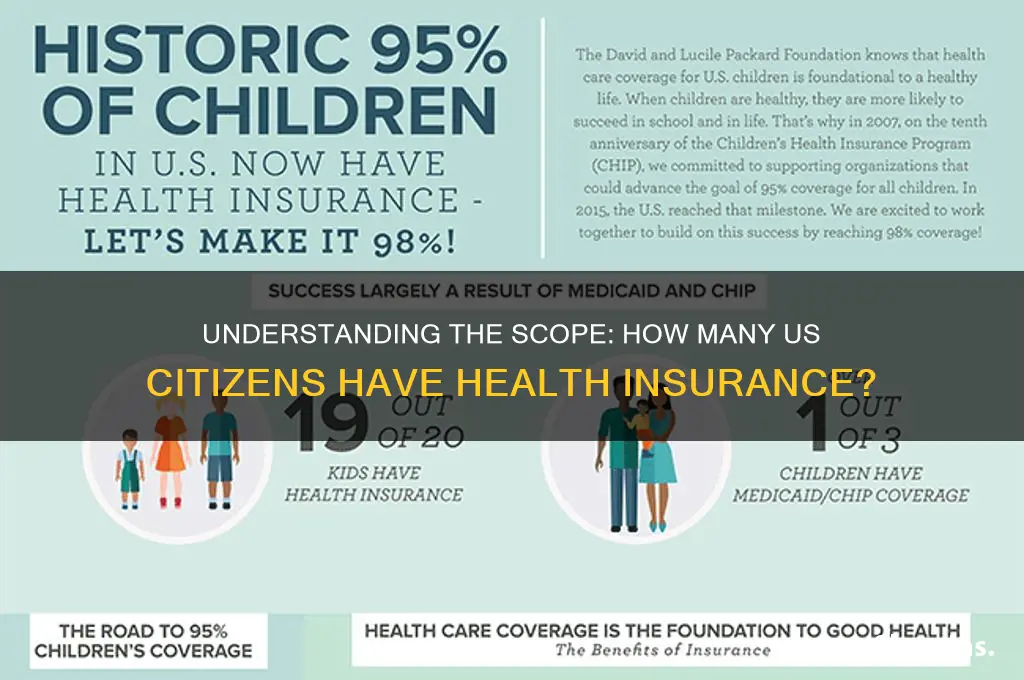

The number of U.S. citizens with health insurance is a critical indicator of the nation's healthcare accessibility and overall well-being. As of recent data, approximately 91% of Americans are covered by some form of health insurance, a significant increase from previous decades due to policy reforms like the Affordable Care Act (ACA). Coverage is primarily divided among employer-sponsored plans, Medicaid, Medicare, and individual marketplace plans. Despite this progress, millions remain uninsured, often due to affordability issues, eligibility gaps, or state-level policy differences, highlighting ongoing challenges in achieving universal coverage. Understanding these figures is essential for addressing disparities and shaping future healthcare policies.

Explore related products

What You'll Learn

- Employer-Sponsored Coverage: Percentage of citizens insured through workplace plans, including full-time and part-time employees

- Medicare Enrollment: Number of seniors and disabled individuals covered by federal Medicare programs

- Medicaid Participation: State-specific enrollment rates in Medicaid for low-income citizens

- Individual Market Plans: Citizens purchasing private insurance directly through exchanges or providers

- Uninsured Population: Demographics and reasons for lack of health insurance among U.S. citizens

![]()

Employer-Sponsored Coverage: Percentage of citizens insured through workplace plans, including full-time and part-time employees

Employer-sponsored health insurance remains the cornerstone of coverage for millions of Americans, with approximately 56% of the non-elderly population insured through workplace plans as of 2023. This figure underscores the critical role employers play in providing access to healthcare, particularly for full-time workers, where the coverage rate jumps to nearly 70%. However, part-time employees face a stark disparity, with only about 25% offered employer-sponsored plans, highlighting a significant gap in access based on employment status.

Analyzing the trends reveals a gradual decline in employer-sponsored coverage over the past two decades, partly due to rising costs and shifting workforce dynamics. Small businesses, in particular, struggle to offer competitive health benefits, with only 47% of firms with fewer than 50 employees providing insurance, compared to 96% of large firms. This disparity disproportionately affects low-wage workers, who are more likely to work for smaller companies or in part-time roles. Policymakers and employers must address these inequities to ensure broader access, such as by expanding tax incentives for small businesses or mandating coverage for part-time workers.

