The cost of health insurance varies depending on a range of factors, including age, location, and the type of plan. In 2024, the average annual health insurance premium was $8,951 for single coverage and $25,572 for family coverage, with higher premiums for older individuals and those in the Northeast. The cost of health insurance is also influenced by the plan's metal tier, with higher premiums for gold and platinum plans. Additionally, group health insurance plans, such as employer-sponsored coverage, tend to be cheaper than individual plans. When considering the cost of health insurance, it's important to factor in deductibles, copayments, and coinsurance, which can significantly impact total yearly costs.

Explore related products

What You'll Learn

![]()

Average annual insurance costs

The average annual cost of health insurance in the United States varies depending on several factors, including age, plan type, and location.

According to Forbes, the average annual health insurance cost is $7,080 for ACA (Affordable Care Act) marketplace plans. The cost of health insurance on the ACA marketplace varies based on multiple factors, with Forbes listing age, smoking status, location, metal tier, and plan type as key determinants of price. The average monthly cost of health insurance for a single person also varies depending on age, with a 21-year-old paying $445, a 27-year-old paying $467, and a 30-year-old paying $505. As people age, the cost of health insurance increases, with health insurance for a 60-year-old costing $1,478 per month.

The type of plan also affects the average annual insurance cost. For example, the average annual deductible for employer-sponsored health plans ranges from $1,000 to over $2,600. The average annual health insurance deductible is $5,774 for a bronze plan, $4,483 for a silver plan, and $1,092 for a gold plan. Platinum plans, which are rare, have the lowest deductibles but the highest premiums, with an average monthly cost of $1,166.

The cost of health insurance also varies depending on location. For example, Virginia has the lowest health insurance premiums, with an average monthly cost of $390, while West Virginia has the highest, with an average monthly premium of $864.

It is worth noting that many Americans qualify for subsidies that make buying health insurance more affordable. Additionally, individuals may have lower-cost options if their employer offers health benefits or they are eligible for government insurance programs such as Medicaid or Medicare.

Life Insurance and Medicaid: Understanding Payout Implications

You may want to see also

Explore related products

![]()

Premium tax credits and subsidies

The Premium Tax Credit (PTC) is a refundable tax credit that helps eligible individuals and families cover the premiums for their health insurance purchased through the Health Insurance Marketplace (also known as the Exchange). The size of the PTC is based on a sliding scale, with larger credits going to those with lower incomes to help cover the cost of their insurance.

To be eligible for the PTC, your household income must be at least 100% and, for years other than 2021 and 2022, no more than 400% of the federal poverty line for your family size. For 2021 and 2022, the American Rescue Plan Act of 2021 (ARPA) temporarily eliminated the rule that a taxpayer with household income above 400% of the federal poverty line cannot qualify for a premium tax credit. There are two exceptions for individuals with household incomes below 100% of the applicable federal poverty line.

To receive a premium tax credit for 2025 coverage, a Marketplace enrollee must meet the following criteria:

- Have a household income at least equal to the Federal Poverty Level (FPL).

- Not have access to an employer plan (including a family member’s employer) that meets minimum value and is considered affordable.

- Not be eligible for coverage through Medicare, Medicaid, or the Children’s Health Insurance Program (CHIP).

- Have U.S. citizenship or proof of legal residency.

Advance credit payments are amounts paid to your insurance company on your behalf to lower the out-of-pocket cost for your health insurance premiums. If you choose to have advance payments of the PTC made on your behalf, you will be required to file Form 8962 with your income tax return to reconcile the amount of advance payments with the PTC that you may claim based on your actual household income and family size.

Disability Insurance: No Medical Check-Up Required?

You may want to see also

Explore related products

![]()

Deductibles, copayments, and coinsurance

The cost of full medical insurance is influenced by several factors, including deductibles, copayments, and coinsurance. These factors determine the amount you pay out-of-pocket before and after meeting your deductible.

Deductibles

A deductible is the amount you pay for covered health services and prescription drugs before your insurance plan starts contributing. In other words, it is the amount you need to spend on eligible medical services or medications before your health plan begins to share the cost. For example, if you have a $1,500 deductible, you will need to pay the first $1,500 of your total eligible medical costs before your insurance plan starts helping with the expenses. Deductibles vary depending on the plan and can range from $1,500 to $2,000 or more.

Copayments

A copayment, often shortened to copay, is a flat fee or set rate you pay each time you receive a specific covered service, such as a doctor's visit or medication. Copays are typically predetermined by your health insurance plan and can be found on your health plan ID card. They are paid at the time of service, and the amount varies depending on the type of service received. For example, a visit to the doctor for an illness may incur a $20 copay. Some plans may use both copays and deductibles/coinsurance, depending on the type of covered service.

