The average cost of homeowners insurance in the US varies depending on several factors, including location, the size of the home, and the coverage amount. On average, homeowners insurance in the US costs between $2,110 and $2,466 per year for $300,000 in dwelling coverage. However, rates can vary significantly by state, with Oklahoma, Texas, and Nebraska being among the most expensive states for home insurance, while Hawaii, Vermont, and Delaware are among the cheapest. The age of the home, the homeowner's credit history, and the deductible amount also influence the cost of homeowners insurance.

| Characteristics | Values |

|---|---|

| Average annual cost of homeowners insurance in the U.S. | $1,951-$2,601 |

| Average monthly cost of homeowners insurance in the U.S. | $217 |

| Average annual cost of homeowners insurance with $350,000 dwelling coverage | $1,951 |

| Average annual cost of homeowners insurance with $300,000 dwelling coverage | $2,601 |

| Average annual cost of homeowners insurance with $200,000 dwelling coverage | $461 (Hawaii) - $5,858 (Oklahoma) |

| Average annual cost of homeowners insurance with $400,000 dwelling coverage | $791 (Hawaii) - $7,012 (Oklahoma) |

| Average annual cost of homeowners insurance with $750,000 dwelling coverage | Westfield has the best rates |

| Average annual cost of homeowners insurance with $500,000 dwelling coverage | Progressive has the cheapest rates |

| Cheapest widely available home insurance company | Travelers ($2,055) |

| Most expensive widely available home insurance company | American Family ($2,745) |

| Cheapest state for homeowners insurance | Hawaii |

| Most expensive state for homeowners insurance | Oklahoma |

| Other expensive states for homeowners insurance | Texas, Nebraska, Colorado, Kansas, North Carolina |

| Other cheap states for homeowners insurance | Vermont, Delaware, Alaska, Maine |

| Factors influencing insurance costs | Location, claims history, coverage limits, home characteristics, age of home, credit history, liability concerns, crime rates, construction materials, roof type, business run from home, dog ownership |

Explore related products

$14.99 $14.99

What You'll Learn

![]()

Home insurance costs vary by state

The cost of home insurance varies across the United States, with several factors influencing the price. The national average is $2,466 per year for $300,000 in dwelling coverage, but this cost will differ depending on the state.

For example, Oklahoma has the highest insurance rates, with an average of $5,858 to $6,210 a year. Texas, Nebraska, Colorado, and Kansas are also among the most expensive states for home insurance. On the other hand, Hawaii is the cheapest state for home insurance, with an average rate of $610 to $613 a year. Vermont, Delaware, Alaska, and Maine are also among the states with the lowest insurance rates.

Location plays a significant role in determining insurance costs due to varying levels of risk across the country. For instance, homes in the Midwest tend to have higher premiums due to the increased risk of tornadoes and windstorms. Coastal areas are also prone to higher premiums because of the risk of flooding and high winds. Additionally, states like California have experienced rate hikes due to severe storms and wildfires.

Other factors that influence insurance rates include the age and construction materials of the home, the coverage amount, the presence of attractive nuisances like swimming pools, and the homeowner's credit history. Inflation and the increased frequency of natural disasters have also contributed to rising insurance costs.

Mortgage Insurance: APR Fee or Extra Cost?

You may want to see also

Explore related products

![]()

Older homes are more expensive to insure

The average cost of homeowners insurance for a 12-month policy ranges from $1,090.08 to $3,353.74 per year, depending on various factors. The cost of home insurance is influenced by factors such as location, claims history, coverage limits, and home characteristics. Oklahoma, Texas, and Nebraska are among the most expensive states for home insurance, while Hawaii, Vermont, and Delaware are the least expensive.

Older homes are often more expensive to insure than newer ones due to several reasons. Firstly, older homes may not have the same safety features as modern homes, and repairs can be more costly. They may also be built with harder-to-source materials, making them more expensive to rebuild or repair after a loss. Additionally, older homes may need to be brought up to modern safety and building codes, further increasing costs.

The age of a home is a significant factor in determining insurance costs. Some insurers consider homes built over 40 years ago as older properties, and these homes may require specialized coverage. The cost of rebuilding an older home can exceed its market value, especially if rare or handmade materials were used. Outdated plumbing systems in older homes are more prone to leaks, blockages, and burst pipes.

The construction materials used in older homes may be obsolete and more expensive to replace. Features such as plaster walls, stucco, and custom architectural details were common in pre-war homes and are costlier than modern materials. The unique or antique furnishings in older homes may also require additional coverage to protect their higher value.

