The Affordable Care Act (ACA), commonly known as Obamacare, significantly reduced the number of uninsured Americans by expanding access to health insurance through Medicaid expansion, the establishment of health insurance marketplaces, and the introduction of subsidies to make coverage more affordable. By 2016, the uninsured rate had dropped from approximately 16% in 2010 to around 8.6%, representing millions of previously uninsured individuals gaining coverage. Key provisions such as allowing young adults to stay on their parents’ plans until age 26 and prohibiting denial of coverage for pre-existing conditions also contributed to this decline. While the exact number of uninsured who gained insurance varies by source and methodology, estimates suggest that over 20 million Americans obtained coverage as a direct result of the ACA’s implementation.

| Characteristics | Values |

|---|---|

| Total Reduction in Uninsured Rate (2010-2019) | Approximately 20 million people gained health insurance coverage |

| Uninsured Rate in 2010 (Pre-ACA) | 16.0% |

| Uninsured Rate in 2019 (Latest Data) | 8.9% |

| Largest Coverage Gains | Medicaid expansion states |

| Young Adult Coverage (Ages 19-25) | Increased by 10.3 percentage points (due to dependent coverage provision) |

| Non-Elderly Uninsured Rate (2010 vs 2019) | 21% vs 10.9% |

| Medicaid/CHIP Enrollment Increase (2013-2019) | Over 14 million additional enrollees in expansion states |

| Marketplace Enrollment (2020) | 11.4 million individuals |

| Sources of Coverage Gains | Medicaid (60%), Marketplace plans (25%), Employer-based coverage (15%) |

| Impact on Racial Disparities | Uninsured rates among Black and Hispanic individuals decreased significantly |

| Latest Data Year | 2019 (Note: Some sources may have updated figures through 2021, but 2019 remains the most comprehensive benchmark) |

Explore related products

What You'll Learn

- Enrollment Numbers: Total individuals gaining coverage through ACA marketplaces and Medicaid expansion

- Demographic Shifts: Breakdown of insured by age, income, and racial/ethnic groups

- State Variations: Differences in uninsured rates across states with/without Medicaid expansion

- Impact on Uninsured Rate: National uninsured rate reduction post-ACA implementation

- Long-Term Trends: Sustained coverage gains and fluctuations since ACA’s inception

![]()

Enrollment Numbers: Total individuals gaining coverage through ACA marketplaces and Medicaid expansion

The Affordable Care Act (ACA), often referred to as Obamacare, has significantly reduced the number of uninsured Americans by expanding coverage through its marketplaces and Medicaid expansion. By 2016, approximately 20 million previously uninsured individuals had gained health insurance, according to the U.S. Department of Health and Human Services. This dramatic shift underscores the ACA’s role in addressing long-standing gaps in healthcare access. The majority of these gains came from two primary channels: the ACA marketplaces, which offer subsidized private insurance plans, and Medicaid expansion, which extended eligibility to low-income adults in participating states.

To understand the impact, consider the mechanics of enrollment. The ACA marketplaces provided a platform for individuals and families to purchase affordable health plans, often with premium tax credits reducing costs. For example, a family of four earning up to $100,000 annually might qualify for subsidies, significantly lowering their monthly premiums. Simultaneously, Medicaid expansion targeted adults with incomes up to 138% of the federal poverty level (FPL), a group previously ineligible in many states. This dual approach ensured that both working-class families and those with very low incomes could access coverage.

However, enrollment numbers vary widely by state due to differing policies on Medicaid expansion. As of 2023, 40 states and the District of Columbia have adopted expansion, covering over 12 million additional individuals. In contrast, states that opted out, such as Texas and Florida, saw persistently higher uninsured rates. For instance, Texas, with its large uninsured population, could have covered an estimated 1.5 million more residents if it had expanded Medicaid. This disparity highlights the critical role state-level decisions play in the ACA’s overall success.

Practical tips for maximizing enrollment include leveraging open enrollment periods, typically from November 1 to January 15, and utilizing healthcare navigators or brokers to explore available options. For Medicaid, eligibility can be checked year-round, and applicants should gather income documentation to streamline the process. Additionally, understanding the ACA’s protections, such as guaranteed coverage for pre-existing conditions, can encourage more individuals to enroll without fear of denial.

In conclusion, the ACA’s marketplaces and Medicaid expansion have been transformative, but their full potential remains untapped in non-expansion states. By focusing on these channels and addressing barriers to enrollment, further reductions in the uninsured population are achievable. The data is clear: millions have benefited, but millions more could still gain coverage with targeted efforts and policy changes.

