Understanding how medical insurance deductibles work and how they differ from out-of-pocket expenses is crucial when selecting a health insurance plan. A deductible is the upfront cost you pay for healthcare services before your insurance plan starts contributing to the costs. It is essentially an admission fee, and your insurance will not cover any medical expenses until you have paid this amount out of your own pocket. On the other hand, out-of-pocket expenses refer to all the costs incurred for medical services that are not covered by your insurance, including copayments and coinsurance. While deductibles and out-of-pocket maximums both impact your healthcare spending, they are distinct concepts that influence your overall healthcare costs and financial protection.

| Characteristics | Values |

|---|---|

| What is a deductible? | The amount you pay for healthcare services before your health insurance plan begins paying for care. |

| What is an out-of-pocket maximum? | The most you can pay for in-network care during a year. |

| What is the difference between a deductible and an out-of-pocket maximum? | A deductible is your portion of healthcare costs before a health insurance company kicks in money for care. An out-of-pocket maximum is a limit on the amount of money you have to pay for covered health care services in a plan year. |

| How do they influence what you pay? | These two factors influence how much you pay for health insurance and how much your health plan pays for your bills. |

| What happens when you reach your deductible? | Once you reach your deductible, your insurer begins covering some costs of services. |

| What happens when you reach your out-of-pocket maximum? | Once you reach your out-of-pocket maximum, your insurance pays 100% of your medical expenses for the rest of the year. |

| What is an embedded deductible? | Some family plans have an embedded deductible, meaning there's an individual deductible for each family member, but once one person reaches their individual deductible, their expenses are covered even if the overall family deductible hasn't been met. |

| What are out-of-pocket expenses? | Out-of-pocket expenses encompass all the costs you incur for medical services that aren't covered by your insurance, including copayments and coinsurance. |

| What are copayments? | Copayments are fixed amounts you pay for certain services, like doctor visits or prescriptions. |

| What is coinsurance? | Coinsurance is when health plans pay a portion of healthcare costs after you hit your deductible. This may mean your health plan picks up 80% of the in-network costs and you handle the other 20% until you reach the plan's out-of-pocket maximum. |

| What is an example of how an out-of-pocket maximum might work? | Jane has a health plan with a $2,500 deductible, 20% coinsurance, and a $4,000 out-of-pocket maximum. She sees her regular doctor and a number of specialists, and has a lot of medical tests. She pays 20% coinsurance as her share of these medical costs, while her health plan pays the other 80%. Her bills amount to $1,500. This also counts toward the out-of-pocket maximum. At this point, Jane has spent a total of $4,000 and has met her out-of-pocket maximum. Now, her health plan will begin to pay 100% of her costs for covered care for the rest of the plan year. |

