The cost of medical insurance is a significant expense for both employers and employees. While employer-sponsored health insurance is generally cheaper than individual plans, the cost varies depending on factors such as age, location, smoking status, plan type, and metal tier. In 2022, the average monthly cost of employer-sponsored health insurance was $111 for an individual and $509 for family coverage. However, these costs are expected to rise, with PwC's Health Research Institute projecting a 7% increase in healthcare costs in 2024. To manage expenses, employers may opt for higher-deductible plans or leverage Health Reimbursement Arrangements (HRAs) to reimburse employees for qualified medical expenses. Ultimately, the choice of health insurance plan impacts the monthly premiums paid by employees, with broader coverage and lower deductibles resulting in higher premiums.

| Characteristics | Values |

|---|---|

| Average monthly cost of health insurance | $445 for a single 21-year-old, $467 for a single 27-year-old, $505 for a single 30-year-old, and $1,478 for a 60-year-old. |

| Average annual cost of health insurance | $7,000 for an Affordable Care Act (ACA) marketplace plan. |

| Average annual cost of employer-sponsored health insurance | $6,575 for family coverage and $1,401 for single coverage. |

| Average monthly cost of employer-sponsored health insurance | $111 for an individual policy and $509 for a family policy. |

| Average monthly cost of a marketplace health insurance plan | Under $500. |

| Average monthly premium for an ACA health insurance plan | $590. |

| Average monthly premium for employer-sponsored plans | $114. |

| Average monthly premium for individual plans | $497. |

| Average monthly premium for bronze plans | $495. |

| Average monthly premium for silver plans | $618. |

| Average monthly premium for gold plans | $655. |

| Average monthly premium for platinum plans | $1,166. |

| Average annual health insurance deductible for a bronze plan | $5,774. |

| Average annual health insurance deductible for a silver plan | $4,483. |

| Average annual health insurance deductible for a gold plan | $1,092. |

| Average annual deductible | $2,000. |

Explore related products

What You'll Learn

![]()

Cost-sharing mechanisms

However, this strategy can backfire, as higher levels of cost-sharing have been found to negatively impact prescription drug adherence, which can lead to increased disease complications, hospitalisations, and ultimately, higher healthcare costs. Cost-sharing can also disproportionately affect underserved and underrepresented populations, as well as those with lower health insurance literacy, who may not be able to make informed choices about their healthcare due to a lack of understanding of insurance concepts.

Cost-sharing expenses can vary depending on the type of insurance plan. For example, lower-level plans typically have lower monthly premiums but higher out-of-pocket costs for medical care, while higher-level plans have higher monthly premiums but lower out-of-pocket expenses. The cost of health insurance can also vary depending on factors such as age, location, smoking status, plan type, and metal tier.

To manage the cost of health insurance for employees, employers can consider offering a Group Coverage HRA (GCHRA) or an Integrated HRA to supplement the existing employer-provided health insurance plan. With a GCHRA, employers can offer a monthly allowance to reimburse employees for medical costs, including deductibles, copays, and other medical services. Employees can then choose a plan that meets their individual needs and pay their monthly premiums, with the employer reimbursing them for eligible expenses. Alternatively, employers can opt for a Qualified Small Employer HRA (QSEHRA) or an Individual Coverage HRA (ICHRA) to reimburse employees for qualified medical expenses, including individual health insurance premiums.

Life Events: When Can You Change Your Medical Insurance?

You may want to see also

Explore related products

![]()

Employer-sponsored coverage

The term "employer-sponsored coverage" refers to health insurance obtained through an employer, which is the most common way Americans get insured. It includes insurance for current employees and their families, as well as retired employees. Federal law also gives former employees the right to stay on their employer's health insurance plan, at their own expense, for a period after leaving their job.

Employers with at least 50 full-time employees or equivalents are mandated to provide health coverage to their workers. These employers are called "applicable large employers" or ALEs. Companies that fall under this category and fail to sponsor the required coverage may be penalized. ALEs are required to report the cost of their employees' coverage on W-2 forms. On the other hand, companies with fewer than 50 full-time employees are not obligated to provide coverage, but they may qualify for the Tax Credit for Small Employer Health Insurance Premiums if they opt to do so.

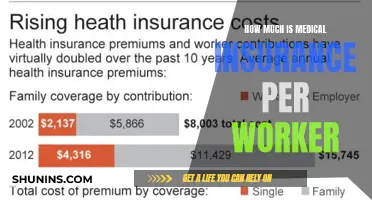

The cost of employer-sponsored health insurance varies. In 2023, group health insurance cost employees $1,401 annually for single coverage and $6,575 for family coverage. On average, employees contributed 17% and 27% toward the total cost of single and family premiums, respectively. These costs are typically paid through payroll deductions on a pre-tax basis. It is worth noting that average premiums tend to increase annually.

