The cost of gender-affirming surgery, previously known as sex reassignment surgery, can vary depending on the procedure and the insurance coverage of the patient. While some insurance companies recognise these procedures as medically necessary, others consider them cosmetic and therefore not covered. The cost of surgery can range from $6,900 to $63,400, with out-of-pocket expenses varying depending on insurance coverage.

How much for a sex change with medical insurance?

| Characteristics | Values |

|---|---|

| Number of Americans undergoing sex reassignment surgery annually | 3,000–9,000 |

| Total costs of transgender-specific care for one person | $25,000–$75,000 |

| Cost of gender-affirming surgery | $6,900–$63,400 |

| Cost of treating depression, substance abuse and HIV/AIDS | Comparable to the cost of surgery and hormones |

| Number of transgender people in the US | 1.4 million |

| Number of transgender people with Medicaid coverage | 276,000 |

| States that have banned gender-affirming surgery for people under 18 | Alabama, Arkansas, Florida, Georgia, Idaho, Indiana, Iowa, Kentucky, Louisiana, Mississippi, Missouri, Montana, Nebraska, North Carolina, North Dakota, Oklahoma, South Dakota, Tennessee, Texas, Utah, West Virginia |

| States with laws or executive orders protecting access to gender-affirming surgery | Alabama, Arkansas, Florida, Indiana |

Explore related products

What You'll Learn

![]()

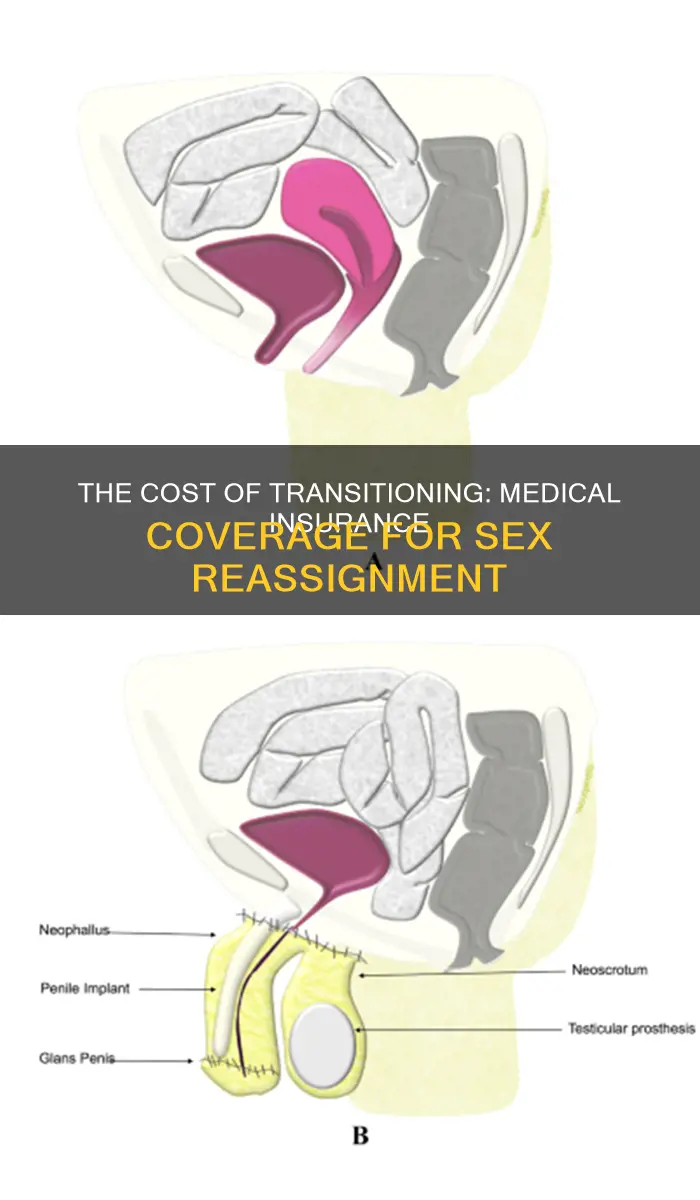

Gender-affirming surgery

The cost of gender-affirming surgery varies depending on the specific procedures performed and the individual's health insurance plan. On average, vaginoplasty costs $6,000 with insurance coverage, but the price can range from $6,000 to $50,000 without insurance. The total costs of transgender-specific care for one person are often estimated to be between $25,000 and $75,000. These costs are considered minimal compared to other expensive procedures or chronic conditions. For example, defibrillator implants range from $68,000 to $102,000, and cystic fibrosis treatments cost $300,000 per year.

