Homeowner's insurance is often bundled with mortgage payments through an escrow account, which is a savings account managed by the lender. This arrangement is required by most mortgage lenders and makes managing housing expenses easier. The escrow account is used to pay annual or biannual expenses like property taxes and insurance on the homeowner's behalf. While not all homeowners need mortgage insurance, homeowner's insurance is usually a necessity to ensure the home is sufficiently protected. The cost of homeowner's insurance is determined by factors such as the home's value, location, and construction type, and it can vary each year depending on changes in insurance rates and property tax. As insurance rates continue to climb due to factors like climate change and rising property values, the monthly mortgage payment will also rise to account for the increased cost.

| Characteristics | Values |

|---|---|

| What is homeowners insurance? | Coverage against specific damages and incidents affecting your home. |

| What is mortgage insurance? | Protects the lender if you default on the loan. |

| Who requires mortgage insurance? | Lenders may require it to protect their interests if you default on your loan. |

| Who requires homeowners insurance? | All mortgage lenders require it for all borrowers. |

| How much does homeowners insurance cost? | The national average for home insurance is $2,377 a year, but this varies by state. |

| What factors influence the cost of homeowners insurance? | Home value, location, construction type, past claims, neighbourhood, and the condition of the house. |

| How is homeowners insurance paid? | Homeowners insurance can be paid through an escrow account or directly to the insurance company |

| What is an escrow account? | A savings account managed by the lender to pay for expenses like property taxes and insurance. |

| What are the benefits of using an escrow account? | Combining bills into one monthly payment can make managing housing expenses easier. |

| Can I opt-out of using an escrow account? | Yes, you can choose to pay your homeowners insurance directly, typically on a monthly, quarterly, semi-annual, or yearly basis. |

Explore related products

$15.95 $15.95

What You'll Learn

![]()

Escrow accounts

An escrow account is a savings account managed by a mortgage servicer or lender. It is used to pay annual or biannual expenses like property taxes, insurance, and other expenses like flood insurance and private mortgage insurance (PMI) on your behalf. This arrangement can make managing housing expenses easier. With an escrow account, expenses for principal, interest, taxes, and insurance are combined into one monthly payment. The lender or loan servicer prorates these expenses and adds them to your mortgage payment. By having your property taxes and home insurance disbursements done through escrow, you can ensure your premiums are paid and that your lender's investment is protected.

