The cost of good medical insurance is a complex topic influenced by several factors, including age, location, income, plan type, and metal tier. The average monthly premium for an individual health insurance plan in the US is $456, but prices vary depending on personal circumstances and the level of coverage chosen. For example, the average monthly cost for a 21-year-old is $445, while a 30-year-old can expect to pay around $618. The type of plan, such as bronze, silver, gold, or platinum, also impacts the price, with higher premiums typically resulting in lower out-of-pocket costs. Additionally, factors like deductibles, copayments, and coinsurance can significantly affect total yearly expenses. Understanding these variables is crucial when selecting a plan that balances cost and coverage to meet specific healthcare needs.

Explore related products

What You'll Learn

![]()

Premium tax credits and subsidies

The Affordable Care Act (ACA) provides sliding-scale subsidies that lower premiums and insurers offer plans with reduced out-of-pocket (OOP) costs for eligible individuals. There are two types of financial assistance available to Marketplace enrollees: the premium tax credit and the cost-sharing reduction (CSR). The premium tax credit is a refundable tax credit designed to help eligible individuals and families with low or moderate incomes afford health insurance purchased through the Health Insurance Marketplace. The size of the premium tax credit is based on a sliding scale, with those who have a lower income receiving a larger credit to help cover the cost of their insurance. The credit amounts are then reconciled with the actual income at year's end when enrollees file their federal taxes.

To be eligible for the premium tax credit, your household income must be at least 100% and, for years other than 2021 and 2022, no more than 400% of the federal poverty line for your family size. For tax years 2021 and 2022, the American Rescue Plan of 2021 (ARPA) temporarily expanded eligibility for the premium tax credit by eliminating the rule that a taxpayer is not allowed a premium tax credit if their household income is above 400% of the federal poverty line. However, individuals making above 400% of the FPL whose required contribution for a benchmark silver premium is greater than the actual cost of a benchmark silver plan relative to their household income would be ineligible for subsidies.

To receive a premium tax credit for 2025 coverage, a Marketplace enrollee must meet the following criteria: have a household income at least equal to the Federal Poverty Level (FPL); not have access to an employer plan (including a family member's employer) that both meets the minimum value and is considered affordable; not be eligible for coverage through Medicare, Medicaid, or the Children's Health Insurance Program (CHIP); and have U.S. citizenship or proof of legal residency. Lawfully present immigrants whose household income is below 100% FPL can also be eligible for tax subsidies through the Marketplace if they meet all other eligibility requirements.

When you enroll, the Marketplace will determine if you are eligible for advance payments of the premium tax credit, also called advance credit payments or APTC. Advance credit payments are amounts paid to your insurance company on your behalf to lower the out-of-pocket cost for your health insurance premiums. If you benefit from advance payments of the premium tax credit, it is important to report life changes to the Marketplace as they happen throughout the year, as certain changes to your household, income, or family size may affect the amount of your premium tax credit.

Medical Insurance and Translation Fees: What's Covered?

You may want to see also

Explore related products

![]()

