The U.S. health insurance landscape is vast and complex, with a multitude of insurers operating across the country. While exact numbers fluctuate due to mergers, acquisitions, and market exits, estimates suggest there are over 900 health insurance companies in the United States. These range from large, national carriers like UnitedHealthcare, Anthem, and Aetna, to smaller, regional providers and specialized insurers. The diversity in size and scope reflects the fragmented nature of the U.S. healthcare system, where coverage options vary significantly by state and provider network. Understanding the number and types of health insurers is crucial for consumers, policymakers, and industry stakeholders navigating this intricate market.

Explore related products

What You'll Learn

![]()

Major national health insurers in the US

The U.S. health insurance landscape is dominated by a handful of major national players, despite the existence of thousands of smaller, regional insurers. These giants—UnitedHealth Group, Anthem, Aetna, Cigna, and Humana—control a significant portion of the market, offering a wide range of plans to millions of Americans. Their size allows them to negotiate lower rates with healthcare providers, but it also raises concerns about market concentration and reduced competition. Understanding these key players is essential for anyone navigating the complexities of U.S. healthcare.

Analyzing Market Share and Influence

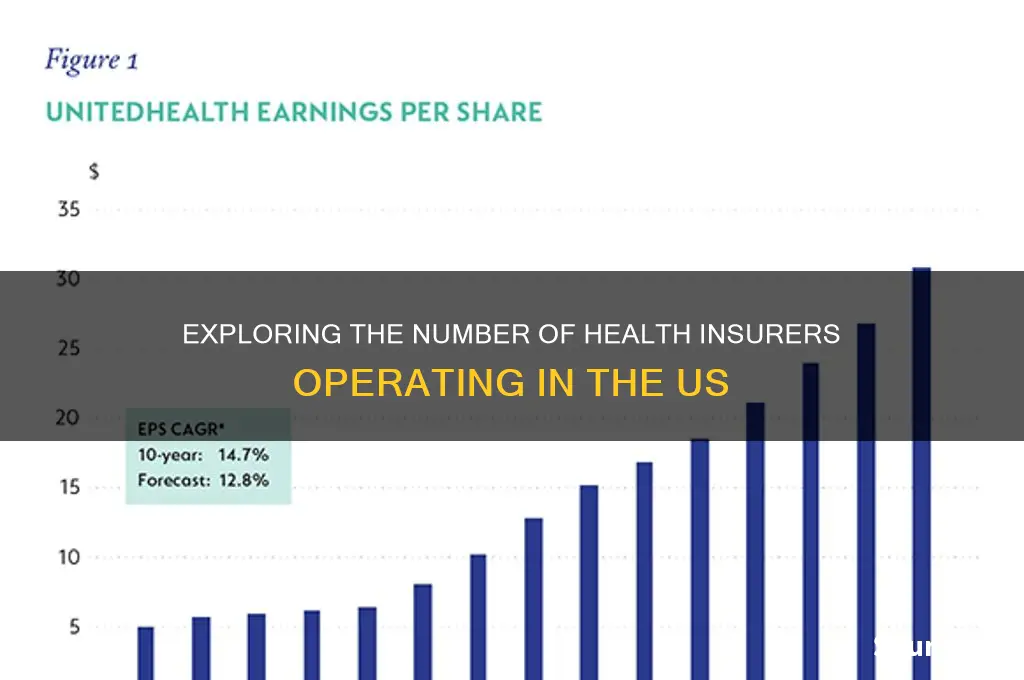

UnitedHealth Group consistently leads the pack, with over 49 million members and a market share of roughly 15%. Its diversified portfolio, including Optum (a healthcare services company), positions it as a powerhouse in both insurance and healthcare delivery. Anthem, now known as Elevance Health, follows closely with approximately 46 million members, focusing on Blue Cross Blue Shield plans across 14 states. Aetna, a CVS Health subsidiary, serves around 22 million members, leveraging its pharmacy benefits management to offer integrated care solutions. Cigna and Humana, with 17 million and 16 million members respectively, round out the top five, each specializing in distinct areas like global health services and Medicare Advantage plans.

