The COVID-19 pandemic has had a profound impact on the healthcare landscape in the United States, with one of the most pressing concerns being the significant number of Americans who have lost their health insurance. As millions of people faced job losses and reduced work hours due to the economic downturn, many also lost their employer-sponsored health coverage, which is the primary source of insurance for most Americans. Recent studies and reports indicate a sharp rise in the number of uninsured individuals, raising alarms about the potential long-term consequences on public health and the healthcare system. Understanding the scale of this issue is crucial, as it highlights the vulnerabilities within the current healthcare infrastructure and the urgent need for policy interventions to address this growing crisis.

| Characteristics | Values |

|---|---|

| Total Number of U.S. Citizens Who Lost Health Insurance (2020-2021) | Approximately 5 million (due to job losses during the COVID-19 pandemic) |

| Primary Cause of Loss | Job-based health insurance loss due to pandemic-related layoffs or furloughs |

| Age Group Most Affected | Working-age adults (25-54 years old) |

| Recovery by 2023 | Many regained coverage through employer plans, Medicaid, or ACA marketplaces |

| Current Uninsured Rate (2023) | ~8.5% of the U.S. population (approximately 28 million uninsured) |

| Key Demographics Affected | Low-income households, part-time workers, and gig economy workers |

| Impact of Medicaid Unwinding (2023) | ~15 million people at risk of losing Medicaid coverage post-pandemic |

| Source of Data | U.S. Census Bureau, Commonwealth Fund, and Kaiser Family Foundation |

Explore related products

What You'll Learn

![]()

Impact of COVID-19 layoffs on health insurance coverage

The COVID-19 pandemic triggered a wave of layoffs that left millions of Americans without employer-sponsored health insurance, the primary coverage source for most working-age adults. Estimates suggest that between March and May 2020 alone, over 12 million workers lost their jobs, and with them, their health benefits. This sudden disruption exposed the fragility of tying healthcare to employment, particularly during a public health crisis.

Example: A 35-year-old marketing professional in Ohio, laid off in April 2020, faced a stark choice: COBRA continuation coverage, costing over $600 monthly, or going uninsured while seeking a new job in a shrinking market.

The impact wasn't uniform. Younger workers, gig economy participants, and those in low-wage service industries were disproportionately affected. According to the Commonwealth Fund, individuals aged 19-34 experienced the largest percentage increase in uninsured rates, rising from 13.3% in 2019 to 16.1% in 2020. This age group often lacks the financial cushion to absorb the cost of individual plans, leaving them vulnerable to medical debt and delayed care.

Analysis: The pandemic exacerbated existing inequalities in healthcare access. Those already struggling financially were more likely to lose coverage and face barriers to obtaining alternative options like Medicaid or Affordable Care Act (ACA) marketplace plans.

While government interventions like the Families First Coronavirus Response Act provided some relief, they were temporary and didn't fully address the scale of the problem. *Takeaway:* The pandemic highlighted the need for a more robust safety net, decoupling health insurance from employment and expanding access to affordable, comprehensive coverage for all Americans.

Practical Tip: Individuals who lose employer-sponsored insurance should explore options like COBRA, ACA marketplace plans, or Medicaid. Navigating these options can be complex, so seeking assistance from healthcare navigators or enrollment specialists can be invaluable.

Medicaid Insurance Options: Understanding the Different Plan Names

You may want to see also

Explore related products

![]()

Effects of policy changes on uninsured rates

Policy shifts can dramatically alter uninsured rates, often with unintended consequences. The Affordable Care Act (ACA), for instance, reduced the uninsured rate by expanding Medicaid and creating health insurance marketplaces. From 2010 to 2016, the uninsured rate dropped from 16% to 8.6%, equating to approximately 20 million more Americans gaining coverage. However, subsequent policy changes, such as the elimination of the individual mandate penalty in 2019, led to a reversal. By 2021, an estimated 2.3 million more people were uninsured, highlighting how even small adjustments can erode progress.