Explore related products

What You'll Learn

- Out-of-pocket expenses include copayments and coinsurance

- Deductibles are annual costs that reset each policy year

- Out-of-pocket maximums are a safety net to protect against financial ruin

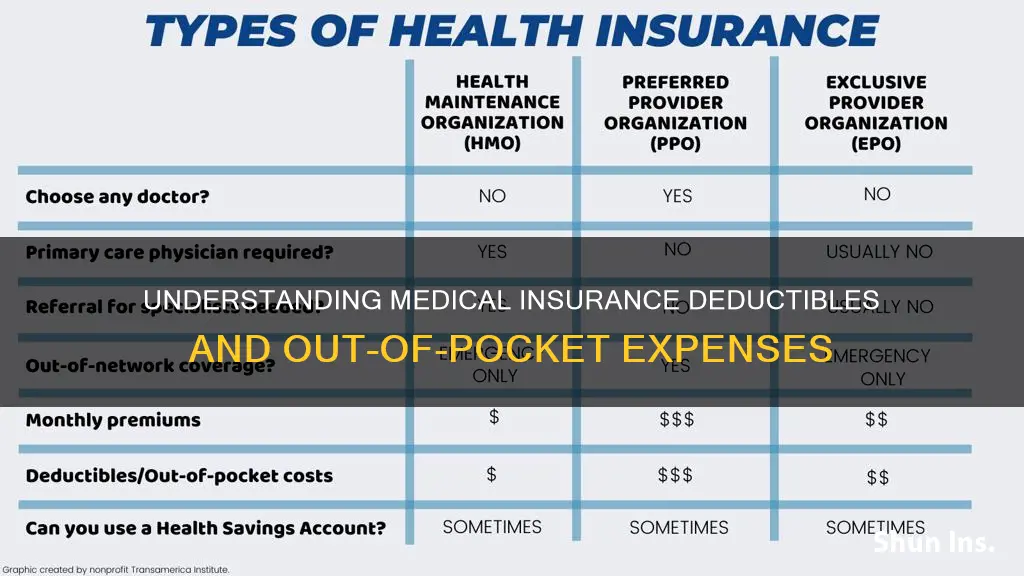

- HDHPs have lower premiums but higher deductibles than PPOs

- Out-of-pocket maximums vary depending on the type of plan

![]()

Out-of-pocket expenses include copayments and coinsurance

Out-of-pocket expenses refer to the maximum amount you could pay during a 12-month coverage period for your share of the costs of covered services. Typically, copayments, deductibles, and coinsurance all count toward your out-of-pocket maximum.

A copayment, or copay, is a fixed amount you pay for a covered health care service, usually at the time you receive the service. Copay amounts can vary depending on the provider and service. With health plans that have copays, you’ll know exactly what you have to pay ahead of time, which can help you budget your health care costs. For most plans, your copay does not apply toward your deductible.

Coinsurance refers to the percentage of costs you pay for covered services after you meet your deductible. For example, if your office visit is $100 and your coinsurance is 20%, then you would pay $20 out of pocket. Your health insurance plan would pay the remaining $80.

Your out-of-pocket maximum is the most you can pay for in-network care during a year. This is the highest amount of money you could pay during a 12-month coverage period for your share of the costs of covered services. Once you reach your out-of-pocket maximum, your insurance pays 100% of the cost for all covered services for the rest of the plan year.

Credit Card Perks: Medical Evacuation Insurance Coverage Explained

You may want to see also

Explore related products

![]()

Deductibles are annual costs that reset each policy year

A deductible is the amount of money that the insured person must pay before their insurance policy starts paying for covered expenses. In other words, it is the upfront cost you are responsible for before your insurance kicks in. It is like the admission fee to healthcare. For example, if you have a health insurance policy with a $1,000 deductible and you receive a medical bill for $2,000, you would be responsible for paying the first $1,000 and your insurance would cover the remaining $1,000.

The deductible amount varies depending on the type of insurance policy, the level of coverage, and other factors. It is important to note that deductibles only apply to covered expenses. If a particular expense is not covered by the insurance policy, it cannot be applied toward the deductible.

The timing of when a deductible resets can vary. For most health plans, the deductible resets every calendar year on January 1. However, it is important to check your health insurance plan documents to find out the specific details of when your deductible resets. This information is usually found in the plan's summary of benefits and coverage (SBC).

Medicaid Health Insurance: Eligibility and Access

You may want to see also

Explore related products

$17.99 $17.99

![]()

Out-of-pocket maximums are a safety net to protect against financial ruin

The out-of-pocket maximum is an annual limit that includes deductibles, copayments, and coinsurance. A deductible refers to the upfront cost or admission fee that must be paid before your insurance plan begins to cover any costs. Once you have met your deductible, you are still responsible for paying copayments (fixed amounts for specific services) and coinsurance (a percentage of the total cost) until you reach your out-of-pocket maximum. It is important to note that the out-of-pocket maximum does not include insurance premiums, costs for non-covered services, or out-of-network services.

The amount of the out-of-pocket maximum varies depending on the type of plan chosen. Group insurance plans obtained through an employer typically have a lower out-of-pocket maximum than individual plans. Additionally, opting for a high deductible health plan (HDHP) can help save money if you are generally in good health, as these plans tend to have lower monthly premiums. However, it is crucial to carefully consider your own health needs when selecting a plan, as higher deductibles can result in higher out-of-pocket expenses before reaching the maximum.

Understanding the difference between deductibles and out-of-pocket maximums is essential when choosing a health insurance plan. While a plan with a lower deductible may seem appealing, it often comes with higher monthly premiums. On the other hand, a plan with a higher deductible usually has lower monthly premiums but may result in higher out-of-pocket expenses before reaching the maximum. Therefore, it is important to compare not just monthly premiums but also deductibles and out-of-pocket costs when selecting a health plan.

