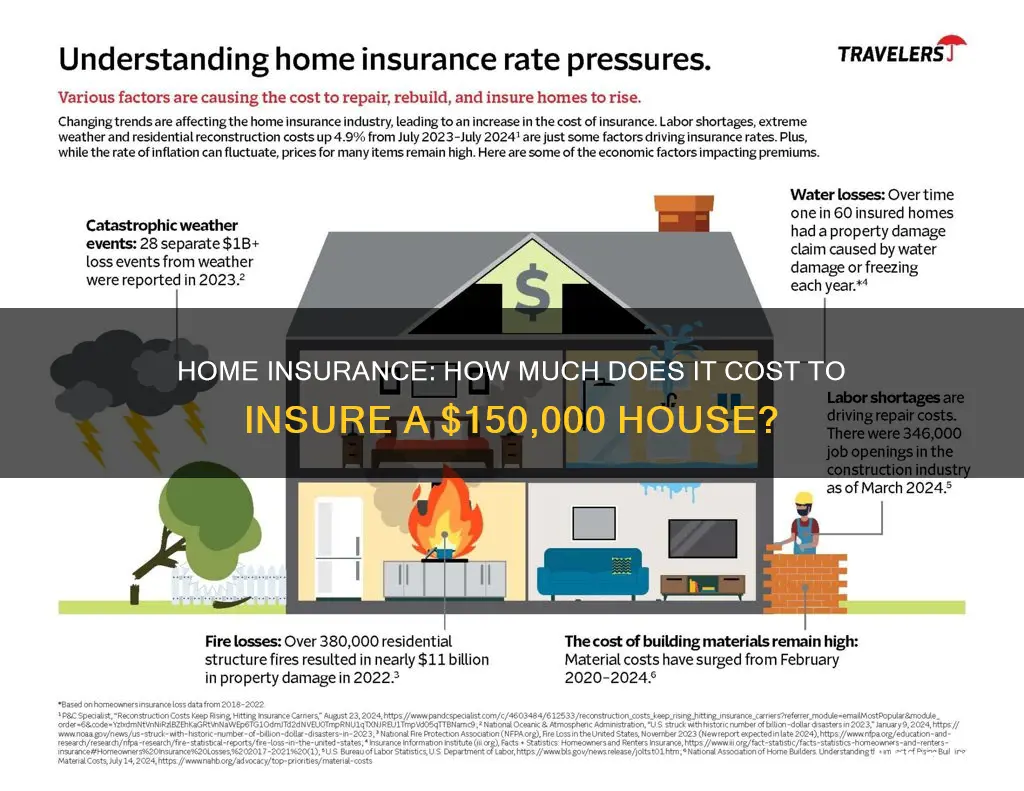

Homeowners insurance costs vary based on multiple factors, including location, age of the property, and the insurer's assessment of the home's level of risk. The average monthly cost of homeowners insurance for a $150,000 house is $109, or $1,308 per year. However, this can vary significantly depending on the state and local factors. For example, the average annual premium in Louisiana is $1,967 due to the risk of hurricanes and tropical storms, while Oregon has an average of $659 due to fewer natural disasters. Additionally, factors such as the home's dwelling coverage limit, replacement cost value, and policy deductible can impact the overall cost of insurance.

| Characteristics | Values |

|---|---|

| Average annual cost | $1,308 |

| Average monthly cost | $109 |

| Average annual cost (by state) | Louisiana: $1,967; Oregon: $659; Florida: $6,149; Vermont: $549 |

| Average annual cost (by company) | AIG: $3,564; Travelers: $1,415 |

| Factors influencing cost | Location, age, style, construction costs, risk of natural disasters, claims history, credit score, deductible, policy limits, additional structures, home usage, contents |

| Home insurance coverage | Damage to interior and exterior, personal property in case of theft or damage, liability for injuries to others on the property |

| Home insurance exclusions | Flood and earthquake damage, normal wear and tear, intentional damage |

Explore related products

$14.99 $14.99

What You'll Learn

![]()

Home insurance rates vary by state

Home insurance rates vary significantly across states in the USA. The national average cost of home insurance is $2,466 per year for a policy with a $300,000 dwelling limit, or $2,601 per year, according to some sources. However, the specific rates differ by state, with some states having much higher or lower rates than the national average. For instance, Oklahoma has the highest home insurance rates, with an average of $5,858 per year, while Hawaii has the lowest, with an average of $613 per year.

