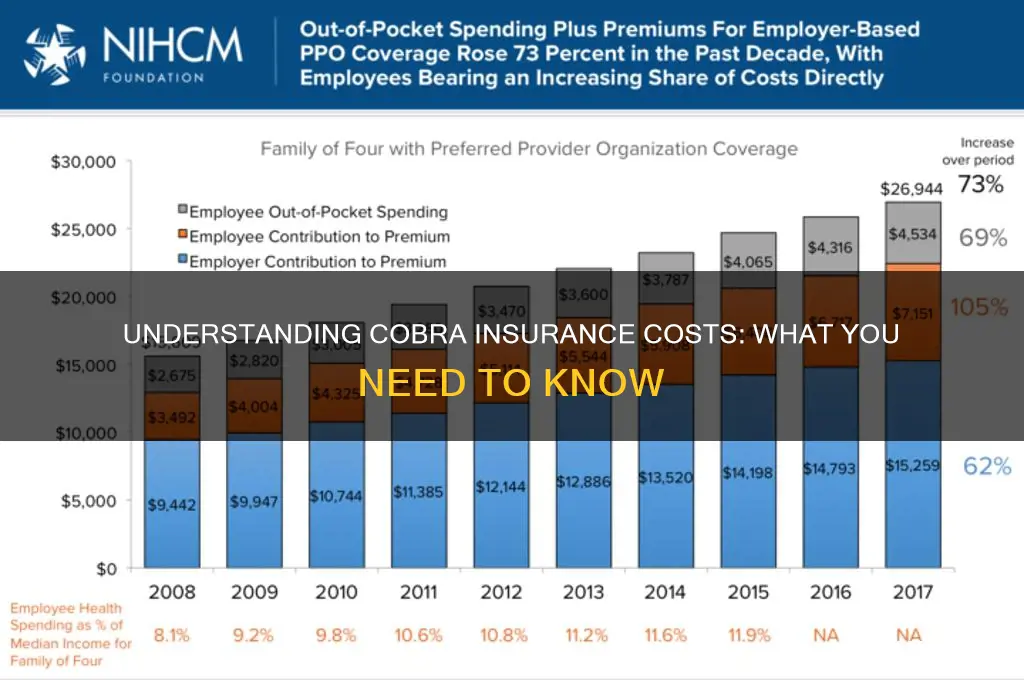

COBRA insurance, which allows individuals to continue their employer-sponsored health coverage after leaving a job, often comes with a significant cost. The price of COBRA insurance typically includes the full premium of the health plan, plus an additional 2% administrative fee, totaling up to 102% of the plan’s cost. For many, this can translate to hundreds or even thousands of dollars per month, depending on the type of coverage and the number of dependents. Understanding these costs is crucial for anyone considering COBRA, as it helps in weighing the benefits against alternative options like private insurance or marketplace plans.

| Characteristics | Values |

|---|---|

| Average Monthly COBRA Premium (2023) | $700 - $1,000 (individual), $2,000 - $2,500 (family) |

| Cost Structure | Typically 102% of the plan's premium (includes 2% administration fee) |

| Duration of Coverage | Up to 18 months (may extend to 36 months in certain cases) |

| Eligibility | Employees and their dependents who lose group health coverage due to qualifying events (e.g., job loss, reduced hours) |

| Employer Contribution | None (employee pays full premium + administrative fee) |

| Plan Types Covered | Medical, dental, vision, and other group health plans |

| Tax Implications | Premiums are not tax-deductible unless itemizing deductions and meeting certain criteria |

| Alternative Options | ACA Marketplace plans, spouse's employer plan, short-term health insurance, Medicaid |

| Enrollment Period | 60 days from the qualifying event or loss of coverage |

| State-Specific Variations | Some states (e.g., California, New York) offer mini-COBRA with extended coverage or lower costs |

| Pre-Existing Conditions | Covered if previously enrolled in the employer's plan |

| Portability | Coverage is tied to the previous employer's plan, not portable to new employers |

Explore related products

![Cobra - Collector's Edition [Blu-ray]](https://m.media-amazon.com/images/I/81mc0ZQlTvL._AC_UY218_.jpg)

What You'll Learn

![]()

Cobra Insurance Costs by State

COBRA insurance costs vary significantly by state, influenced by factors like local healthcare expenses, state regulations, and the specific employer-sponsored plan. For instance, in high-cost states like California or New York, monthly premiums can exceed $700 for individual coverage and $2,000 for family plans. In contrast, states with lower healthcare costs, such as Mississippi or Alabama, may see premiums around $400 for individuals and $1,200 for families. These disparities highlight the importance of understanding your state’s healthcare landscape when budgeting for COBRA.