From a practical standpoint, employees should carefully evaluate their workplace health plans during open enrollment periods. Key factors to consider include premiums, deductibles, and network coverage, as these can significantly impact out-of-pocket costs. For instance, a high-deductible health plan (HDHP) paired with a Health Savings Account (HSA) may be cost-effective for healthy individuals, while families might benefit from plans with lower deductibles and broader provider networks. Part-time workers, often excluded from employer plans, should explore alternatives like the Affordable Care Act (ACA) marketplace, where subsidies can reduce premiums for those earning up to 400% of the federal poverty level.

Comparatively, employer-sponsored insurance offers advantages over individual plans, such as shared premium costs and guaranteed issue, meaning employees cannot be denied coverage due to pre-existing conditions. However, it also limits portability, as workers may lose coverage when changing jobs or during layoffs. To mitigate this risk, employees should consider purchasing short-term health plans or COBRA continuation coverage, though these options are often more expensive. Ultimately, understanding the nuances of employer-sponsored insurance is essential for maximizing benefits and ensuring continuous coverage in an evolving healthcare landscape.

Luxottica's Eye Insurance Ownership: Which Company Do They Control?

You may want to see also

Explore related products

![]()

Medicare Enrollment: Number of seniors and disabled individuals covered by federal Medicare programs

As of 2023, over 65 million Americans are enrolled in Medicare, a federal health insurance program primarily serving individuals aged 65 and older, as well as younger people with certain disabilities or end-stage renal disease. This figure represents approximately 20% of the U.S. population, making Medicare a cornerstone of the nation’s healthcare system. Among enrollees, about 57 million are seniors aged 65 and older, while the remaining 8 million are disabled individuals under 65. These numbers highlight the program’s critical role in providing coverage to vulnerable populations who might otherwise face significant barriers to accessing healthcare.

Breaking down enrollment further, Medicare consists of several parts, each covering different services. Part A, which covers hospital stays, is nearly universal among enrollees, with over 99% of Medicare beneficiaries enrolled. Part B, covering outpatient services, is selected by about 92% of participants. Additionally, roughly 48% of beneficiaries opt for Medicare Advantage (Part C) plans, which are private insurance alternatives to traditional Medicare. Prescription drug coverage (Part D) is chosen by approximately 73% of enrollees, reflecting its importance in managing chronic conditions common among seniors and disabled individuals.

Enrollment trends reveal both demographic shifts and policy impacts. The aging of the Baby Boomer generation has driven steady growth in Medicare enrollment, with projections indicating that the number of beneficiaries will reach 80 million by 2030. However, enrollment among disabled individuals under 65 has remained relatively stable, influenced by factors such as Social Security Disability Insurance (SSDI) eligibility criteria and state-level Medicaid expansion. Policymakers must consider these trends when addressing funding, coverage gaps, and long-term sustainability.

For seniors and disabled individuals, understanding Medicare enrollment is essential for maximizing benefits. Eligibility begins three months before an individual’s 65th birthday, and late enrollment can result in penalties. Disabled individuals typically become eligible after receiving SSDI benefits for 24 months. Practical tips include reviewing the annual “Medicare & You” handbook, comparing Part D plans during the Open Enrollment Period (October 15–December 7), and exploring supplemental coverage options like Medigap policies. Proactive planning ensures beneficiaries access the full range of services they need without unexpected costs.

In comparison to other health insurance programs, Medicare stands out for its comprehensive coverage and broad eligibility criteria. While employer-sponsored insurance and Medicaid cover larger portions of the population, Medicare’s focus on seniors and disabled individuals addresses a unique gap in the healthcare system. However, challenges such as out-of-pocket costs and limited dental, vision, and hearing coverage persist. Advocates argue for expansions like adding dental benefits, a change that could significantly improve quality of life for millions. As debates continue, Medicare remains a vital safety net, underscoring the need for informed enrollment decisions and ongoing policy reforms.

Medical Insurance: Options for Tourists Abroad

You may want to see also

Explore related products

![]()

Medicaid Participation: State-specific enrollment rates in Medicaid for low-income citizens

As of recent data, approximately 91% of Americans have health insurance, with Medicaid covering a significant portion of low-income individuals. However, Medicaid participation varies widely by state, influenced by factors such as eligibility criteria, policy decisions, and socioeconomic conditions. Understanding these state-specific enrollment rates is crucial for assessing the effectiveness of Medicaid in reaching its intended population.