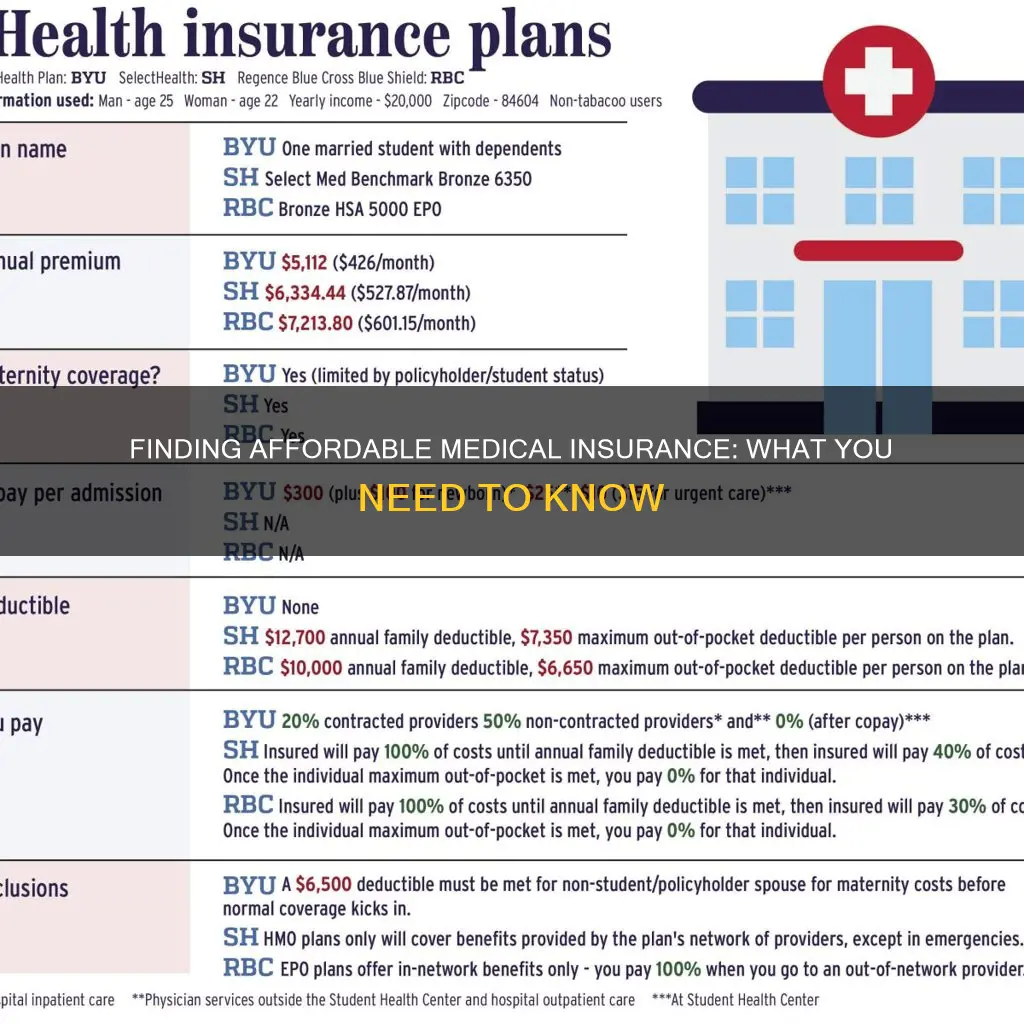

Plan types: EPO, HMO, PPO

The cost of medical insurance varies depending on factors such as age, type of plan, and metal tier. For example, the average monthly health insurance cost for a single person ranges from $445 for a 21-year-old to $505 for a 30-year-old. The average annual cost for an ACA marketplace plan is $7,080, but this can be reduced through premium tax credits and cost-saving subsidies.

Now, let's delve into the details of EPO, HMO, and PPO plan types:

EPO (Exclusive Provider Organization)

EPO plans typically offer lower monthly premiums but higher deductibles. This means you pay less each month but may end up paying more when you need healthcare services. EPO plans require you to stay within their network of select providers, and you may have to pay the full cost if you seek care outside the network. EPOs usually have larger networks than HMOs and may not require referrals from a primary care physician. They are suitable for those seeking a more budget-friendly option and those who are comfortable with a limited network of providers.

HMO (Health Maintenance Organization)

HMO plans are designed to help maintain your health. They often come with higher monthly premiums or higher deductibles. You typically need to use in-network providers and obtain referrals from your primary care physician (PCP) to see specialists. HMOs may be a good choice if you are comfortable with a PCP coordinating your care and referring you to specialists.

PPO (Preferred Provider Organization)

PPO plans offer more flexibility and choice in terms of physicians and healthcare options but usually come with higher monthly premiums. They allow you to see specialists and out-of-network doctors without a referral, and you'll pay lower out-of-pocket costs when using in-network providers. PPOs are ideal if you want more freedom in choosing your healthcare providers and don't want to go through a PCP for referrals.

Utah Hospital: What Medical Insurance is Offered?

You may want to see also

Explore related products

![]()

Coinsurance and copayments

A copayment, or copay, is a fixed cost that an insurance policyholder pays for a specific service covered by their insurance. Copayments are usually paid at the time of service and are a flat fee that you pay on the spot each time you go to your doctor, fill a prescription, or receive another covered medical expense. Copayments do not typically count toward your deductible. Copays vary depending on the type of healthcare service and can be different for emergency rooms versus urgent care centres, or for different prescription drugs.