To estimate your COBRA costs, start by reviewing your employer’s plan details, as premiums are typically 102% of the plan’s total cost (including the employer’s share). For example, if your employer previously covered 70% of a $1,000 monthly premium, your COBRA cost would be $1,020. However, state-specific factors like insurance mandates or provider networks can further adjust these figures. Use online COBRA calculators or consult your state’s insurance department for precise estimates tailored to your location.

A comparative analysis reveals that states with robust healthcare infrastructure often have higher COBRA premiums due to increased provider fees and service utilization. For instance, Massachusetts, known for its comprehensive healthcare system, reports average COBRA costs of $800 for individuals, while Texas, with a more fragmented system, averages $550. This underscores the trade-off between access to care and insurance affordability. If you’re relocating or considering COBRA across state lines, research these differences to avoid unexpected financial strain.

Practical tips for managing COBRA costs include exploring state-specific subsidies or alternative coverage options. Some states, like New Jersey, offer temporary premium assistance programs for eligible individuals. Additionally, compare COBRA to marketplace plans or spouse/parent coverage, as these may provide similar benefits at a lower cost. For example, a 27-year-old in Colorado might save $200 monthly by switching from COBRA to a marketplace plan with comparable coverage. Always weigh the pros and cons before making a decision.

Finally, be mindful of COBRA’s time-limited nature (typically 18 months) and plan accordingly. States like California extend COBRA-like coverage for up to 36 months under certain conditions, but federal rules generally apply elsewhere. To avoid gaps in coverage, mark your COBRA expiration date and start researching alternatives three months prior. This proactive approach ensures continuity of care while optimizing costs based on your state’s unique insurance environment.

Cashing in on Liberty National Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Factors Affecting Cobra Insurance Premiums

COBRA insurance premiums are not one-size-fits-all; they vary widely based on several key factors. Understanding these can help you anticipate costs and make informed decisions. One of the most significant determinants is the type of health plan you’re continuing. For instance, a family plan will almost always cost more than an individual plan, often two to three times the individual rate. If your previous employer’s plan included dental or vision coverage, opting to continue those benefits under COBRA will further increase your premium.

The size of your employer also plays a critical role. Under federal COBRA, companies with 20 or more employees are subject to the law, but state-specific "mini-COBRA" laws may apply to smaller businesses. Premiums for COBRA coverage can be up to 102% of the plan’s total cost, including the portion previously paid by your employer plus a 2% administrative fee. For example, if your employer paid $1,000 monthly for your family plan and you paid $300, your COBRA premium could jump to $1,020, reflecting the full cost plus the fee.

Geographic location is another often-overlooked factor. Health care costs vary dramatically by state and region, influencing COBRA premiums. For instance, a family plan in California might cost $1,800 per month under COBRA, while a similar plan in Texas could be closer to $1,500. Additionally, the specific benefits and provider networks of the plan can affect costs. Plans with broader networks or more comprehensive coverage will generally result in higher premiums.

Finally, the duration of your COBRA coverage matters. While federal COBRA allows for up to 18 months of coverage (with extensions in certain cases), the longer you remain on the plan, the more you’ll pay in total. For example, 18 months of a $1,020 monthly premium totals $18,360. If you’re eligible for a subsidy or have access to a more affordable alternative, such as a spouse’s employer plan or a marketplace plan, transitioning sooner could save you thousands. Always compare COBRA costs with other options to ensure you’re making the most cost-effective choice.