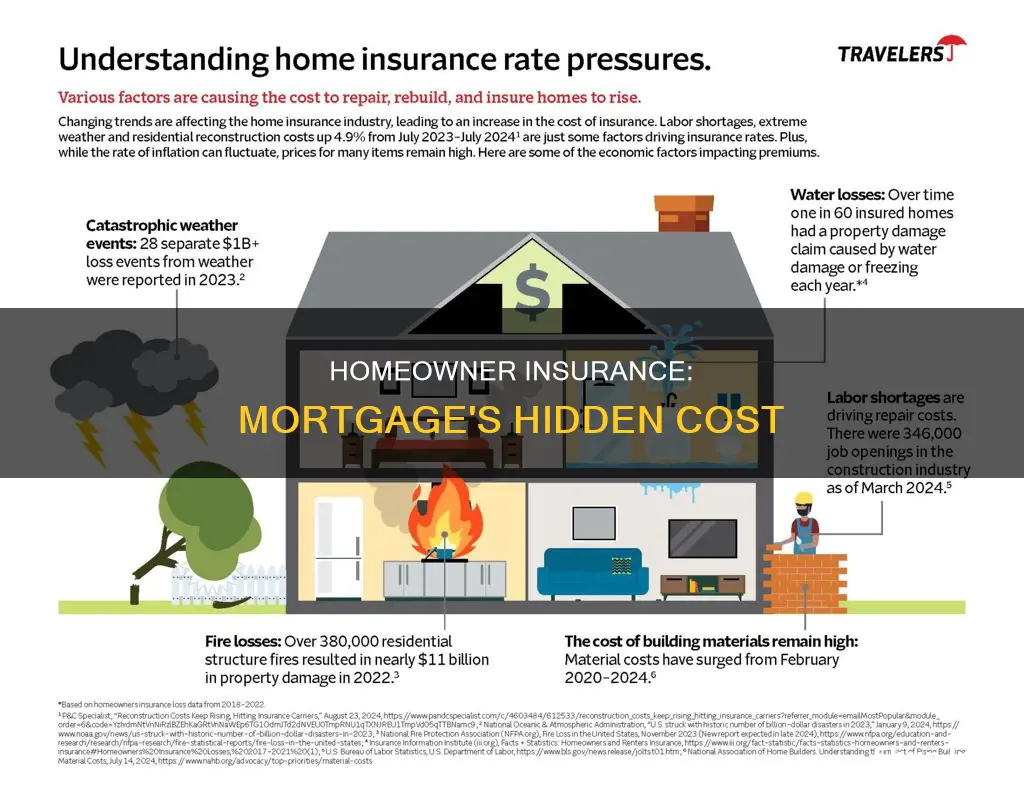

Escrow payments can go up or down each year, depending on changes in insurance and property tax. If home insurance rates increase, your monthly mortgage payment will rise to account for the cost. This is exactly what’s happening to homeowners around the US as insurance premiums continue to climb due to factors like climate change, rising property values, and increased litigation.

When you close on your home, your lender may set up an escrow account for depositing part of your monthly loan payment to cover your real estate taxes, homeowners insurance premium, and, if necessary, private mortgage insurance. Your mortgage lender deposits a designated amount from your mortgage payment into the escrow account each month and then directly pays your homeowners insurer. Escrow accounts can vary depending on your lender, type of property, and location. If you're concerned about the process or have specific questions about your escrow account, contact your lender or a qualified mortgage professional.

Homeowners Insurance: Necessary Protection or Waste of Money?

You may want to see also

Explore related products

![]()

Private mortgage insurance (PMI)

PMI can be paid in a few different ways. Sometimes, it's paid as a one-time upfront premium at closing, which is shown on your Loan Estimate and Closing Disclosure. Other times, it's paid with both upfront and monthly premiums. The monthly premium is also shown on your Loan Estimate and Closing Disclosure. Lenders may offer multiple PMI options, so it's worth asking the loan officer to help you calculate the total costs over different timeframes.

PMI is not a permanent fixture. You can request to cancel it when your mortgage balance reaches 80% of your home's value. Federal law also dictates that your mortgage lender must automatically end PMI when the LTV ratio drops to 78% or when you are one month past the midpoint of your loan term.

PMI should not be confused with homeowners insurance. While PMI protects the lender in case the borrower defaults on their loan, homeowners insurance, also called home insurance, protects the homeowner against specific damages and incidents affecting their home. It also provides liability coverage in case a guest or visitor gets injured on the property. Home insurance is usually paid through an escrow account, which is set up by the mortgage lender to collect and manage funds for property taxes and insurance. Escrow payments can vary from year to year, depending on changes in insurance rates and property tax.

Finding Homeowners Insurance: Who Covers Your Property?

You may want to see also

Explore related products

![]()

Homeowner's insurance rates

Homeowners insurance rates vary depending on a variety of factors, and they can add hundreds of dollars to your monthly budget. The average cost of homeowners insurance for a 12-month policy from Progressive's network of insurers ranges from $1,090.08 ($90.84/month) to $3,353.74 ($279.48/month) for policies effective on or after January 1, 2024. According to Insurify, the national average for home insurance is $2,377 per year. However, rates can vary significantly by city, state, and region.

The main factor influencing homeowners insurance rates is the amount of dwelling coverage, also known as Coverage A. Larger homes are typically more expensive to insure than smaller homes. Additionally, the location of the property plays a significant role in determining rates. Homes in coastal regions or areas prone to extreme weather, flooding, wildfires, or high crime rates may be riskier to insure and, therefore, more costly.

Other factors that can impact homeowners insurance rates include the construction materials used, coverage selections, prior claims history, and the presence of additional hazards on the property, such as a swimming pool or a trampoline.

