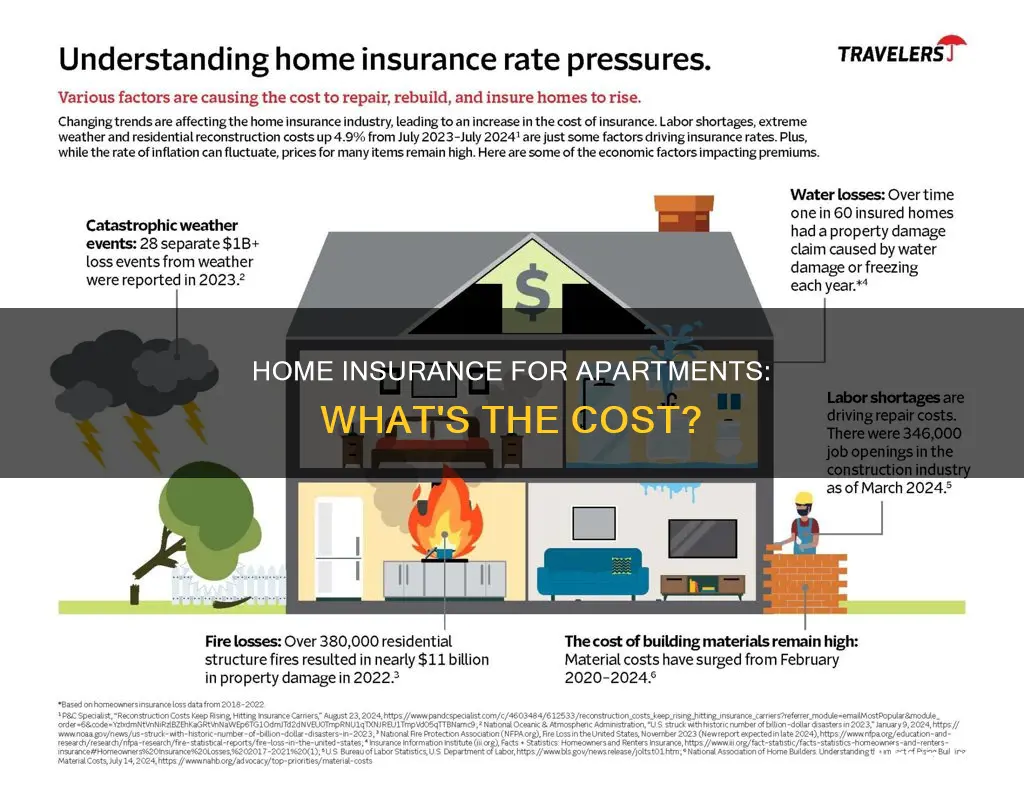

The cost of homeowners insurance for apartments depends on several factors, including the location, size, and characteristics of the property. For example, apartments in areas prone to severe weather or with higher crime rates may have higher insurance costs. The age and construction materials of the building, such as the type of roof or siding, can also impact the insurance rates. In the United States, the average cost of homeowners insurance is $2,110 per year, or about $176 per month, but this can vary significantly depending on the specific details of the property and the coverage required. Apartment building owners may require additional coverage, such as liability insurance and business income insurance, to protect against risks associated with renting out multiple units. Ultimately, the cost of homeowners insurance for apartments can vary widely, and it is essential to consult with an insurance agent to determine the appropriate coverage and associated costs.

| Characteristics | Values |

|---|---|

| Average cost of homeowners insurance | $2,110 a year or $176 a month |

| Range of costs | $1,090.08 a year ($90.84/month) to $3,353.74 a year ($279.48/month) |

| Factors affecting pricing | Location, claims history, coverage limits, home characteristics, construction materials, siding type, flooring materials, heating type, roof type, shape and construction, deductible, business usage, animal ownership, security measures |

| Exclusions | Flood damage, mold and mildew damage, deliberate damage by tenants, damage from lack of maintenance, pest damage, normal wear and tear |

| Additional coverage options | Umbrella policies ($1 million to $15 million), ordinance and law endorsement, business income insurance, animal liability coverage |

Explore related products

What You'll Learn

![]()

Homeowners insurance costs on average $2,110 a year

One of the main factors influencing the cost of homeowners insurance is location. The rates differ across states, with Oklahoma, Texas, and Nebraska being the most expensive, and Hawaii, Vermont, and Delaware being the least expensive. Additionally, homes in coastal regions or areas prone to severe weather, such as tornadoes, hurricanes, and hail, tend to have higher insurance costs due to the increased risk of natural disasters. Crime rates in the area can also impact insurance rates, as higher crime areas may lead to higher premiums to account for potential theft claims.