What Happens to Your Insurance Coverage When Your Policy Lapses?

You may want to see also

Explore related products

$28.99 $37.99

![]()

Demographic Shifts: Breakdown of insured by age, income, and racial/ethnic groups

The Affordable Care Act (ACA), often referred to as Obamacare, significantly reduced the number of uninsured Americans, but the impact wasn’t uniform across demographics. Analyzing the breakdown by age, income, and racial/ethnic groups reveals where the most substantial shifts occurred. For instance, young adults aged 19–25 experienced a notable increase in coverage due to the ACA’s provision allowing them to remain on their parents’ insurance plans until age 26. This single policy change contributed to a 10-percentage-point drop in uninsured rates among this age group between 2010 and 2016, according to the Centers for Disease Control and Prevention (CDC).

Income played a pivotal role in determining who gained coverage under the ACA. Low-income individuals, particularly those in states that expanded Medicaid, saw the most dramatic improvements. In expansion states, the uninsured rate among adults with incomes below 138% of the federal poverty level (FPL) dropped from 36% in 2013 to 14% in 2019, as reported by the Kaiser Family Foundation. Conversely, in non-expansion states, this group’s uninsured rate remained stubbornly high at 29%. This disparity underscores the importance of state-level policy decisions in shaping access to care.

Racial and ethnic disparities in insurance coverage narrowed but persisted post-ACA. Hispanic individuals, historically one of the most uninsured groups, saw their uninsured rate drop from 32% in 2013 to 19% in 2019. However, they still lag behind non-Hispanic whites, whose uninsured rate fell to 7% during the same period. Similarly, Black Americans experienced a significant decline in uninsured rates, from 21% to 11%, but gaps remain due to systemic barriers like income inequality and limited access to employer-sponsored insurance.

To maximize the ACA’s impact on these demographic shifts, practical steps can be taken. For young adults, leveraging the dependent coverage provision until age 26 is a no-brainer. Low-income individuals should check their state’s Medicaid expansion status and enroll if eligible, as this remains the most cost-effective pathway to coverage. Racial and ethnic minorities can benefit from targeted outreach programs, such as those offered by community health centers, which provide culturally competent enrollment assistance.

In conclusion, while the ACA made strides in reducing uninsured rates, the demographic breakdown highlights areas for improvement. Policymakers and advocates must address lingering disparities by expanding Medicaid in non-expansion states, enhancing outreach to underserved communities, and tackling systemic barriers to equitable access. By doing so, the promise of universal coverage can move closer to reality.

Who Can Be a Life Insurance Beneficiary?

You may want to see also

Explore related products

$39.97

![]()

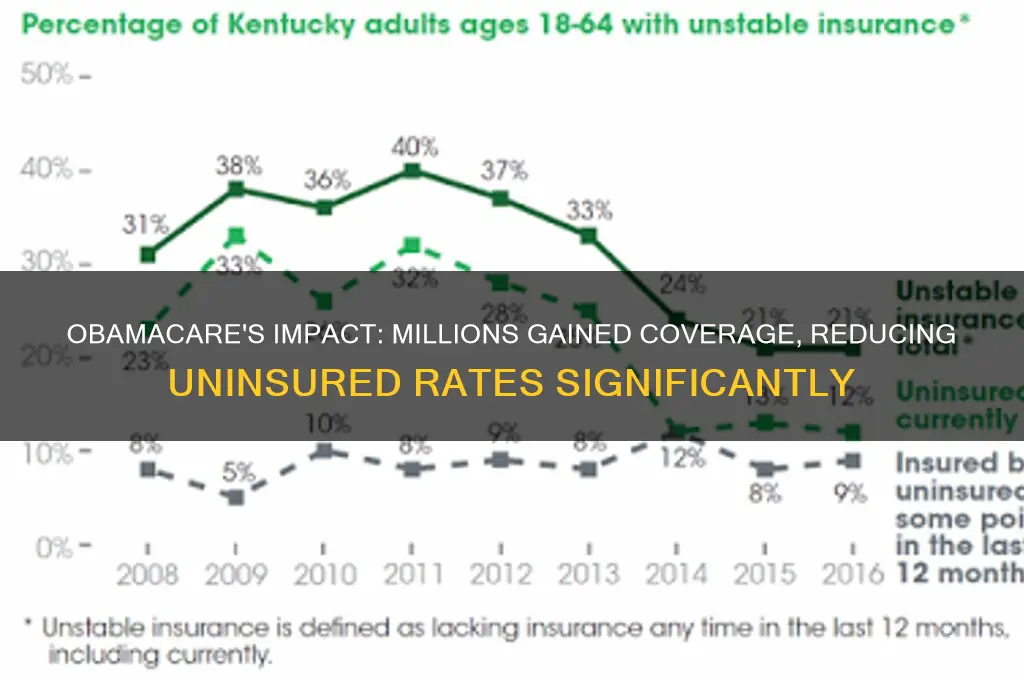

State Variations: Differences in uninsured rates across states with/without Medicaid expansion