Consider the impact of Medicaid expansion decisions at the state level. As of 2023, 10 states have not expanded Medicaid under the ACA, leaving millions of low-income adults ineligible for coverage. In Texas, for example, nearly 1.5 million residents fall into the "coverage gap"—earning too much to qualify for traditional Medicaid but too little to afford marketplace plans. This disparity underscores how federal policies rely on state adoption, creating geographic inequities in uninsured rates. States that expanded Medicaid saw uninsured rates drop by an average of 9.3 percentage points more than non-expansion states.

A persuasive argument emerges when examining the role of policy stability. Frequent changes in healthcare legislation create uncertainty for insurers, leading to higher premiums and reduced participation in marketplaces. For instance, the 2017 repeal of the cost-sharing reduction payments caused insurers to raise premiums by an average of 20% in 2018, pricing out many moderate-income individuals who didn’t qualify for subsidies. Stability, conversely, fosters trust and encourages enrollment. The ACA’s open enrollment periods, when consistently promoted, have consistently driven down uninsured rates among younger, healthier populations.

Comparatively, policies targeting specific demographics yield mixed results. The Children’s Health Insurance Program (CHIP) has maintained low uninsured rates among children, with only 4.3% uninsured in 2022. In contrast, policies affecting immigrant populations, such as the 2019 public charge rule, deterred eligible non-citizens from enrolling in Medicaid or CHIP, even for their U.S.-born children. This chilling effect increased uninsured rates among children by an estimated 600,000, demonstrating how policies targeting one group can spill over to others.

Practically, policymakers must balance broad reforms with targeted interventions. Expanding Medicaid in holdout states could immediately cover 4 million uninsured adults, while reinstating outreach funding for ACA enrollment could reverse recent declines. Employers can also play a role by offering more affordable plans, particularly for workers in industries like retail and hospitality, where uninsured rates remain high. Ultimately, the uninsured rate is a policy choice—one that requires deliberate, evidence-based decisions to ensure coverage for all.

Medicaid Supplemental Insurance: Understanding Your Coverage Options

You may want to see also

Explore related products

$20 $67.66

$164.06 $245.95

![]()

Trends in employer-sponsored insurance losses

The COVID-19 pandemic exposed a stark vulnerability in the US healthcare system: the reliance on employer-sponsored insurance (ESI). Between February and April 2020, an estimated 16.2 million workers lost their jobs, and with them, their health coverage. This wasn't just a temporary blip; it highlighted a long-standing trend of ESI erosion. Since the early 2000s, the percentage of Americans with ESI has steadily declined, dropping from 69% in 2000 to 56% in 2020. This trend predates the pandemic, fueled by rising healthcare costs, shifting employment landscapes, and policy changes.

Small businesses, in particular, have struggled to offer competitive benefits packages, leaving many workers vulnerable.

This decline in ESI has significant implications. For individuals, losing employer-sponsored coverage often means facing the daunting task of navigating the individual insurance market, where premiums and out-of-pocket costs can be prohibitively expensive. This can lead to delayed or forgone care, worsening health outcomes and increasing financial strain. Families are particularly hard hit, as losing coverage for one member often means losing it for all. The ripple effects extend beyond individual health, impacting productivity, economic stability, and overall societal well-being.

A 2021 Commonwealth Fund survey found that 43% of adults who lost job-based coverage during the pandemic reported difficulty affording healthcare, compared to 28% of those who retained their ESI. This disparity underscores the critical role ESI plays in ensuring access to affordable healthcare.

Several factors contribute to the ongoing erosion of ESI. Rising healthcare costs, which have outpaced inflation for decades, make it increasingly difficult for employers, especially small businesses, to absorb the expense of providing coverage. The shift towards part-time and gig work, often without benefits, further exacerbates the problem. Policy changes, such as the Affordable Care Act's individual mandate penalty repeal, may have also discouraged some employers from offering coverage.

Addressing the decline in ESI requires a multi-pronged approach. Policymakers could explore options like expanding Medicaid eligibility, creating a public health insurance option, or providing tax incentives for small businesses to offer coverage. Individuals can advocate for policies that prioritize affordable, accessible healthcare and explore alternative coverage options like health sharing ministries or short-term plans, though these often come with limitations. Ultimately, ensuring access to affordable healthcare for all Americans will require a fundamental rethinking of our current system, one that decouples health insurance from employment and prioritizes universal coverage.