Consider the stark differences between states like California and Texas. California, with its expansive Medicaid program (Medi-Cal), covers over 14 million residents, representing about 35% of its population. This high enrollment rate is partly due to the state’s decision to adopt the Affordable Care Act’s Medicaid expansion, which extended eligibility to adults earning up to 138% of the federal poverty level. In contrast, Texas, which has not expanded Medicaid, covers only about 17% of its population, leaving over 1.5 million low-income adults in the "coverage gap"—earning too much for traditional Medicaid but too little for marketplace subsidies. This example highlights how policy choices directly impact enrollment rates and access to care.

To analyze these disparities, examine the role of federal and state policies. States that expanded Medicaid under the ACA saw an average enrollment increase of 25% compared to non-expansion states. For instance, Kentucky’s expansion led to a 70% reduction in its uninsured rate, while neighboring Tennessee, which did not expand, saw minimal changes. Additionally, states with streamlined enrollment processes, such as online applications and automatic renewals, tend to have higher participation rates. For example, New York’s simplified enrollment system has contributed to its Medicaid coverage of over 7 million residents, or about 36% of its population.

Practical steps for improving Medicaid participation include advocating for expansion in non-expansion states, as this single policy change could cover up to 4 million uninsured adults. States can also invest in outreach campaigns targeting eligible populations, particularly in rural or underserved areas. For instance, Michigan’s "Healthy Michigan" campaign successfully enrolled over 600,000 residents by leveraging community partnerships and multilingual resources. Another strategy is to align Medicaid eligibility with other safety-net programs, such as SNAP, to reduce administrative barriers and increase enrollment efficiency.

In conclusion, Medicaid participation is not just a numbers game but a reflection of state-level commitment to health equity. By studying enrollment rates, policymakers and advocates can identify gaps, implement targeted solutions, and ensure that low-income citizens have access to essential healthcare services. The data is clear: expansion and simplification work, and states that prioritize these strategies can significantly reduce uninsured rates and improve public health outcomes.

Trulicity Insurance Coverage: Which Companies Offer This Diabetes Medication?

You may want to see also

Explore related products

![]()

Individual Market Plans: Citizens purchasing private insurance directly through exchanges or providers

In the United States, approximately 14.3 million citizens purchase health insurance through the individual market, either directly from providers or via exchanges established under the Affordable Care Act (ACA). This segment represents a critical pathway for those who lack employer-sponsored coverage or government-funded options like Medicare or Medicaid. Unlike group plans, individual market plans offer personalized choices but require careful navigation to balance cost and coverage.

Analyzing the Landscape: Exchanges vs. Direct Providers

Health insurance exchanges, such as Healthcare.gov, serve as centralized platforms where individuals compare standardized plans categorized by metal tiers (Bronze, Silver, Gold, Platinum). These plans must cover essential health benefits, including preventive care, prescription drugs, and maternity care. Premiums vary by age, location, and income, with subsidies available for those earning up to 400% of the federal poverty level. Conversely, purchasing directly from providers (e.g., Aetna, UnitedHealthcare) allows for more tailored options, including short-term plans or high-deductible health plans paired with Health Savings Accounts (HSAs). However, direct purchases bypass subsidies and may exclude ACA protections like pre-existing condition coverage.

Practical Tips for Enrolling in Individual Plans

When selecting an individual market plan, start by assessing your healthcare needs. For instance, a 30-year-old with no chronic conditions might opt for a Bronze plan with lower premiums but higher out-of-pocket costs, while a family with frequent medical visits may benefit from a Gold plan’s lower deductibles. Use exchange platforms to estimate annual costs, including premiums, deductibles, and copays. If purchasing directly, verify that the plan complies with ACA regulations unless you’re specifically seeking short-term coverage. Enroll during the Open Enrollment Period (November 1 to January 15) or qualify for a Special Enrollment Period due to life events like marriage or job loss.