Does AAA Offer Trip Insurance? Exploring Coverage Options for Travelers

You may want to see also

Explore related products

![Stallone 5-Movie Collection (Assassins, The Specialist, Tango and Cash, Demolition Man, Cobra) [Blu-ray] [Region Free]](https://m.media-amazon.com/images/I/81LlS1rZyFL._AC_UY218_.jpg)

![]()

Cobra vs. Private Health Insurance

COBRA insurance, an extension of employer-sponsored coverage, allows individuals to retain their existing plans after job loss, but at a steep cost—typically 102% of the full premium, including what the employer previously subsidized. This price tag often exceeds $700 monthly for individual plans and can surpass $2,000 for families, making it a financial burden for many. In contrast, private health insurance offers a broader range of options, with premiums averaging $456 monthly for individuals and $1,138 for families, according to 2023 data. However, the trade-off lies in plan specifics: COBRA ensures continuity with known networks and coverage, while private plans may require adjusting to new providers and benefits.

For those weighing COBRA vs. private insurance, the decision hinges on timing and eligibility. COBRA is only available for 18 to 36 months, depending on the circumstances of job loss, and requires enrollment within 60 days of losing coverage. Private insurance, however, can be purchased year-round during open enrollment or with a qualifying event, such as job loss, which triggers a special enrollment period. Subsidies through the Affordable Care Act (ACA) marketplace can significantly reduce private plan costs for individuals earning up to 400% of the federal poverty level—approximately $54,000 for a single person or $111,000 for a family of four in 2023.

A critical factor in this comparison is pre-existing conditions. COBRA guarantees coverage without exclusions, making it ideal for those with ongoing medical needs. Private plans, while prohibited from denying coverage due to pre-existing conditions under the ACA, may have different formularies or provider networks, potentially disrupting care. For example, a COBRA plan might include a specific specialist or medication already in use, whereas a private plan could require switching providers or paying higher out-of-pocket costs for the same treatment.

Practically, individuals should assess their health needs, budget, and future plans. If expecting employment with benefits soon, COBRA provides seamless coverage. For those facing long-term unemployment or seeking affordability, private insurance—especially with subsidies—may be more sustainable. Tools like Healthcare.gov’s plan comparison feature can help evaluate premiums, deductibles, and network adequacy. Additionally, consulting a broker or using online calculators can clarify cost differences based on income and location.

Ultimately, the choice between COBRA and private insurance requires balancing immediate needs with long-term financial stability. While COBRA offers familiarity and continuity, its cost often outweighs its benefits for those eligible for subsidized private plans. Conversely, private insurance demands research to ensure adequate coverage but can provide significant savings and flexibility. Careful consideration of these factors ensures a decision aligned with both health and financial well-being.

Borrowing Against Life Insurance: What Australians Need to Know

You may want to see also

![]()

Cobra Coverage Duration Limits

COBRA insurance, while a lifeline for many, comes with a ticking clock. The Consolidated Omnibus Budget Reconciliation Act (COBRA) mandates that employers offer continuation of group health coverage for a limited time after certain qualifying events, such as job loss or reduced hours. Understanding these duration limits is crucial for planning your healthcare needs during transitions.

The standard COBRA coverage period is 18 months, but this can vary based on the qualifying event and other factors. For instance, if you experience a job loss due to gross misconduct, you may not be eligible for COBRA at all. In cases of divorce or legal separation, the covered spouse and dependents can continue coverage for up to 36 months. Disability extends the coverage period to 29 months if properly notified within 60 days of the disability determination. Knowing these exceptions can help you maximize your coverage window.

Let’s break it down further: if you’re a healthy individual with no pre-existing conditions, 18 months might be sufficient to find new employment with benefits. However, if you or a dependent has ongoing medical needs, the 36-month extension in cases of divorce or disability becomes invaluable. For example, a family with a child undergoing long-term treatment could benefit significantly from the extended coverage.

Practical tip: Mark your calendar with key dates, such as the start of COBRA coverage and the deadline to enroll. Missing these dates can result in loss of coverage. Additionally, consider comparing COBRA costs to marketplace plans or spouse/partner insurance, as COBRA can be expensive due to the employee’s share and administrative fees.