The characteristics of the home itself also play a crucial role in determining insurance costs. The construction materials used, such as roofing and siding types, can influence the overall value of the property and its susceptibility to certain types of damage. For example, asphalt shingles are less flammable and may result in lower insurance costs compared to cedar or wood-shake roofs. The age and square footage of the home are also considered, with older homes potentially requiring higher coverage due to outdated building codes and regulations.

The amount of coverage and deductible selected will also impact the cost of homeowners insurance. While increasing coverage may not significantly affect the rate, choosing a higher deductible can help minimize the overall insurance cost. Additionally, prior claims history can influence future rates, as multiple claims may indicate a higher risk of future incidents.

It's worth noting that apartment building owners have different insurance considerations. Liability insurance is crucial to protect against potential lawsuits and medical bills. General liability covers incidents such as tenant injuries or discrimination claims. Umbrella policies can provide additional coverage ranging from $1 million to $15 million, which can be beneficial for larger complexes. Business income insurance (BIC) is another important consideration, as it covers lost income due to repairs or damage to the building.

Federal Insurance Office: Who Does It Report To?

You may want to see also

Explore related products

$4.95 $14.95

![]()

Apartment insurance rates depend on location and building characteristics

Location is a significant factor in determining insurance rates. Properties in high-crime areas or regions prone to natural disasters such as floods, hurricanes, or earthquakes tend to have higher insurance premiums. For example, coastal states like Florida and Texas have seen insurance premiums rise by over 100% due to the increased risk of hurricanes. Areas with lower construction costs often have more favourable insurance rates. Crime rates in a particular ZIP code can also impact insurance rates, as a higher crime rate may lead to more theft and vandalism claims.

Building characteristics also play a crucial role in insurance costs. Older properties with outdated electrical, plumbing, or roofing systems often face higher premiums due to the increased risk of issues. The construction materials used can also impact rates, as certain materials may be more resistant to fires or strong winds, reducing the risk of damage. The building's age, value, and risk level are additional factors that influence insurance rates.

Other factors that can affect insurance rates include the coverage limits selected and the claims history of the property. Higher coverage limits provide better protection but result in higher premiums, while a history of claims can lead to increased premiums as the property is deemed higher risk.

Liberty Mutual: Is Their Homeowners Insurance Any Good?

You may want to see also

Explore related products

$9.97 $19.99

$8

![]()

Apartment insurance policies should include liability coverage

The cost of homeowners insurance for apartments varies depending on several factors, including location, the size of the apartment, and the coverage amount required. On average, homeowners insurance costs around $2,110 per year, or about $176 per month, but this can range from $1,090.08 to $3,353.74 annually.

Now, let's discuss why apartment insurance policies should include liability coverage:

Liability coverage is essential for apartment owners to protect themselves from potential financial risks. General liability insurance covers you in case someone gets injured on your property and sues you for negligence. For example, if a tenant or guest trips and falls due to improper maintenance, liability insurance will cover their medical expenses and any resulting lawsuits. This type of coverage is especially important for apartment building owners, as they face more risks compared to traditional homeowners.

In addition to covering injuries, liability insurance can also protect you from discrimination lawsuits. For instance, if a tenant or prospective tenant sues you for discrimination, your liability coverage will help with the legal costs.

Furthermore, liability insurance can provide financial protection in the event of property damage caused by negligence. For example, if a fire in your apartment damages the neighbouring unit, liability coverage will help pay for the associated expenses.

Another benefit of liability coverage is that it can provide peace of mind and financial assistance if you are found liable for accidents caused by your pets. For instance, if your dog bites someone, your liability insurance will likely cover their injuries, provided your insurer doesn't exclude that breed.

Lastly, liability coverage can also be extended to include business income insurance, especially if your income is tied to your apartment. This type of coverage will reimburse you for lost income due to repairs if your apartment becomes unrentable due to smoke, fire, or burst pipes.

In conclusion, apartment insurance policies should include liability coverage to protect yourself from financial losses due to accidents, injuries, property damage, and lawsuits. It is a crucial component of any comprehensive insurance policy for apartment owners.