Comparing Costs and Coverage

Individual market plans often cost more than employer-sponsored insurance due to the absence of employer contributions. For example, the average monthly premium for a 40-year-old on a Silver plan in 2023 was $485, though subsidies reduced this to $175 for eligible individuals. Direct provider plans may offer lower premiums but often exclude ACA mandates, such as maternity care or mental health services. Short-term plans, while cheaper (starting at $100/month), cap coverage at 365 days and exclude pre-existing conditions. Weigh these trade-offs against your health risks and financial stability.

The Role of Subsidies and Tax Credits

Premium tax credits are a cornerstone of affordability in the individual market. For instance, a single adult earning $30,000 annually in 2023 could save up to $200/month on a Silver plan through subsidies. Additionally, cost-sharing reductions (CSRs) lower out-of-pocket costs for those earning up to 250% of the poverty level. To maximize savings, use the exchange’s subsidy calculator and apply during enrollment. Direct provider plans do not qualify for these subsidies, making them less cost-effective for lower-income individuals.

Choosing an individual market plan requires balancing personalization with protection. Exchanges offer ACA-compliant plans with potential subsidies, ideal for those seeking comprehensive coverage. Direct provider plans provide flexibility but may lack critical benefits. By evaluating your health needs, budget, and eligibility for financial assistance, you can secure a plan that aligns with your lifestyle. Remember, the individual market is not one-size-fits-all—it’s a tailored solution for those willing to invest time in research and comparison.

Short-Term Health Insurance: Can It Help You Avoid ACA Penalties?

You may want to see also

Explore related products

![]()

Uninsured Population: Demographics and reasons for lack of health insurance among U.S. citizens

As of recent data, approximately 8.5% of the U.S. population, or about 28 million people, remain uninsured. This figure, while lower than pre-Affordable Care Act (ACA) levels, highlights persistent gaps in coverage. Understanding who these individuals are and why they lack insurance is crucial for addressing this issue effectively.

Demographics of the Uninsured

The uninsured population is not evenly distributed across the U.S. demographic landscape. Young adults aged 18–34 represent a significant portion, often due to perceived good health and lower prioritization of insurance. Low-income individuals, particularly those in states that have not expanded Medicaid under the ACA, face higher uninsured rates. For instance, in non-expansion states, nearly 1 in 5 low-income adults lacks coverage. Racial and ethnic disparities persist, with Hispanic and American Indian/Alaska Native populations experiencing uninsured rates of 19% and 16%, respectively, compared to 8% for non-Hispanic Whites.

Economic Barriers to Coverage

Cost remains the most cited reason for lacking insurance. Despite ACA subsidies, many find premiums, deductibles, and out-of-pocket costs prohibitive. For example, a family of four earning just above the federal poverty level ($28,000 annually) may still face premiums exceeding $500 monthly, even with subsidies. Additionally, the "coverage gap" in non-expansion states leaves individuals earning too much for traditional Medicaid but too little for marketplace subsidies without affordable options.

Structural and Policy Factors

Policy decisions play a pivotal role in uninsured rates. States that expanded Medicaid saw uninsured rates drop by an average of 10 percentage points more than non-expansion states. Immigration status also influences coverage, as undocumented immigrants are ineligible for most federal programs, and mixed-status families may avoid enrolling eligible members due to fear of legal repercussions. Employer-based insurance, which covers 56% of Americans, leaves out part-time workers and those in industries like hospitality and agriculture, where coverage is less commonly offered.

Practical Solutions and Takeaways

To reduce uninsured rates, targeted interventions are needed. Expanding Medicaid in the 10 remaining non-expansion states could cover up to 4 million uninsured individuals. Increasing awareness of ACA subsidies, which cap premiums at 8.5% of income for eligible households, could help low-income families. For young adults, educational campaigns emphasizing the value of preventive care and catastrophic coverage may shift perceptions. Policymakers should also address the coverage gap for immigrants and ensure part-time workers have access to affordable plans. By focusing on these demographics and barriers, the U.S. can move closer to universal coverage.

UFC Fighters and Health Insurance: Coverage, Costs, and Concerns

You may want to see also

Frequently asked questions

As of the latest data (2023), approximately 91% of U.S. citizens, or about 300 million people, have some form of health insurance coverage.

About 9% of U.S. citizens, or roughly 30 million people, remain uninsured, according to recent estimates.

The majority of insured U.S. citizens receive coverage through employer-sponsored plans (about 55%), followed by Medicaid (19%), Medicare (18%), and individual market plans (7%).