Comparing Plan Offerings and Specializations

Each insurer tailors its offerings to specific demographics and needs. UnitedHealth Group excels in employer-sponsored plans and Medicare Advantage, while Anthem’s Blue Cross Blue Shield affiliation provides broad state-level coverage. Aetna’s integration with CVS allows it to offer unique pharmacy and health benefits, particularly for chronic conditions. Cigna stands out in international health plans and behavioral health services, whereas Humana dominates the Medicare Advantage market, catering to seniors with comprehensive wellness programs. For individuals, choosing the right insurer often depends on location, age, and specific health requirements.

Practical Tips for Selecting a National Insurer

When evaluating these major insurers, consider network size and provider access. UnitedHealth and Anthem typically offer the largest networks, but regional availability varies. For seniors, Humana’s Medicare Advantage plans often include additional benefits like dental and vision care. Aetna’s pharmacy discounts can be a game-changer for those on multiple medications. Cigna’s global coverage is ideal for frequent travelers or expatriates. Always review plan details, including deductibles, copays, and out-of-pocket maximums, to ensure alignment with your healthcare needs and budget.

The Takeaway: Navigating a Consolidated Market

While the dominance of these five insurers simplifies choice to some extent, it also underscores the importance of careful comparison. Their size ensures stability and comprehensive coverage, but it can limit flexibility and drive up costs in less competitive regions. Consumers should leverage online tools, such as Healthcare.gov or insurer comparison platforms, to assess plans side by side. Additionally, consulting a broker or using employer-provided resources can provide personalized guidance. In a market where a few players hold significant sway, informed decision-making is key to securing the best possible coverage.

Get Medication Cheaper: Tips for the Uninsured

You may want to see also

Explore related products

![]()

Regional health insurance providers by state

The United States health insurance landscape is fragmented, with over 900 health insurance companies operating across the country. However, the market is dominated by a few large national players, leaving regional providers to carve out their niches by state. These regional insurers often offer tailored plans that reflect local healthcare needs, provider networks, and cost structures. For instance, in Minnesota, HealthPartners and Blue Cross Blue Shield of Minnesota are prominent, while in Massachusetts, Harvard Pilgrim Health Care and Tufts Health Plan hold significant market share. Understanding these regional variations is crucial for consumers seeking plans that align with their local healthcare ecosystem.

Analyzing regional health insurance providers reveals distinct trends. In the Southeast, companies like Blue Cross Blue Shield of Florida and Piedmont WellStar Health Plans dominate due to their extensive provider networks and state-specific plans. Conversely, the Northeast sees a mix of nonprofit and for-profit insurers, such as ConnectiCare in Connecticut and Independent Health in New York, which often emphasize community-based care. Out West, regional insurers like Kaiser Permanente in California and Premera Blue Cross in Washington thrive by integrating health insurance with healthcare delivery systems. These regional differences highlight the importance of locality in shaping insurance options and consumer experiences.

For consumers, selecting a regional health insurance provider requires careful consideration of network coverage, plan costs, and customer service. Start by verifying that your preferred healthcare providers are in-network, as regional insurers often have narrower networks than national carriers. Compare premiums, deductibles, and out-of-pocket maximums to ensure affordability. Additionally, check customer satisfaction ratings and claims processing efficiency, as these vary widely among regional providers. For example, in Texas, Scott and White Health Plan is known for its strong provider network, while in Illinois, Health Alliance is praised for its cost-effective plans. Tailoring your choice to your state’s offerings can lead to better value and care.

A comparative approach can further illuminate the strengths of regional insurers. In states like Michigan, Priority Health stands out for its focus on preventive care and wellness programs, while in Pennsylvania, Geisinger Health Plan offers integrated care models that reduce costs for chronic conditions. Meanwhile, in the Midwest, Medica in Iowa and Nebraska’s Blue Cross Blue Shield emphasize rural healthcare access. By contrasting these providers, consumers can identify which align best with their health priorities. For instance, families might prioritize insurers with robust pediatric networks, while older adults may seek plans with comprehensive prescription drug coverage.

Finally, practical tips can streamline the process of choosing a regional health insurance provider. Use state-specific insurance marketplaces or aggregator websites to compare plans side by side. Attend local health fairs or seminars where regional insurers often provide personalized guidance. If you have specific health needs, such as maternity care or mental health services, inquire about plan benefits directly with the insurer. For example, in Arizona, Banner Health Plans offers specialized maternity programs, while in Oregon, Providence Health Plan provides extensive mental health coverage. By leveraging these resources, consumers can navigate the complexities of regional health insurance with confidence.