Several factors contribute to the variation in home insurance rates across states. One key factor is the risk of natural disasters, such as hurricanes, wildfires, floods, tornadoes, and windstorms. States with a higher risk of natural disasters tend to have higher insurance rates. For example, Florida has the highest insurance premium at $15,460 on average, possibly due to the state's susceptibility to hurricanes and wildfires. On the other hand, Vermont, Alaska, and Delaware are among the least expensive states for home insurance, as they may not face a high risk of natural disasters.

The cost of rebuilding or replacing a home after a disaster is another factor influencing insurance rates. States with a higher cost of living or higher construction costs will likely have higher insurance rates, as rebuilding or repairing a home will be more expensive. Additionally, insurance companies consider local crime rates when setting premiums, as areas with higher crime rates may be more prone to theft or vandalism, leading to higher insurance claims.

The age, location, and features of a home also play a role in determining insurance rates. Older homes may have higher premiums due to the increased risk of issues such as pipe damage or electrical problems. Homes in coastal areas or those with features like swimming pools may have higher insurance rates, as insurance companies consider these factors to increase liability risks.

It is worth noting that insurance rates can change over time due to factors such as inflation, the increased frequency and severity of natural disasters, and changes in the cost of building materials. Therefore, homeowners should regularly review their policies and consider the impact of these factors on their insurance costs.

Legal Protection: Is Your Home Insurance Enough?

You may want to see also

Explore related products

![]()

Home insurance rates vary by insurer

Home insurance rates vary significantly by insurer, and many factors influence the cost of coverage. Firstly, the location of the property is a significant determinant of insurance rates. Local weather patterns, crime rates, insurance laws, and construction costs all contribute to the variability of insurance rates across different states. For example, states that experience frequent natural disasters, such as hurricanes, tornadoes, and wildfires, tend to have higher insurance premiums. Additionally, the risk of natural disasters, such as flooding, can influence rates, with coastal areas near high-risk coastlines potentially facing higher premiums.

The characteristics of the home itself also play a crucial role in determining insurance rates. The construction materials used, the type of siding and roofing, and the heating system all impact the property's overall value and risk assessment. For instance, concrete block homes may be cheaper to insure than wood frame houses due to their higher resistance to fires and strong winds. Similarly, hip roofs, which are more resistant to wind, can help lower insurance costs compared to gable roofs.

The level of coverage and the chosen deductible also influence the rates. Higher coverage limits will generally result in higher premiums. Additionally, a higher deductible, which is the amount paid out of pocket before the insurance company pays a settlement, can affect the insurance rate.

The claims history is another factor considered by insurers. Previous claims indicate a higher risk of future claims, which may lead to increased premiums. Moreover, the presence of additional structures on the property, such as attached garages, sheds, or pools, can drive up insurance costs as they present more opportunities for claims.

It is worth noting that insurance rates are regulated state by state, and the average annual cost of homeowners insurance can vary widely. For example, Florida is known for having the highest insurance rates, with an average annual premium of $6,149 for a home with a $150,000 replacement cost value due to its hurricane risk. In contrast, Vermont has the lowest average annual premium at $549 for similar coverage.

When considering home insurance, it is essential to compare quotes from different insurers and carefully review the coverage offered to find the best rates and ensure adequate financial protection.

Carnival Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Home insurance rates depend on the home's location and risk

Home insurance rates are calculated based on various factors, with location being one of the most significant determinants. The cost of insuring a $150,000 house can vary significantly depending on where it is located within a state or even within a specific area of a town. For instance, in Tennessee, the average annual premium for a $150,000 home is $1,470, while in Idaho or Alaska, it is nearly six times cheaper.

Insurers consider the risk associated with the location, including the likelihood of natural disasters such as hurricanes, tornadoes, wildfires, or earthquakes. States that experience frequent natural disasters tend to have higher insurance premiums. For example, Louisiana, which is prone to hurricanes, has an average annual premium of $1,967, while Oregon, with fewer natural disasters, averages $659 per year. Similarly, Florida, with its high hurricane risk, has the most expensive home insurance rates in the country, with an average annual premium of $6,149 for a home with a $150,000 replacement cost value.

Location also impacts the replacement cost of a home, as construction costs, including labour and materials, can vary by region. The distance from emergency services, such as fire departments, also affects insurance rates, as homes farther away are considered higher risk in case of fire. Additionally, the local crime rate influences premiums, with areas experiencing frequent vandalism, theft, or burglaries resulting in higher rates.

Other location-specific factors that impact insurance rates include local weather patterns, insurance laws, and construction costs. For example, homes in high-risk flood zones may be required to have flood insurance, increasing the overall cost of insurance. Furthermore, the proximity to fire stations or fire hydrants can affect rates, with homes closer to these services sometimes receiving lower premiums.