Homeowners insurance is typically required by mortgage lenders, and it can be included in your mortgage payments through an escrow account. This account is managed by the mortgage servicer and used to pay expenses like property taxes and insurance on your behalf. If home insurance rates increase, your monthly mortgage payment will also rise accordingly.

Lloyd's of London: Does Your Home Insurance Cover Lava?

You may want to see also

Explore related products

$4.99 $14.99

![]()

Lender requirements

The amount of homeowners insurance required by lenders is typically based on the replacement cost of the home. Lenders want to ensure that the home can be completely rebuilt in the event of a total loss. They may also require that you have enough insurance to cover the amount of your loan. For example, if you purchased a $300,000 home with a $60,000 down payment, your lender may require you to have at least $240,000 worth of dwelling coverage.

In addition to dwelling coverage, lenders may also stipulate that you have hazard insurance, which covers damages to the home and other structures. They may also require additional coverage, such as flood insurance or earthquake insurance, depending on the location of the property and the risk of natural disasters.

Homeowners insurance payments are often included in your mortgage payments through an escrow account. This account is set up by the lender to collect and manage funds for property taxes and insurance premiums, ensuring that these payments are made on time. The lender collects a portion of these expenses along with your monthly mortgage payment and then pays them on your behalf.

It is important to note that lender requirements for homeowners insurance may vary, and you should consult your loan agreement or lender directly to understand their specific requirements.

Erie Homeowners Insurance: Does It Cover Renters, Too?

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)

![]()

Additional insurance

Depending on where you live, you may need to purchase additional insurance policies to protect your home. For example, if you live in an area prone to flooding, you may need to purchase flood insurance. Similarly, if you live in an area susceptible to hurricanes or earthquakes, you may want to consider hurricane or earthquake insurance, respectively. These additional policies can provide financial protection in the event of damage or loss caused by these specific events.

It is worth noting that even if you have paid off your mortgage, maintaining home insurance is still highly recommended. Your home is likely one of your most significant financial assets, and without insurance, you would be responsible for covering the full cost of any damage or loss. By continuing to invest in home insurance, you can offset these potential costs and protect your financial stability.

Home insurance policies typically include coverage for specific damages and incidents that may affect your home. However, it is important to carefully review your policy to understand any exclusions or limitations. For example, some policies may not cover damage caused by natural disasters, such as floods or earthquakes, which would require additional insurance as mentioned earlier.

Additionally, consider including Additional Living Expenses (ALE) coverage in your home insurance policy. This type of coverage can assist with lodging and meal expenses if your home becomes uninhabitable due to a covered event. For instance, if your home is undergoing repairs or reconstruction after a covered incident, ALE coverage can help pay for temporary accommodation and meals during that period.

Furthermore, liability coverage is an important aspect of home insurance that should not be overlooked. This type of coverage protects you from liability claims if someone is injured on your property. It can help cover medical bills and, in some cases, even your attorney fees if a liability claim is made against you. By including liability coverage in your home insurance policy, you can gain peace of mind knowing that you are protected financially in the event of an accident or injury involving a guest or visitor on your property.

Home Insurance: Cellphone Coverage and Travelers

You may want to see also

Frequently asked questions

It depends on the type of mortgage and the lender. Many homeowners pay for their homeowners insurance as part of their mortgage payment through an escrow account. However, some lenders may give you the option to pay your insurance provider directly.

An escrow account is a type of savings account managed by your lender. It is used to pay annual or biannual expenses like property taxes and insurance on your behalf. This arrangement can make managing housing expenses easier as it combines principal, interest, taxes and insurance into one monthly payment.

The cost of homeowners insurance is generally determined by factors such as the home's value, location and construction type. The national average for home insurance in the US is $2,377 per year, but prices vary by state.

Homeowners insurance, also known as home insurance, is coverage that is required by all mortgage lenders for all borrowers. It provides coverage against specific damages and incidents affecting your home. Mortgage insurance, on the other hand, protects the lender if you default on your loan. Not every homeowner needs mortgage insurance.