Mastering Health Insurance Calculations: A Step-by-Step Guide to Accurate Premiums

You may want to see also

Explore related products

![]()

Number of health insurers by market share

The U.S. health insurance market is dominated by a handful of major players, with the top five insurers controlling over 50% of the market share. UnitedHealth Group leads the pack, commanding approximately 15% of the market, followed by Anthem, Centene, Humana, and CVS Health (Aetna). This concentration raises questions about competition and consumer choice, as smaller insurers struggle to gain a foothold. Understanding market share distribution is crucial for policymakers, providers, and consumers alike, as it influences premiums, provider networks, and the overall healthcare landscape.

Analyzing market share trends reveals a steady consolidation over the past decade, driven by mergers and acquisitions. For instance, the 2020 merger between Centene and WellCare significantly bolstered Centene’s position in the Medicaid managed care sector. Meanwhile, UnitedHealth Group’s diversification into pharmacy benefit management (PBM) through Optum has solidified its dominance. Smaller regional insurers often specialize in niche markets, such as Medicare Advantage or state-specific Medicaid programs, but their combined market share remains minimal compared to the giants. This disparity highlights the challenges of competing in a market where scale and resources are paramount.

For consumers, market share concentration can translate to limited plan options and higher costs, particularly in regions where one or two insurers dominate. However, it also ensures stability and efficiency for large insurers, enabling them to negotiate better rates with healthcare providers. To navigate this landscape, individuals should compare plans based on network coverage, out-of-pocket costs, and customer satisfaction ratings. Tools like Healthcare.gov or state-based exchanges provide transparent comparisons, though they may not always reflect real-time market dynamics.

From a policy perspective, addressing market concentration requires a delicate balance. Antitrust regulations can curb excessive consolidation, but overly restrictive measures might stifle innovation and efficiency. Encouraging the growth of nonprofit insurers, such as Kaiser Permanente, could introduce more competition without sacrificing affordability. Additionally, expanding public options, like Medicare or Medicaid buy-in programs, could provide alternatives to private insurers, particularly in underserved areas. Policymakers must weigh these strategies carefully to ensure a competitive yet accessible healthcare market.

In conclusion, the number of health insurers by market share underscores a highly concentrated industry with significant implications for stakeholders. While large insurers offer economies of scale and comprehensive networks, their dominance limits consumer choice and fosters regional monopolies. By understanding these dynamics, individuals and policymakers can make informed decisions to promote a more equitable and competitive healthcare system. Practical steps include leveraging comparison tools, advocating for policy reforms, and supporting diverse insurer models to foster a balanced market.

Medicaid for All: Insurance Companies' Surprising Boon

You may want to see also

Explore related products

![]()

Trends in US health insurer consolidation

The US health insurance landscape has witnessed a significant shift towards consolidation, with the number of insurers dwindling over the years. According to a 2020 report by the American Medical Association (AMA), the five largest health insurers in the US accounted for nearly 50% of the market, up from 36% in 2014. This trend raises concerns about reduced competition, potentially leading to higher premiums and limited consumer choice.

Consider the implications of this consolidation on provider networks. As larger insurers merge or acquire smaller ones, they gain greater negotiating power with healthcare providers. This can result in narrower networks, where consumers have access to fewer doctors and hospitals. For instance, a 2019 study published in the Journal of Health Economics found that hospital prices increased by an average of 12% after a merger between two large insurers. To mitigate this risk, consumers should carefully review their plan's provider network during open enrollment, ensuring their preferred doctors and hospitals are included.

A key driver of consolidation is the pursuit of economies of scale and operational efficiencies. By merging, insurers can streamline administrative processes, reduce overhead costs, and invest in technology to improve customer experience. However, this can also lead to a one-size-fits-all approach, where personalized care and tailored benefits take a backseat. To counter this, some insurers are exploring value-based care models, which reward providers for quality outcomes rather than quantity of services. Consumers can encourage this shift by choosing plans that prioritize value-based care and by advocating for transparent quality metrics.