The Affordable Care Act (ACA), often referred to as Obamacare, introduced a significant policy lever to reduce uninsured rates: Medicaid expansion. States that embraced this expansion saw a dramatic drop in uninsured populations, particularly among low-income adults. For instance, Kentucky, which expanded Medicaid, witnessed its uninsured rate plummet from 14.3% in 2013 to 5.8% by 2019. Conversely, states like Texas, which opted out of expansion, experienced far more modest declines, with uninsured rates remaining stubbornly high at around 18% in 2019. This stark contrast highlights the critical role state-level decisions play in shaping healthcare access.

Consider the mechanics of Medicaid expansion: it extends eligibility to adults earning up to 138% of the federal poverty level (FPL), a threshold that captures millions previously ineligible for traditional Medicaid. In expansion states, this policy effectively bridges the gap for individuals who earn too much for traditional Medicaid but too little to afford private insurance. For example, a single adult earning $18,000 annually—138% of the 2023 FPL—would qualify in expansion states but remain uninsured in non-expansion states unless they find employer-sponsored coverage or pay out-of-pocket for marketplace plans.

The impact of these decisions extends beyond raw numbers. Non-expansion states often see higher rates of uncompensated care, straining hospital systems and local economies. A 2020 study found that hospitals in expansion states experienced a 24% reduction in uncompensated care costs compared to their non-expansion counterparts. This financial relief translates into better-equipped healthcare facilities and more stable rural hospitals, which are disproportionately affected by high uninsured rates. For policymakers, this data underscores the economic argument for expansion: it’s not just about coverage but also about fiscal responsibility.

Practical implications for individuals in non-expansion states are dire. Without Medicaid expansion, the so-called “coverage gap” leaves approximately 2.2 million adults ineligible for both Medicaid and ACA premium subsidies. These individuals, often working in low-wage jobs without employer-sponsored insurance, face limited options. Advocacy groups recommend they explore local health clinics, which may offer sliding-scale fees, or seek short-term health plans, though these often exclude pre-existing conditions. However, these solutions are stopgaps, not substitutes for comprehensive coverage.

In conclusion, the divide between expansion and non-expansion states reveals a policy-driven health disparity. While the ACA provided a framework for universal coverage, its success hinges on state participation in Medicaid expansion. For states still on the fence, the evidence is clear: expansion not only reduces uninsured rates but also strengthens healthcare systems and local economies. For individuals, understanding these state-level differences is crucial in navigating their healthcare options—and advocating for policies that close the coverage gap.

Optimal Fire Hydrant Distance for Insurance Coverage and Safety

You may want to see also

Explore related products

$31.73 $34.97

$9.09 $10.99

![]()

Impact on Uninsured Rate: National uninsured rate reduction post-ACA implementation

The Affordable Care Act (ACA), colloquially known as Obamacare, has been a transformative force in the American healthcare landscape, particularly in its impact on the uninsured rate. One of the most significant achievements of the ACA has been the substantial reduction in the number of uninsured individuals across the nation. Data from the Centers for Disease Control and Prevention (CDC) and the U.S. Census Bureau reveal a dramatic decline in the uninsured rate from 16.0% in 2010, the year the ACA was signed into law, to 8.6% in 2016, representing millions of previously uninsured Americans gaining coverage.

To understand the magnitude of this reduction, consider the following breakdown: between 2013 and 2016, approximately 20 million adults gained health insurance coverage. This shift was driven by key provisions of the ACA, such as the expansion of Medicaid eligibility, the establishment of health insurance marketplaces, and the allowance for young adults to remain on their parents’ plans until age 26. States that expanded Medicaid saw even more pronounced declines in uninsured rates, with some experiencing reductions of over 10 percentage points. For instance, Kentucky’s uninsured rate dropped from 14.3% in 2013 to 5.1% in 2016, a testament to the policy’s effectiveness when fully implemented.