To lower insurance rates for older homes, homeowners can consider increasing their dwelling or personal property coverage deductibles or bundling their homeowners insurance with other policies. Updating older homes, such as installing a new roof, can also help safeguard the property against damage and potentially reduce insurance rates.

Homeowner Insurance in California: What's the Cost?

You may want to see also

Explore related products

![]()

Attractive nuisances increase liability

The cost of homeowners' insurance varies widely, with location being a significant factor in determining the price. The average cost of insurance for a 12-month policy ranges from $1,090.08 to $3,353.74 per year. However, in certain states, the average cost can be significantly higher. For example, in Oklahoma, the average annual cost is $6,210. The cost of insurance is impacted by factors such as the size of the house, the dwelling coverage, the construction materials used, and the claims history.

When it comes to attractive nuisances, homeowners should be aware that these can increase their liability and, consequently, their insurance rates. Attractive nuisances are objects or conditions on a property that may attract children and pose a potential hazard. Some common examples include swimming pools, trampolines, playground equipment, abandoned vehicles, and construction sites. The attractive nuisance doctrine holds landowners liable for injuries caused to children trespassing on their property by such attractions. The key factors in determining liability are the age of the child, the potential for harm, the landowner's knowledge of the attraction's appeal to children, and the failure to take appropriate steps to limit access or mitigate the risk.

To reduce liability, homeowners can take several precautions. Firstly, they should ensure that their property is properly secured and that hazardous objects are not easily accessible. This may include installing locked fences around swimming pools or moving dangerous items out of reach. Additionally, posting "No Trespassing" signs may help deter children from entering the property, although it may not always reduce liability, especially if the children are unable to read or understand the warning.

In some cases, the nature of the attractive nuisance may also impact liability. Courts have distinguished between natural and artificial attractions, with artificial features, such as garden fountains, often considered more liable than natural ones, such as creeks. Furthermore, the age and ability of the child to understand the risk are also considered. If a child is old enough to comprehend the danger, the landowner may be shielded from liability.

To ensure adequate protection, landowners may consider increasing their personal liability coverage. This can be done by purchasing an umbrella insurance policy to cover any injury claims resulting from attractive nuisances. By taking the necessary precautions and maintaining safe conditions on their property, landowners can help reduce the risk of accidents and mitigate their liability.

Chicago Homeowners Insurance: What's the Real Cost?

You may want to see also

Explore related products

![]()

Credit history impacts insurance rates

The average cost of homeowners insurance varies depending on several factors, with location being a significant determinant. The average annual cost of homeowners insurance ranges from $610 in Hawaii to $6,210 in Oklahoma.

When it comes to insurance rates, credit history is a critical factor that can significantly impact your premiums. Insurance companies often use an individual's credit history to assess their financial risk and determine the price of coverage. Those with poor credit histories may face higher insurance rates or even be denied coverage.

Credit-based insurance scores are used by insurance companies to evaluate an individual's credit history. These scores are calculated using various factors, including outstanding debt, credit history length, credit mix, and payment history. Maintaining a good credit score can help individuals secure more favourable insurance rates.

Insurers typically consider the following when reviewing an individual's credit history:

- Number of open accounts

- Amount owed compared to available credit

- Past due payments

- Frequency of applying for new lines of credit

- Medical debts that went to collection

- Credit checks related to insurance coverage and other businesses

While credit history plays a role in determining insurance rates, it's important to note that other factors, such as location, claims history, coverage limits, and home characteristics, also influence the final premium.

U.S.A.A. Homeowners Insurance: Can It Be Cancelled?

You may want to see also

Explore related products

![]()

Construction materials affect costs

The cost of home insurance is influenced by a variety of factors, including the construction materials used in building a home. The choice of construction materials can impact the overall value of a property and its resilience to various risks, which in turn affects the insurance premium.

Firstly, the type of construction materials can determine the durability and resilience of a home against different hazards. For instance, homes with concrete block construction are less susceptible to fires and strong winds compared to wood frame houses, making them generally more affordable to insure. Similarly, roofing materials play a critical role, with asphalt shingles being less flammable and potentially resulting in lower insurance costs than cedar or wood-shake roofs. Additionally, homes with hip roofs (characterized by all sides sloping downward) are more resistant to wind damage than gable roofs, which may lead to reduced insurance costs.

The siding type is another important consideration for insurance companies when assessing risk. For example, brick siding is generally more durable and less expensive to insure than wood frame homes, which are more prone to fire and wind damage. Masonry veneer, on the other hand, is primarily decorative and may not provide the same structural benefits as other siding types.

The age of a home is also a significant factor in determining insurance costs. Older homes may be constructed with materials that are harder to source, making repairs more expensive. They may also lack modern safety features, resulting in higher premiums. Conversely, newer homes typically incorporate more recent construction materials and safety standards, reducing the potential for loss and resulting in lower insurance rates.