Coinsurance, on the other hand, is a percentage of the cost of a service. It is the portion of the medical cost you pay after your deductible has been met. Coinsurance levels are often between 20% and 40%, depending on the health plan. Unlike copayments, coinsurance does not have different amounts based on the type of care. The higher your coinsurance percentage, the higher your share of the cost.

Both copayments and coinsurance contribute to your out-of-pocket maximum, which is the most you'll have to pay out of pocket each year. Once you reach this maximum, your insurance company will pay 100% of the costs of covered services for the remainder of the policy year.

Using Medical Insurance Abroad: What's Covered?

You may want to see also

Explore related products

$72.77 $111.95

$70.54 $105.95

![]()

Out-of-pocket maximums

An out-of-pocket maximum, also known as an out-of-pocket limit, is the maximum amount of money a health insurance policyholder will have to pay each year for covered healthcare expenses. Once the policyholder reaches this limit, the insurance company will cover 100% of their qualified expenses for the rest of the plan year.

The out-of-pocket maximum is reached when a policyholder has spent a certain amount in a plan year on deductibles, copayments, and coinsurance for in-network care and services. The out-of-pocket maximum for a plan does not include costs for out-of-network care and services, or for care and services that are not covered by the plan. For example, cosmetic treatments, weight loss surgery, and some alternative medicine may not be covered by a plan.

The federal government publishes new guidelines each year that include the highest out-of-pocket maximum that health plans can impose. The upper limit for 2025 is $9,200 for an individual and $18,400 for multiple family members on the same plan. These limits are set to increase in 2026 to $10,150 and $20,300, respectively.

The out-of-pocket maximum varies depending on the plan. Plans with lower out-of-pocket maximums tend to have higher premiums, while plans with higher out-of-pocket maximums have lower premiums. Some individuals or families may qualify for lower out-of-pocket maximums if they meet certain requirements, such as earning below a certain income threshold.

Best Medical Insurance Options for Retirees

You may want to see also

Explore related products

![]()

Age and location

The cost of good medical insurance varies depending on several factors, including age and location. Let's break down the impact of these factors:

Age

Age plays a significant role in determining the cost of health insurance. Generally, health insurance is cheapest for young adults, teenagers, and children. As individuals get older, the rates tend to increase. For example, the average cost of health insurance is $444 per month for 18-year-olds, $486 per month for 24-year-olds, and $498 per month for 26-year-olds. By the time individuals reach their 30s, the average monthly cost increases to $505. The rates continue to rise faster when individuals reach their 50s and 60s. However, once individuals turn 65 and become eligible for Medicare, it is usually more cost-effective to choose Medicare over private health insurance.

Location

Location is another critical factor influencing the cost of health insurance. The average premium can vary significantly from state to state. For instance, the average premium in New Hampshire is $323, while in Wyoming, it soars to $802. The cost of living and the availability of healthcare providers in a particular area can also impact the price of health insurance.

It is important to note that other factors, such as smoking status, plan type, metal tier, household income, and family size, also contribute to the overall cost of health insurance. Comparing quotes from multiple insurance companies and exploring options like Medicaid and Medicare can help individuals find the most suitable and affordable coverage for their needs.

Medicaid and Other Insurance: Can I Have Both?

You may want to see also

Frequently asked questions

A health insurance premium is the monthly fee you pay to have health insurance. The average premium in the US is $456 per month for an individual plan and $1,483 for a family of four. The cost of a premium depends on your age, income, location, and whether you use tobacco.

Coinsurance is the percentage of the covered amount that you pay. It is typically about 20%. For example, if a covered service costs $125, you would pay $25 (20%) and your insurance would pay the remaining $100 (80%).

There are four types of health insurance plans: Bronze, Silver, Gold, and Platinum. Bronze plans have the lowest premiums but the highest out-of-pocket costs, while Platinum plans have the highest premiums but the lowest out-of-pocket costs. Silver and Gold plans offer a balance between premiums and out-of-pocket expenses.