However, the impact of the ACA on uninsured rates is not uniform across demographics. While the law has significantly benefited low-income individuals and families, disparities persist. For example, uninsured rates remain higher among Hispanic and American Indian/Alaska Native populations compared to other racial and ethnic groups. Additionally, states that have not expanded Medicaid continue to struggle with higher uninsured rates, highlighting the importance of state-level policy decisions in maximizing the ACA’s potential. Addressing these gaps requires targeted efforts, such as increasing outreach to underserved communities and incentivizing non-expansion states to adopt Medicaid expansion.

A critical takeaway from the ACA’s impact on uninsured rates is the importance of sustained policy commitment. The law’s success in reducing the uninsured rate demonstrates that comprehensive healthcare reform can yield measurable results. However, maintaining these gains requires ongoing support for ACA provisions, including funding for marketplace subsidies and continued efforts to enroll eligible individuals in Medicaid. Policymakers and advocates must also address emerging challenges, such as rising premiums and limited provider networks, to ensure that coverage remains accessible and affordable for all Americans.

Practical steps to build on the ACA’s success include expanding Medicaid in non-expansion states, simplifying enrollment processes, and increasing funding for community health centers. Individuals can contribute by staying informed about open enrollment periods and available subsidies, while employers can play a role by offering affordable health insurance options to their employees. By combining policy action with grassroots efforts, the nation can further reduce the uninsured rate and move closer to the goal of universal healthcare coverage. The ACA’s impact serves as both a milestone and a foundation for future progress in ensuring health security for all.

How to Cancel Your Aviva Life Insurance Policy

You may want to see also

Explore related products

![]()

Long-Term Trends: Sustained coverage gains and fluctuations since ACA’s inception

The Affordable Care Act (ACA), colloquially known as Obamacare, has reshaped the American health insurance landscape since its inception in 2010. One of its most significant achievements is the substantial reduction in the uninsured rate, which plummeted from 16% in 2010 to 8.6% by 2016. This translates to approximately 20 million previously uninsured individuals gaining coverage, a testament to the ACA’s transformative impact. However, this progress hasn’t been linear. Fluctuations in coverage rates, driven by policy changes, economic shifts, and political debates, highlight the dynamic nature of healthcare reform.

To understand these long-term trends, consider the ACA’s core mechanisms: Medicaid expansion, health insurance marketplaces, and subsidies for low-income individuals. States that embraced Medicaid expansion saw sharper declines in uninsured rates compared to those that did not. For instance, Kentucky’s uninsured rate dropped from 14.3% in 2013 to 5.8% in 2016 after expanding Medicaid, while Texas, which opted out, saw a more modest decline from 22.1% to 16.6%. This disparity underscores the importance of state-level decisions in sustaining coverage gains.

Despite these successes, the ACA’s trajectory has faced challenges. The elimination of the individual mandate penalty in 2019, coupled with rising premiums, led to a slight uptick in uninsured rates, particularly among younger, healthier individuals who opted out of coverage. By 2021, the uninsured rate had risen to 9.1%, reversing some of the earlier gains. However, recent data shows a rebound, with the uninsured rate dropping to 8.3% in 2023, fueled by enhanced subsidies under the American Rescue Plan and increased enrollment during the COVID-19 pandemic.

A critical takeaway is the ACA’s resilience in the face of adversity. Its ability to adapt to changing circumstances, such as the pandemic-era expansion of special enrollment periods and increased outreach efforts, has been pivotal. For policymakers and advocates, this underscores the need for continued investment in enrollment assistance, premium subsidies, and public awareness campaigns. Individuals can maximize their benefits by exploring all available options during open enrollment, leveraging tax credits, and staying informed about policy updates.

In conclusion, the ACA’s long-term trends reveal a story of sustained progress punctuated by fluctuations. While challenges remain, the act’s foundational reforms have undeniably expanded access to healthcare. By learning from past successes and setbacks, stakeholders can work toward a future where coverage gains are not only sustained but deepened, ensuring health insurance remains a right, not a privilege.

Understanding Conversion Privilege in Life Insurance Policies

You may want to see also

Frequently asked questions

Estimates vary, but approximately 20 million previously uninsured Americans gained health coverage as a result of the Affordable Care Act by 2016, according to the U.S. Department of Health and Human Services and the Congressional Budget Office.

The uninsured rate in the U.S. dropped significantly under Obamacare, from about 16% in 2010 to around 9% by 2016, representing a reduction of nearly half the uninsured population.

No, the impact varied by state. States that expanded Medicaid under the ACA saw larger reductions in uninsured rates compared to those that did not expand Medicaid, with expansion states experiencing a more significant drop in uninsured populations.