. For instance, a family of four earning up to $106,000 annually in 2023 could qualify for assistance, significantly reducing their monthly premiums. This financial support has been instrumental in driving up enrollment numbers, particularly among younger and healthier populations, which are essential for stabilizing insurance markets.

However, the ACA’s impact isn’t without challenges. Critics argue that rising premiums and limited provider networks in some areas have offset its benefits. For example, in rural regions, where healthcare infrastructure is already strained, access to affordable plans remains a concern. Despite these issues, the ACA’s protections for pre-existing conditions and the elimination of lifetime coverage caps have provided security for millions. A 2022 Kaiser Family Foundation survey found that 58% of Americans view the ACA favorably, underscoring its enduring importance in the healthcare debate.

To maximize the ACA’s benefits, individuals should take proactive steps. First, understand your eligibility for subsidies by using the marketplace’s online calculator. Second, enroll during the annual open enrollment period (typically November 1 to January 15) to avoid gaps in coverage. Finally, if your state hasn’t expanded Medicaid, advocate for policy changes that could extend coverage to more residents. The ACA’s success depends not only on federal legislation but also on informed, engaged citizens leveraging its tools to secure their health and financial well-being.

Understanding Japan's Private Health Insurance: Coverage, Costs, and Benefits

You may want to see also

Explore related products

![]()

Age and income demographics

As of recent data, approximately 91% of the U.S. population has health insurance, but this figure masks significant disparities when broken down by age and income. Younger adults, aged 18–24, are the least insured demographic, with only about 85% coverage, often due to transitioning from parental plans or entering the workforce without employer-sponsored benefits. In contrast, individuals aged 65 and older, eligible for Medicare, boast near-universal coverage at 99%. This stark difference highlights how age-specific policies and life stages critically influence insurance rates.

Income level further complicates the picture, acting as both a barrier and a determinant of coverage type. Among households earning below the federal poverty level, only 78% have insurance, despite the Affordable Care Act’s expansions. Low-income families often face gaps in Medicaid eligibility, particularly in states that have not expanded the program. Conversely, households earning over $100,000 annually achieve a 97% coverage rate, primarily through employer-sponsored plans. This income-based divide underscores the role of economic stability in accessing consistent healthcare.

For those aged 25–64, income becomes a pivotal factor in navigating the insurance landscape. Middle-income earners ($40,000–$75,000) often face the highest premiums relative to their income, with many opting for high-deductible plans to reduce monthly costs. This group represents a critical demographic for policy interventions, as they are too affluent for subsidies but struggle with affordability. Practical tips for this cohort include exploring health savings accounts (HSAs) to offset out-of-pocket expenses and leveraging state-based marketplaces for premium tax credits.

Children under 18, however, exhibit a more uniform coverage rate of 95%, largely due to the Children’s Health Insurance Program (CHIP) and Medicaid. This success story demonstrates how targeted policies can bridge demographic gaps. Yet, even here, income disparities persist: children in households earning below $25,000 are twice as likely to be uninsured compared to those in higher-income families. Addressing these residual gaps requires expanding outreach and simplifying enrollment processes for low-income families.

In conclusion, age and income demographics are inextricably linked to health insurance coverage in the U.S. Policymakers and individuals alike must recognize these intersections to craft solutions that reduce disparities. For younger adults, expanding access to affordable plans and educating on enrollment options is key. For low-income households, closing the Medicaid gap and enhancing subsidies could significantly improve coverage. By targeting these specific demographics, the U.S. can move closer to achieving equitable healthcare access for all.

Free Medical Insurance: Sign Up and Stay Covered

You may want to see also

Frequently asked questions

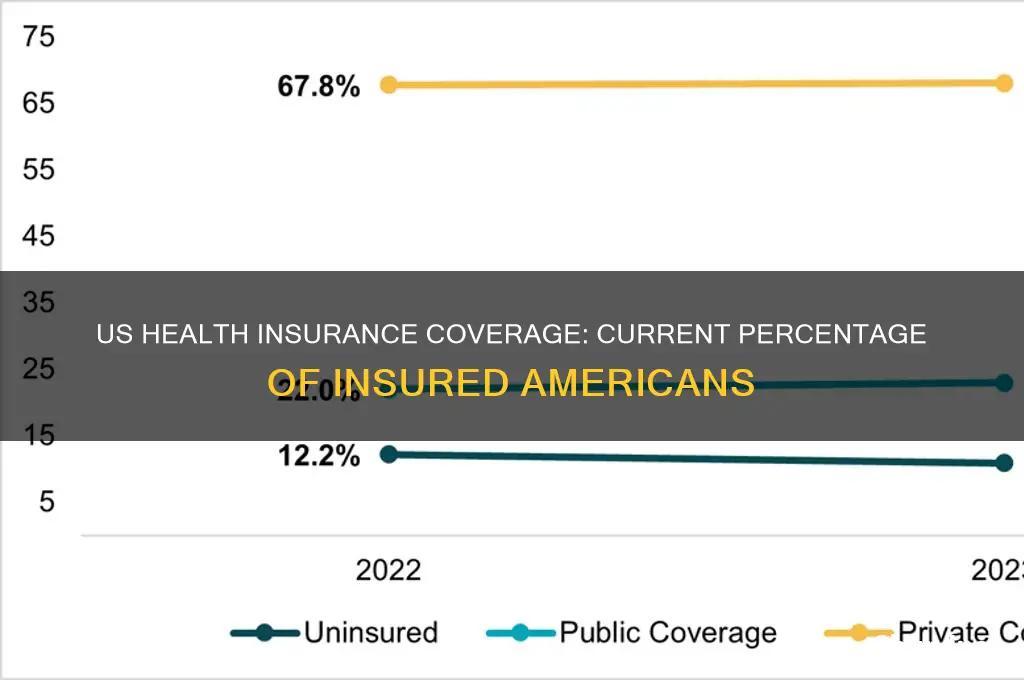

As of 2023, approximately 91% of the U.S. population has health insurance, according to data from the Centers for Disease Control and Prevention (CDC) and the U.S. Census Bureau.

The percentage of insured Americans has increased significantly over the past decade, largely due to the Affordable Care Act (ACA). In 2010, about 84% of the population had health insurance, compared to around 91% in 2023.

Older adults aged 65 and above have the highest percentage of health insurance coverage, primarily due to Medicare. Nearly 100% of this age group is insured, compared to younger demographics where coverage rates are lower.