From a regulatory perspective, the trend towards consolidation has prompted increased scrutiny from antitrust authorities. The Department of Justice (DOJ) and Federal Trade Commission (FTC) have blocked several proposed mergers, citing concerns about reduced competition and potential harm to consumers. However, the criteria for evaluating mergers remain complex and often subjective. Consumers can play a role in shaping regulatory decisions by providing feedback on their experiences with insurers and by supporting policies that promote market competition. For example, submitting comments during the public comment period for proposed mergers can help regulators understand the potential impact on consumers.

As the consolidation trend continues, it is essential for consumers to stay informed and proactive. This includes regularly reviewing their insurance plans, comparing options during open enrollment, and advocating for policies that promote transparency and competition. By doing so, consumers can help ensure that the benefits of consolidation, such as improved operational efficiencies, are balanced with the need for accessible, high-quality care. Additionally, staying engaged with industry developments, such as proposed mergers or regulatory changes, can provide valuable insights into the evolving landscape of US health insurance.

Insurance Policy Termination: Accidents and Their Impact

You may want to see also

Explore related products

![]()

Health insurance types and provider counts

The U.S. health insurance landscape is fragmented, with over 900 health insurance companies operating nationwide. This number includes both for-profit and non-profit entities, ranging from large national carriers to smaller, regional providers. Understanding the types of health insurance and the distribution of providers is crucial for navigating this complex market.

Analytical Breakdown:

Health insurance in the U.S. falls into five primary categories: employer-sponsored plans, individual market plans, Medicare, Medicaid, and government employee plans. Employer-sponsored insurance dominates, covering approximately 157 million Americans, with providers like UnitedHealth Group, Anthem, and Aetna leading the market. The individual market, serving about 16 million people, is more diverse, with regional insurers like Blue Cross Blue Shield (BCBS) affiliates playing a significant role. Medicare and Medicaid, while government-run, often contract with private insurers for plan administration, adding another layer of provider involvement.

Instructive Guide:

To assess provider counts, start by identifying your insurance type. For employer-sponsored plans, check your company’s benefits portal for the insurer’s name. Individual market enrollees can verify their provider via Healthcare.gov or state exchanges. Medicare and Medicaid beneficiaries should review their plan documents for the administering insurer. For example, Humana and Cigna are major Medicare Advantage providers, while Molina Healthcare specializes in Medicaid managed care. Understanding your insurer is the first step in maximizing benefits and resolving claims efficiently.

Comparative Insight:

While large insurers like UnitedHealth Group and Centene Corporation dominate market share, smaller providers often offer competitive rates and localized services. For instance, BCBS affiliates operate in every state, tailoring plans to regional healthcare needs. In contrast, national carriers provide broader networks but may lack localized flexibility. When choosing a plan, compare provider counts within your area—a higher number of in-network providers can reduce out-of-pocket costs and improve access to care.

Practical Tips:

When evaluating health insurance, consider these specifics:

- Employer Plans: Ask HR for a list of in-network providers and compare it to your preferred doctors or specialists.

- Individual Market: Use Healthcare.gov’s provider directory tool to filter plans by insurer and network size.

- Medicare/Medicaid: Check the Centers for Medicare & Medicaid Services (CMS) website for a list of contracted insurers in your state.

- Regional Providers: If you have a pre-existing condition, regional insurers may offer more tailored coverage options.

By focusing on both insurance type and provider counts, you can make informed decisions that align with your healthcare needs and financial situation.

Selecting the Right Insurance Plan: A Medicaid Guide

You may want to see also

Frequently asked questions

There are over 900 health insurance companies operating in the United States, ranging from large national providers to smaller regional and local insurers.

The largest health insurers in the U.S. include UnitedHealth Group, Anthem, Aetna, Cigna, and Humana, which collectively cover a significant portion of the insured population.

No, not all U.S. health insurers are for-profit. Some are non-profit organizations, such as Blue Cross Blue Shield plans, which operate in various states.

The number varies by state and year, but typically, several dozen insurers participate in the ACA Marketplace nationwide, with some states having only one or two options.

No, coverage types vary widely among insurers. Plans can include HMOs, PPOs, EPOs, and high-deductible health plans (HDHPs), each with different benefits, networks, and costs.