Mary Lou Retton's Health Insurance Dilemma: Unraveling the Shocking Truth

You may want to see also

Explore related products

![]()

Rise in uninsured rates among low-income families

The number of uninsured Americans has been on the rise, with low-income families bearing the brunt of this trend. Recent data reveals a disturbing pattern: between 2017 and 2020, the uninsured rate among low-income adults (those earning below 200% of the federal poverty level) increased from 16.2% to 19.3%. This translates to millions of individuals and families losing access to essential healthcare services, exacerbating existing health disparities.

Factors Driving the Increase

Several factors contribute to this alarming rise. Firstly, the rollback of Medicaid expansion in some states has left many low-income individuals without coverage. Additionally, the Affordable Care Act's individual mandate repeal has reduced incentives for healthy individuals to enroll in insurance plans, leading to higher premiums and reduced affordability for those who need it most. Furthermore, the COVID-19 pandemic has resulted in widespread job losses, with many low-income workers losing employer-sponsored insurance. As a result, families are forced to choose between paying for necessities like rent and food or purchasing health insurance.

Consequences for Low-Income Families

The consequences of being uninsured are severe, particularly for low-income families. Without insurance, individuals are less likely to receive preventive care, delaying treatment until conditions become more severe and costly to treat. This can lead to poorer health outcomes, reduced productivity, and increased financial strain. For example, a study by the Commonwealth Fund found that uninsured adults are more likely to report fair or poor health status, experience medical debt, and forgo needed care due to cost. Moreover, children in low-income families without insurance are at risk of falling behind on developmental milestones, missing school due to illness, and experiencing long-term health consequences.

Addressing the Issue: Practical Solutions

To mitigate the rise in uninsured rates among low-income families, a multi-faceted approach is necessary. Policymakers should consider expanding Medicaid eligibility, increasing subsidies for marketplace plans, and implementing targeted outreach programs to educate low-income individuals about available coverage options. For instance, the American Rescue Plan Act of 2021 temporarily increased subsidies for marketplace plans, making coverage more affordable for many low-income families. Additionally, community health centers and non-profit organizations can play a crucial role in providing low-cost or free healthcare services to uninsured individuals. Families can also take proactive steps, such as exploring Medicaid eligibility, comparing marketplace plans, and utilizing health savings accounts to offset out-of-pocket costs. By combining policy solutions with individual initiatives, it is possible to reduce the number of uninsured low-income families and improve overall health outcomes.

A Call to Action

The rise in uninsured rates among low-income families is not an insurmountable challenge, but it requires immediate attention and collective effort. By understanding the underlying factors, consequences, and potential solutions, stakeholders can work together to expand access to affordable healthcare. This may involve advocating for policy changes, supporting community-based initiatives, or simply helping a neighbor navigate the complexities of the healthcare system. As the data shows, the consequences of inaction are dire – but with targeted interventions and a commitment to equity, we can reverse this trend and ensure that all families, regardless of income, have access to the care they need.

Why Insurance Companies Keep Calling You: Understanding the Persistent Calls

You may want to see also

Explore related products

$55.71 $110

![]()