Furthermore, the interior finishes of a home can impact its overall replacement cost. Certain finishes may increase the replacement value of a building, leading to higher insurance premiums. This is because insurance companies base their rates on the replacement cost of a home, which reflects the current construction material prices in the market.

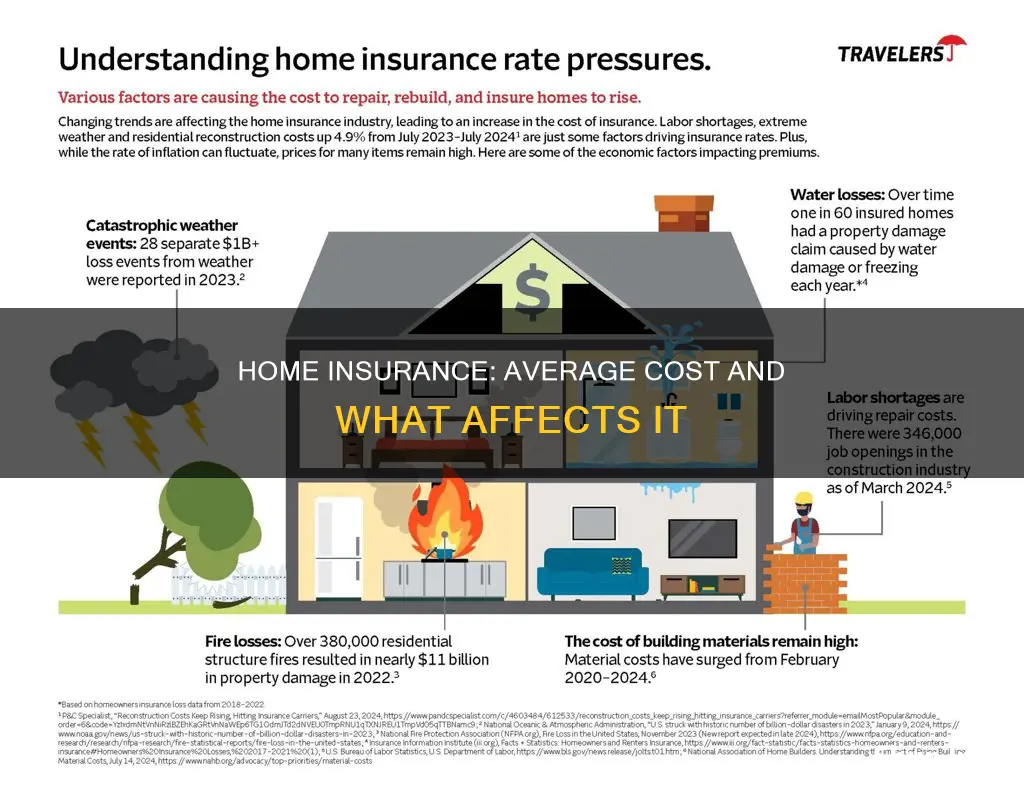

In recent years, the rising cost of construction materials has contributed to increasing insurance premiums. Since 2020, construction materials have experienced significant price increases, with over 80% of materials becoming more expensive. Consequently, insurance companies have had to adjust their rates to account for the higher project values and the potential for larger claims.

In summary, the choice of construction materials can significantly impact the cost of home insurance. Insurance companies assess the risk associated with different materials, considering their durability, fire resistance, wind resistance, and overall impact on the property's value. The age of the home and the interior finishes also play a role in determining the insurance premium. As construction material prices continue to rise, it is essential for homeowners to be aware of how these costs can influence their insurance rates.

Phone Insurance Claims: A Step-by-Step Guide

You may want to see also

Frequently asked questions

The average cost of homeowners insurance in the US is $2,110 a year for $300,000 worth of dwelling coverage. However, rates can vary by state, with Oklahoma, Texas, and Nebraska being the most expensive, and Hawaii, Vermont, and Delaware being the least expensive.

Many factors can influence the cost of homeowners insurance, including the location of the home, the size of the home, the age of the home, the coverage amount, and the deductible.

Homes located in areas perceived as risky, such as those prone to extreme weather, flooding, wildfires, or crime, will typically be more expensive to insure. Additionally, homes in coastal regions or near woods and brush may be riskier to insure due to the potential for natural disasters.

Larger homes generally have higher insurance rates because they have more surface area that can be damaged or destroyed, leading to higher repair and rebuilding costs.

Older homes may be more expensive to insure because they may not have modern safety features, and repairs can be costlier due to the need to source harder-to-find materials.