Social Security and Insurance Settlements: What You Need to Report

You may want to see also

Explore related products

![]()

Apartment owners need landlord insurance, not homeowners insurance

The average cost of homeowners insurance in the U.S. is around $1,754 a year, or $2,110 according to another source. However, this figure can vary depending on several factors, such as location, claims history, coverage limits, and the characteristics of the home. For example, homes in regions prone to severe weather issues like hurricanes and hail tend to have higher insurance rates due to the increased risk of damage. Similarly, homes in coastal areas or near woods and brush may face higher insurance rates as they are more susceptible to natural disasters and wildfires.

While homeowners insurance is essential for protecting your primary residence, apartment owners who rent out their properties require a different type of coverage: landlord insurance. Landlord insurance, also known as rental property insurance, is designed specifically for rental homes inhabited by tenants and includes specialized coverages to address the unique risks associated with renting out a property. These risks can include liability concerns, premises damage, and loss of rental income in the event that the property becomes temporarily uninhabitable.

For instance, if a tenant or their guest gets hurt on the property, landlord insurance can cover your legal fees and any damages if you are found liable for their injuries. It can also provide rental compensation to prevent loss of income while the rental property undergoes repairs or remains vacant. This type of coverage is especially important for apartment owners, as their income is directly tied to the rent collected from tenants.

Additionally, landlord insurance can cover liability for bodily injury or property damage that occurs on the rental property. This includes coverage for medical costs if someone is injured on the property, regardless of fault. This aspect of landlord insurance is crucial, as failing to obtain adequate liability coverage could leave apartment owners vulnerable to costly lawsuits and medical bills.

In conclusion, while homeowners insurance is designed for owner-occupied homes, apartment owners who rent out their properties should opt for landlord insurance. Landlord insurance provides specialized coverage for rental properties, protecting both the landlord's income and their tenants' well-being. By understanding the differences between homeowners insurance and landlord insurance, apartment owners can ensure they have the necessary protection to avoid unexpected expenses and provide a safe and secure environment for their tenants.

Ditech, Assurant, and the Mortgage Insurance Scheme

You may want to see also

Explore related products

$12.08 $15.99

![]()

Homeowners insurance is not a legal requirement

The cost of homeowners insurance for apartments varies depending on several factors. The average cost of homeowners insurance in the U.S. is $2,110 per year or about $176 per month. However, the price can range from $1,090.08 to $3,353.74 per year, depending on factors such as location, claims history, coverage limits, and the characteristics of the home. The type of construction materials used, the coverage selections, and prior claims can also impact the cost of insurance.

While homeowners insurance is important and recommended for financial protection, it is not a legal requirement. States and the federal government do not mandate homeowners to have insurance. However, if you have taken out a mortgage, your lender will typically require you to have homeowners insurance to protect their financial interest in your home. This is because your home is likely your biggest investment, and without insurance, you are financially vulnerable to unexpected events. Disasters can strike at any time, and without insurance, you will be responsible for covering all repair and replacement costs yourself, which can be financially devastating.

Lenders generally ask for proof of homeowners insurance to ensure your property is protected. Standard homeowners insurance covers losses and damage to your property due to unexpected events like fires, theft, or natural disasters. It can also provide liability protection if someone is injured on your property. However, it usually does not cover damage from earthquakes or floods, so additional coverage may be needed depending on your location and specific circumstances.

As a homeowner, you can shop for homeowners insurance separately and choose the provider and plan that suits your needs. This allows you to increase your coverage while only minimally impacting your insurance rate. However, if you do not maintain homeowners insurance, your lender may purchase insurance on your behalf, which may only cover their interests and may be more expensive. Therefore, it is essential to understand your lender's requirements and maintain adequate insurance coverage to protect your financial interests.

Dressing for the Farmers Insurance Open: A Style Guide

You may want to see also

Frequently asked questions

The average cost of homeowners insurance in the U.S. is $2,110 per year or $176 per month. However, the cost of insurance varies depending on location, the size of the house, and the coverage required. A basic policy costs around $300 to $400 per year and covers contents up to a certain amount.

The cost of insurance for an apartment can be influenced by various factors, including the location, the age of the building, and the construction materials used. For instance, coastal properties or homes near woods are often considered riskier to insure due to the possibility of natural disasters or wildfires.

As an apartment owner, you should consider purchasing comprehensive landlord insurance to cover all potential risks, including storm and fire damage, lawsuits, and medical expenses. General liability insurance is crucial to protect against injuries or discrimination claims. Business income insurance (BIC) is also recommended to cover lost income due to repairs or damage to the units.