State-by-state variations in health insurance losses

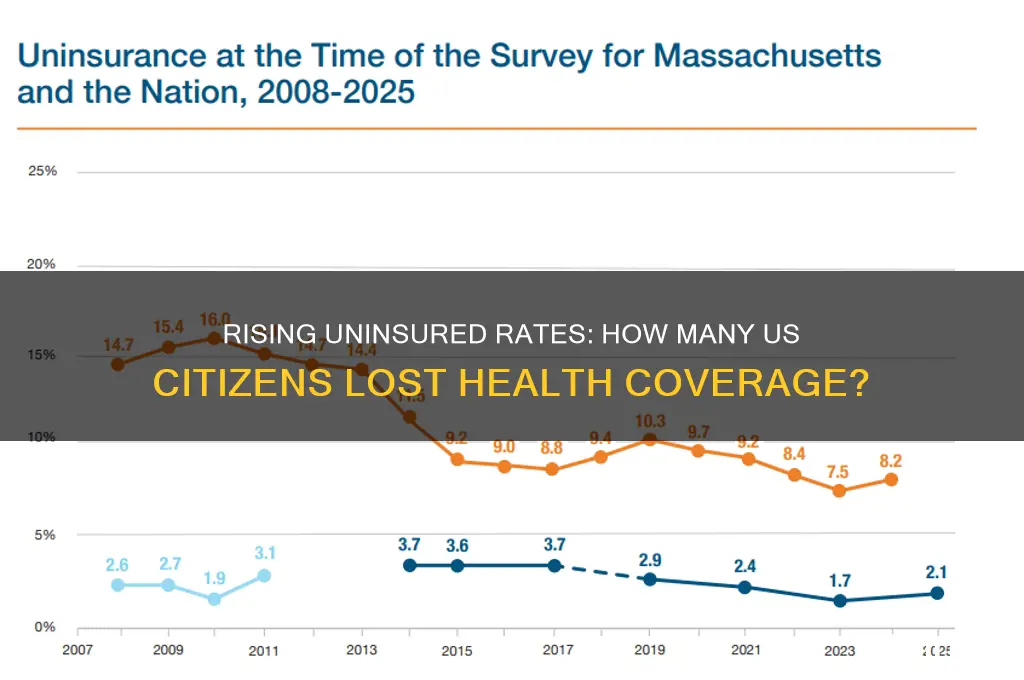

The impact of health insurance losses is not uniform across the United States, with state-by-state variations revealing stark disparities. For instance, states like Texas and Florida have consistently reported higher numbers of uninsured residents, often attributed to their large populations and policies that limit Medicaid expansion. In contrast, states such as Massachusetts and Vermont have maintained lower uninsured rates due to proactive measures like state-run health exchanges and expanded Medicaid programs. These differences highlight the critical role of state-level policies in shaping access to healthcare.

Analyzing the data further, states with higher uninsured rates often share common characteristics, such as lower median incomes and a higher proportion of gig economy workers who lack employer-sponsored insurance. For example, in Texas, approximately 18% of the population was uninsured in 2022, compared to just 3% in Massachusetts. This disparity underscores the need for targeted interventions in states with vulnerable populations. Policymakers in these regions could consider expanding Medicaid eligibility or offering subsidized health plans to bridge the coverage gap.

A comparative approach reveals that states with robust healthcare infrastructure and proactive policies fare better in mitigating insurance losses. California, for instance, has invested heavily in its state-run exchange, Covered California, which offers subsidized plans to low- and middle-income residents. As a result, the state’s uninsured rate has dropped significantly over the past decade. Conversely, states that have not expanded Medicaid under the Affordable Care Act, such as Mississippi and Alabama, continue to struggle with high uninsured rates, particularly among low-income adults.

To address these variations, states can adopt practical strategies tailored to their unique challenges. For example, states with large rural populations, like Wyoming and Montana, could focus on telemedicine initiatives to improve access to care. Additionally, public awareness campaigns about available health insurance options, such as those in New York and Colorado, have proven effective in reducing uninsured rates. By learning from successful state models, policymakers can design interventions that address the specific needs of their populations.

Finally, understanding state-by-state variations in health insurance losses is crucial for crafting effective solutions. While federal policies provide a framework, the implementation and outcomes vary widely based on state-level decisions. By examining these disparities, stakeholders can identify best practices and implement targeted measures to ensure more equitable access to healthcare across the nation. This state-specific approach is essential for reducing the overall number of uninsured Americans and improving public health outcomes.

How Company Insurance Mitigates Adverse Selection Risks Effectively

You may want to see also

Frequently asked questions

Estimates suggest that between 5 and 10 million Americans lost employer-sponsored health insurance during the COVID-19 pandemic due to job losses and economic downturns.

The percentage of uninsured Americans fluctuated over the past decade, with a notable increase during the pandemic. As of 2023, approximately 8-10% of the population remains uninsured, reflecting both gains and losses in coverage.

Yes, low-income individuals, part-time workers, and those in industries with high turnover (e.g., hospitality, retail) are disproportionately affected by health insurance loss, often due to job instability or lack of employer-sponsored coverage.