Many transgender people face barriers in accessing gender-affirming surgery due to insurance denials and out-of-pocket expenses. However, organisations like the Gender Confirmation Center (GCC) and HealthPartners aim to reduce these barriers by offering free consultations and insurance concierge services that have successfully secured insurance coverage for a majority of their patients. Additionally, using a Flexible Spending Account (FSA) or Health Savings Account (HSA) can help reduce out-of-pocket costs for gender-affirming care as the money in these accounts is tax-free and can be used for medical treatments and procedures.

It is important to note that prior authorisation from your insurance provider is typically required for gender-affirming surgery, even if it wasn't necessary for hormone therapy. The specific coverage and requirements vary depending on your insurance plan, so it is essential to review your plan details and confirm all out-of-pocket costs before proceeding with surgery.

Get Medical Help Without Insurance: Your Options Explained

You may want to see also

Explore related products

![]()

Transition-related care

The cost of transition-related care varies depending on the specific treatments and procedures involved. While some insurance plans deny benefits to transgender individuals for medical care related to transitioning, studies have shown that providing coverage for these procedures is cost-effective. The total costs of transition-related care for one person are often estimated to be between $25,000 and $75,000. These costs are relatively minimal when compared to other expensive medical procedures.

In the United States, it is believed that between 3,000 and 9,000 people undergo sex reassignment surgery each year. While this is a small percentage of the population, the impact of providing coverage for these procedures can be significant for those who need them. In addition, providing access to transition-related care has been shown to positively impact the mental and physical health of transgender individuals, leading to decreased anxiety, depression, and psychological distress, and increased quality of life.

Understanding Medicare with Employer-Provided Insurance Coverage

You may want to see also

Explore related products

![]()

Preventative services

It is important to note that insurance companies cannot limit sex-specific recommended preventive services based on assigned sex at birth, gender identity, or recorded gender. For example, a transgender man with residual breast tissue or an intact cervix should have access to a mammogram or pap smear if their doctor deems it medically appropriate.

In addition to STD testing and screenings, other preventive care services like vaccines, cholesterol screenings, blood pressure screenings, and certain mental health screenings are typically covered under most health insurance plans. Most plans also cover at least one wellness visit per year, and some may cover additional preventive services, tests, and screenings based on current medical guidelines and an individual's medical history.

When it comes to gender-affirming care, insurance coverage can vary. While some insurance companies may cover a range of gender-affirming health services, others may have exclusions. It is essential to carefully review the terms of coverage, looking for explicit exclusions related to transgender healthcare. If you are unsure about how services would be covered or excluded, it is recommended to contact your health plan directly. Additionally, prior authorization or letters from a provider may be required by insurance companies to demonstrate the medical necessity of a service or medication.

In the context of Medicare, gender-affirming surgery coverage is determined by an individual's plan, which decides whether the surgery is medically necessary. Individuals typically pay the Medicare Part A deductible for major surgeries, the Part B deductible, and 20% coinsurance for any outpatient procedures. However, Medicare does not cover procedures it considers cosmetic surgery.

To summarize, while there may be variations in insurance coverage for specific procedures and treatments related to transgender healthcare, preventive services are often mandated by law and provided at no cost to the patient. It is crucial to carefully review insurance plans and understand the scope of covered procedures, medications, and resources, as well as appeal rights in cases of denial.

Medical Insurance: A Replacement Option for Medicare?

You may want to see also

Explore related products

![]()

Discrimination and transgender health insurance

Despite federal law prohibiting most public and private health plans from discriminating against transgender individuals, many transgender people continue to face discriminatory denials of care. While some employers and health insurance companies offer at least one plan that covers transition care, most US health insurance policies still contain transgender exclusions.