While location plays a significant role in determining home insurance rates, it is essential to remember that other factors related to the home itself, such as age, construction style, and additional structures, also influence the cost of insurance. Additionally, the insurer's assessment of the home's level of risk and the coverage options chosen will impact the final insurance costs.

Fireworks and Home Insurance: What's Covered?

You may want to see also

Explore related products

![]()

Home insurance rates depend on the home's replacement cost value

Home insurance rates depend on a variety of factors, including the home's replacement cost value. This value refers to the amount it would take to rebuild the home from the ground up, using current prices for construction materials and labour. It is important to note that the replacement cost is different from the market value of the home, which is based on the amount buyers are willing to pay for it in the real estate market.

When determining the replacement cost value, insurance companies consider factors such as the size and structure of the home, as well as the cost of materials and labour needed to rebuild it. This value is used to set the coverage limit for the home insurance policy, which represents the maximum amount the insurer will pay in the event of a total loss. It is crucial to ensure that the coverage limit is sufficient to cover the full cost of rebuilding the home, as having a policy with too low of a limit can leave the homeowner financially vulnerable.

While insurance companies typically estimate the replacement cost on behalf of their customers, it is recommended that homeowners consider getting their own replacement cost estimate from a licensed appraiser. This can help ensure that the coverage limits are adequate and provide peace of mind that the home is sufficiently insured. Additionally, homeowners should review their policies annually to account for changes in construction costs and make any necessary adjustments to their coverage.

The replacement cost value of a home is just one factor that influences home insurance rates. Other factors include the location, age, and construction type of the home, as well as the coverage options and limits chosen by the homeowner. Natural disaster risks, such as hurricanes, tornadoes, and wildfires, can also significantly impact insurance premiums, with states facing higher risks tending to have higher average premiums.

In summary, home insurance rates are influenced by a variety of factors, including the home's replacement cost value. By understanding these factors and staying informed about market conditions, homeowners can make informed decisions about their insurance coverage and ensure they have adequate protection in the event of a loss.

Title Agent's Role: Canceling Home Insurance When Selling

You may want to see also

Explore related products

$9.97 $19.99

$8

![]()

Home insurance rates depend on the deductible

The cost of homeowners insurance for a $150,000 house varies depending on several factors, including location, style, age, and construction costs. For example, the average annual premium in Florida is $6,149, while in Vermont, it is $549.

Now, when it comes to home insurance rates and deductibles, it's important to understand that the deductible is the part of a claim that you're responsible for covering out of your own pocket. The higher your deductible, the lower your insurance premium, and vice versa. This is because the deductible reduces your claim payout. For example, if you have a $1,000 deductible and submit a claim for $8,000, your insurance company will pay out $7,000, and you'll cover the remaining $1,000.

Standard home insurance deductibles typically range from $500 to $2,000, but they can go as high as $5,000, or even $10,000 in the case of flood insurance. When choosing a deductible, consider what you can comfortably afford to pay out-of-pocket in the event of a claim. If you opt for a higher deductible to save on premiums, make sure you have the funds readily available to cover the higher amount when needed.

It's also worth noting that some policies have percentage deductibles, which are based on a percentage of your home's insured value. These typically apply to specific claims like wind, hail, or hurricane damage.

To find the right balance between your deductible and premium, it's a good idea to get quotes with different deductible amounts and compare rates. This will help you make an informed decision that fits your budget and coverage needs.

SCDW Insurance: Worth the Cost or Wasteful?

You may want to see also

Frequently asked questions

The average cost of home insurance for a $150,000 house is around $1,511 per year, according to Insurify. However, rates may vary depending on several factors, such as dwelling coverage, location, the age of the home, and construction costs.

The location of your home can significantly impact the cost of insurance. States with frequent natural disasters, such as hurricanes, tornadoes, or wildfires, generally experience higher insurance premiums. Additionally, factors such as the local crime rate and proximity to the coast can also affect premiums.

Dwelling coverage is a core component of your home insurance policy, paying for the cost to repair or rebuild your home in case of damage or destruction. The amount of dwelling coverage you need will depend on the size of your house and any additional structures, such as detached garages or fences. Opting for higher coverage limits will typically result in higher insurance rates.

You can reduce your home insurance costs by increasing your deductible, which is the amount you pay out of pocket before insurance coverage begins. A higher deductible will lead to lower monthly premiums. Additionally, maintaining a good credit score and a clean claims record can also help lower your insurance costs.