In conclusion, COBRA’s duration limits are not one-size-fits-all. By understanding the nuances of these limits and planning accordingly, you can ensure continuous healthcare coverage during life’s transitions. Always review your specific qualifying event and consult with your employer or a benefits specialist to avoid gaps in protection.

Playground Insurance in TN: Is It Required for Your Business?

You may want to see also

![]()

Eligibility Requirements for Cobra Insurance

COBRA insurance, an acronym for the Consolidated Omnibus Budget Reconciliation Act, is a federal law that allows certain individuals to continue their employer-sponsored health insurance coverage after they leave their job. However, not everyone is eligible for this continuation coverage. Understanding the eligibility requirements is crucial for those who wish to maintain their health insurance during a transition period.

Qualifying Events and Coverage Duration

To be eligible for COBRA, you must experience a "qualifying event" that results in the loss of your group health insurance. Common qualifying events include job termination (voluntary or involuntary), reduction in work hours, divorce, or the death of the covered employee. Notably, quitting a job without a reduction in hours does not qualify. Once eligible, COBRA coverage typically lasts for 18 months, though certain circumstances, such as a disability or a second qualifying event, can extend this period to 29 or 36 months. For instance, if you become disabled within the first 60 days of COBRA coverage, you may qualify for an 11-month extension.

Who Is Covered Under COBRA?

COBRA eligibility extends beyond the employee to include their spouse and dependent children who were covered under the employer’s group health plan at the time of the qualifying event. For example, if a spouse loses their job and had family coverage, both the spouse and the children can continue their insurance through COBRA. However, dependents may lose coverage if they reach a disqualifying age (e.g., turning 26) or get married, depending on the plan’s terms.

Employer Size and Plan Requirements

Not all employers are required to offer COBRA. The law applies only to employers with 20 or more employees. Smaller businesses may be exempt, though some states have "mini-COBRA" laws that provide similar benefits. Additionally, COBRA applies only to group health plans, which typically include medical, dental, vision, and prescription drug coverage. Other benefits, like life insurance or health flexible spending accounts (FSAs), may also be continued under COBRA, but this varies by plan.

Practical Tips for Navigating Eligibility

If you believe you qualify for COBRA, act promptly. Employers have 30 to 45 days to notify you of your COBRA rights after a qualifying event, and you have 60 days to elect coverage. Missing these deadlines can result in losing eligibility. Keep detailed records of your employment status, qualifying event, and communications with your employer or insurer. If you’re unsure about your eligibility, consult your employer’s HR department or a benefits specialist. Remember, COBRA is not automatic—you must actively elect and pay for the coverage, often at a higher cost than your previous employer-subsidized rate.

Comparing COBRA to Alternatives

While COBRA ensures continuity of coverage, it’s often expensive since you’re responsible for the full premium plus an administrative fee. Alternatives like purchasing insurance through the Health Insurance Marketplace, Medicaid, or a spouse’s employer plan may be more cost-effective. For example, if you lose your job and qualify for a special enrollment period on Healthcare.gov, you might find a plan with lower premiums or subsidies. Weighing COBRA against these options requires careful consideration of your health needs, budget, and the level of coverage you’re willing to maintain.

Steps to Cancel Lemonade Insurance: A Comprehensive Guide to Ending Coverage

You may want to see also

Frequently asked questions

COBRA insurance typically costs the full premium of the employer-sponsored plan, plus an administrative fee of up to 2%. On average, this can range from $400 to $700 per month for individual coverage and $1,200 to $2,000 for family coverage.

No, COBRA insurance costs are not determined by state. The cost is based on the employer’s group health plan premium and the 2% administrative fee, which applies uniformly across states.

COBRA itself does not offer discounts, but individuals may qualify for subsidies through the American Rescue Plan Act (ARPA) or other programs. Check with your state’s health insurance marketplace for potential assistance.

COBRA is expensive because it requires individuals to pay the full premium of the employer-sponsored plan, including the portion previously covered by the employer, plus the administrative fee. Other plans may be subsidized or have lower premiums.