In 2014, the Center for Medicare and Medicaid Services began paying for sex reassignment surgery and other transitional care, after a 33-year ban on covering those costs was lifted. However, in 2024, only 24 states and Washington, D.C., prohibited transgender exclusions in health insurance service coverage. Eight states and Washington, D.C., had laws prohibiting health insurance discrimination based on gender identity, while 15 states, one territory, and Washington, D.C., had laws prohibiting health insurance discrimination based on sexual orientation and gender identity. Notably, no states had laws prohibiting discrimination based solely on sexual orientation.

In addition, while insurance nondiscrimination laws and policies exist to protect LGBTQ individuals from being unfairly denied coverage or excluded from specific procedures based on sexual orientation or gender identity, the reality is that many health insurance companies still restrict access to gender-affirming care. This leaves transgender individuals facing discriminatory denials of necessary care. For example, a health plan that categorically excludes all coverage for facial feminization surgery or imposes arbitrary age limits that contradict medical standards of care is engaging in unlawful discrimination.

The high cost of surgery is often cited as a reason for denying coverage for gender-affirming procedures. However, studies have shown that providing funding for sex reassignment surgery and hormones is cost-effective. The cost of surgery and hormones is not significantly higher than the cost of treating depression, substance abuse, and HIV/AIDS, which are prevalent among transgender individuals who cannot transition due to financial barriers. Furthermore, making insurance plans inclusive is generally inexpensive, as only a small percentage of people undergo transgender-specific medical treatment, and the one-time costs of surgical procedures are minimal compared to other expensive procedures.

To address discrimination in transgender health insurance, individuals can seek preauthorization for care and appeal insurance denials. They can also contact legal organizations, such as the National Center for Lesbian Rights or the Transgender Law Center, for guidance and support in fighting discriminatory policies.

Veba Plans: Reimbursing Medical Insurance Premiums?

You may want to see also

Explore related products

![]()

Financial options

The cost of gender-affirming surgery can vary depending on the specific procedure and the surgeon's experience. A 2022 study found that the cost of surgery can range from $6,900 to $63,400, with out-of-pocket expenses varying based on insurance coverage. The total costs of transgender-specific care for an individual are often estimated to be between $25,000 and $75,000. These costs are considered minimal compared to other expensive medical procedures.

It is important to check with your insurance provider to understand your coverage for gender-affirming care. While some insurance companies recognize these procedures as medically necessary, others may consider them cosmetic and exclude them from coverage. Federally funded health insurance programs cannot deny coverage based on gender identity due to Section 1557 of the Affordable Care Act. However, this does not apply to private insurance companies, and several states have passed laws banning or restricting access to gender-affirming care for minors.

If your insurance plan does not cover gender-affirming surgery, there are other financial options to consider. Some surgical practices partner with medical credit organizations to help patients finance their procedures. Additionally, you can explore payment plans or loans from financial institutions to cover the costs.

It is worth noting that the cost of surgery is not the only financial consideration. Facility-related costs, such as operating room fees, anesthesia, and hospital stays, can add up. Pre-surgical charges for postoperative supplies will also contribute to the overall cost. These expenses should be factored into your financial planning for gender-affirming surgery.

While the financial aspects of gender-affirming surgery can be complex, there are resources available to help patients navigate insurance coverage and explore alternative funding options. Seeking information from your insurance provider and surgical practices is a crucial step in understanding the financial options available to you.

Medical Exams for Children's Life Insurance: Are They Necessary?

You may want to see also

Frequently asked questions

Gender-affirming care is a phrase used by most medical groups for dysphoria treatment. This care can include hormones, surgery, or counseling. The care aligns a person's gender identity with gender expression in appearance, anatomy, and voice.

Many insurance providers offer coverage for gender-affirming surgery. However, it is not a requirement for a single health insurance plan to cover any specific kind of procedure. For private insurers who do cover gender-affirming surgery, a patient must first prove that the procedure is medically necessary.

Before enrolling in a plan, carefully review its terms. Plans might use different language to describe exclusions, so look for terms like "sex change", "transsexualism", "gender identity disorder", and "gender dysphoria". If you are still unsure, contact your health plan directly by phone.

If you are unable to get insurance coverage, other options include paying out of pocket, taking out a personal loan, or seeking financial help from charities and organizations.