LASIK Surgery: Can Medical Insurance Cover the Cost?

You may want to see also

Explore related products

![]()

HDHPs have lower premiums but higher deductibles than PPOs

A health insurance deductible is the amount you pay for healthcare services before your health plan kicks in and starts paying for your care. The out-of-pocket maximum is the most you can pay for in-network care during a year. These two factors influence how much you pay for health insurance and how much your health plan pays for your bills.

High-deductible health plans (HDHPs) are a type of health insurance plan that generally has higher deductibles and out-of-pocket maximums than traditional health insurance plans like Preferred Provider Organizations (PPOs). This means that with an HDHP, you will pay less every month for your plan (lower premiums), but you will have to pay more out of your own pocket before your insurance coverage kicks in.

On the other hand, a traditional PPO typically has a lower deductible and lower out-of-pocket maximum than an HDHP. This means that with a PPO, you will pay a higher monthly premium, but you will have to pay less out of your own pocket before your insurance coverage starts paying for your care.

It's important to note that the choice between an HDHP and a PPO depends on your individual needs and circumstances. An HDHP may be suitable if you are generally healthy and don't anticipate needing frequent medical care. However, if you have ongoing medical conditions or expect to incur higher medical expenses, a PPO with its lower deductible and out-of-pocket maximum may be a better option, despite the higher monthly premiums.

Additionally, HDHPs often provide access to health savings accounts (HSAs), which can be used for expenses towards deductibles, prescriptions, and other medical expenses. Contributions to an HSA can reduce your taxable income and provide tax-free withdrawals for eligible medical expenses.

Medicaid as Secondary Insurance: Texas-Specific Options

You may want to see also

Explore related products

$14.99 $19.99

![]()

Out-of-pocket maximums vary depending on the type of plan

Out-of-pocket maximums and deductibles vary depending on the type of plan chosen. Group insurance plans obtained through an employer will often have a lower out-of-pocket maximum than an individual plan. The same applies for deductibles. Opting for a high-deductible health plan (HDHP) versus a traditional preferred provider organisation (PPO) can help save money if you're in good health, as it could mean fewer unexpected visits to the doctor. That's because HDHPs tend to have lower monthly premiums, so you'll likely be spending less money upfront.

Lower-income individuals and families may qualify for reduced out-of-pocket maximums through cost-sharing reduction discounts. To be eligible, you must meet income requirements and enrol in a Health Insurance Marketplace plan in the Silver category. Cost-sharing reductions offer a range of benefits, including lower deductibles, copayments or coinsurance, and a lower out-of-pocket maximum.

The out-of-pocket maximum for marketplace plans can't be above a set amount each year. For example, for the 2022 plan year, this amount was $8,700 for an individual and $17,400 for a family. The out-of-pocket maximum is the most a health insurance policyholder will pay each year for covered healthcare expenses. When this limit is reached, the health plan will cover 100% of the qualified expenses for the rest of the plan year.

There are a number of expenses that may not count toward the out-of-pocket maximum. These include care and services that aren't covered by the health plan, such as cosmetic treatments, weight loss surgery, and some alternative medicine. Costs above the allowed amount may also not be covered, as most plans set a maximum amount they will pay for various services. Out-of-network care and services may not be covered either, as most health plans have a network of doctors who provide discounted rates for plan customers.

Navigating Healthcare Without Medical Insurance: Challenges and Strategies

You may want to see also

Frequently asked questions

A deductible is the upfront cost you pay for healthcare services before your insurance plan begins to pay for your care.

An out-of-pocket maximum is the most you can pay for in-network care during a year. After you reach this amount, your insurance company will pay 100% of your medical expenses for the rest of the year.

Your out-of-pocket maximum includes your deductible, copayments, and coinsurance. Once you have spent a total of this amount on covered health services, you will have reached your out-of-pocket maximum.

A deductible is the amount you pay before your insurance company starts contributing to your healthcare costs. An out-of-pocket maximum is the maximum amount you will pay for healthcare in a year, after which your insurance company will pay for all covered services.

When selecting a health insurance plan, it is important to assess your health and potential medical needs. A plan with a lower deductible often has higher monthly premiums, so you pay more upfront but less when you need medical care. A high-deductible plan usually has lower monthly premiums, so you pay less upfront but more when you need medical care.