Coinsurance

Coinsurance is the percentage of the covered amount that you pay after you have met your deductible. It is a way of sharing the cost of your medical expenses with your insurance carrier. For example, if you have an 80/20 coinsurance plan, you will pay 20% of the cost of your covered medical bills, while your insurance plan will pay the remaining 80%. The higher your coinsurance percentage, the higher your share of the cost. Coinsurance is typically applied after you have met your deductible for the year.

Protective Health Insurance: Can They Access My Medical Records?

You may want to see also

Explore related products

![]()

Cost variation by state and age

The cost of full medical insurance in the US varies depending on several factors, including age, location, and plan type. Firstly, let's break down the cost variation by state. The cost of health insurance differs from state to state, and this variation can be significant. For example, health insurance in Alaska is more than double the cost in Indiana. The number of insurance companies and plans available in a state can impact the cost; fewer companies in a state may result in higher prices. Additionally, each state has its own regulations and insurance companies offer different plans in different locations, contributing to the variation in costs across states.

Now, let's discuss the impact of age on insurance costs. Generally, health insurance rates increase with age. Younger individuals can expect to pay lower rates, while older individuals, especially those in their 50s, 60s, and above, will likely face higher premiums. Interestingly, age doesn't factor into rate-setting for employer-sponsored insurance but is a consideration for ACA marketplace plans. The difference in rates between age groups can be substantial, with insurance companies allowed to charge up to three times more for people in their 60s compared to those in their early 20s.

Therapy and Medical Insurance: What's Covered?

You may want to see also

Explore related products

![]()

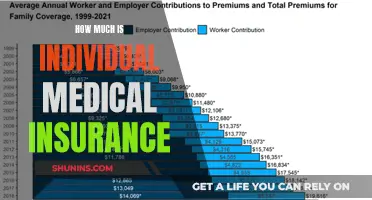

Employer-sponsored health insurance

ESI is a way for employers to provide health benefits for their workers and their families. The average employer pays the majority of the cost, but employees typically pay a portion of the premiums through payroll deduction. In 2023, the average employer-sponsored health plan had a total monthly premium of $703 for a single employee and $1,997 for family coverage. Group health insurance plans, including small-group, large-group, and self-insured plans, are guaranteed issue, meaning that the plan must cover all enrollees whose employment qualifies them for coverage.

The Affordable Care Act (ACA) includes an 'employer mandate' that applies to all businesses with at least 50 full-time equivalent employees (FTEs). These employers are required to offer affordable, minimum-value insurance to their full-time (at least 30 hours per week) workers or face a potential tax penalty. Employers can purchase small-group or large-group coverage, depending on the number of employees they have. Alternatively, they can self-insure, meaning they pay employees' medical claims out of pocket rather than purchasing coverage from an insurer.

Federal and state laws divide ESI into the small group and large group markets, based on the number of FTEs working for the employer sponsoring the plan. Generally, employers with fewer than 50 FTEs are in the small group market, while employers with at least 50 FTEs are in the large group market. However, states can choose to raise the small group market limit to fewer than 100 FTEs. The regulatory requirements for the small and large group markets differ, with the small group insured market being subject to more extensive rules about benefits and ratings.

ESI provides an efficient way to offer coverage options to working families, and the tax benefits of employer-based coverage make it even more attractive. However, it often results in uneven coverage, especially for those with low wages or those working at smaller firms.

Prescription Insurance: A Medical Insurance Companion?

You may want to see also

Frequently asked questions

The cost of full medical insurance depends on several factors, including age, location, and plan type. The average annual health insurance cost for an individual in 2024 was $8,951, while family coverage was $25,572. The average cost for a single 30-year-old in 2025 is $505 per month. The premium for an ACA health insurance plan is $590 per month, with the average bronze plan costing $495 per month and the average gold plan costing $655 per month.

The cost of full medical insurance is influenced by factors such as age, with older individuals typically paying higher premiums. The type of plan, such as HMO or PPO, and the metal tier of the plan can also impact the cost. Additionally, location plays a role, with premiums varying across different states and regions.

Yes, there are a few ways to save on full medical insurance. Group health insurance plans, often offered by employers, tend to be more cost-effective as the employer may contribute to the premiums. Additionally, entering household income information on the ACA marketplace website can help identify affordable plans or eligibility for premium tax credits and subsidies.

Full medical insurance coverage typically includes regular check-ups, preventive care, surgeries, and ongoing treatment regimens. It may also cover specific services such as doctor visits, lab tests, and outpatient care, depending on the plan chosen.

When choosing a full medical insurance plan, it is important to consider your health needs and financial situation. If you anticipate needing significant medical care, opting for a plan with higher monthly premiums can help avoid high out-of-pocket costs. Additionally, comparing different plans based on their benefits, coverage limits, and cost-sharing requirements can help you select the most suitable option.