There are different types of employer-sponsored health insurance plans. One type is a closed-network plan, where enrollees are generally covered only if they receive care from providers within the plan's network. The other type is an open-network plan, where enrollees have some coverage even if they go outside the network, but they usually face higher costs. Health Maintenance Organization (HMO) and Exclusive Provider Organization (EPO) plans are examples of closed-network plans, while Preferred Provider Organization (PPO) and Point of Service (POS) plans fall under open-network plans.

America's Best Medicaid Insurance Options: What You Need to Know

You may want to see also

Explore related products

![]()

Health insurance costs for different ages

The cost of health insurance varies depending on age, location, tobacco use, and more. Federal guidelines determine how much age can impact your insurance costs. For example, a 64-year-old cannot be charged more than three times as much as someone in their early 20s. This rule applies to most people, but eight states and Washington, D.C., have different rules. New York, Vermont, Alabama, Minnesota, Mississippi, and Oregon do not use age as a factor in calculating health insurance costs.

For those aged 21-24, a full-price health insurance plan costs an average of $486 per month. This is known as the base rate, which is used to calculate costs for other ages. For example, the cost of health insurance for a 40-year-old averages $621 per month, which is 27.8% more than the base rate. Costs start to increase significantly in one's fifties, with rates more than 75% higher than the base rate.

The average premium for an 18-year-old is $396 per month, compared to $781 for a 50-year-old and $1,187 for a 60-year-old. These premiums have increased since 2022, but some populations may be eligible for subsidies if they have low incomes, have retired early, or have scaled back their working hours.

Large employers typically do not use age to set rates, although they are allowed to in some circumstances. Small employers (those with 50 or fewer employees) can use age to rate policies but must follow federal guidelines on charges.

Billing Two Insurances in Colorado: Is It Possible?

You may want to see also

Explore related products

![[8 Pack 4" x 5 Yards] Beige-Self Adhesive Cohesive Bandage Wrap, Self Adherant Non-Woven Wrap Rolls, Atheletic Tape for Wrist, Ankle, Hand, Leg, Premium-Grade Medical Stretch Wrap](https://m.media-amazon.com/images/I/81wGnSXRl8L._AC_UL320_.jpg)

![]()

Health Reimbursement Arrangements (HRAs)

The cost of health insurance varies depending on a variety of factors, including age, smoking status, location, plan type, and metal tier. The average monthly cost of health insurance is $445 for a single 21-year-old, $467 for a single 27-year-old, and $505 for a single 30-year-old. The cost of health insurance also increases with age, with a 60-year-old paying $1,478 per month on average. Group health insurance plans, where the employer helps pay for the plan, often cost less than individual plans. The average monthly premium for employer-sponsored plans is $114, while the average for individual plans is $497.

There are different types of HRAs available, including the Qualified Small Employer HRA (QSEHRA) and the Individual Coverage HRA (ICHRA). The QSEHRA is designed for small businesses with fewer than 50 full-time equivalent employees, while the ICHRA is available to employers of any size. Additionally, employers can offer a Group Coverage HRA (GCHRA) or an integrated HRA to supplement an existing employer-provided health insurance plan. With a GCHRA, employees can purchase their own health insurance plan and be reimbursed for eligible expenses up to their allowance balance.

HRAs provide flexibility for both employees and employers. Employees can use individual coverage HRAs to reimburse premiums for individual health insurance plans, promoting choice and customization. Employers can use HRAs to better control the cost of health benefits, especially if offering a traditional group health plan is not feasible. However, it is important to note that HRAs might not be the best option for every employer, and there may be other factors to consider, such as eligibility for premium tax credits.

Medicare Supplemental Plans: Are Prescriptions Covered?

You may want to see also

Explore related products

![]()

Additional benefits

The cost of workplace medical insurance depends on a variety of factors, including the insurance company, the plan type, the network of providers, plan features, location, contribution amount, and employee demographics. While it is one of the most expensive benefits, it is also the most sought-after by employees.

When it comes to additional benefits, employers can offer extra perks like dental, vision, or mental health coverage. These benefits can be included in the health insurance plan or offered separately. Dental coverage typically includes regular check-ups, cleanings, and treatments, while vision coverage can provide discounts on eye exams, glasses, and contacts. Mental health coverage can include access to counselling services, therapy, and other mental health resources.

Some companies also choose to offer wellness programs that promote healthy habits and proactive health initiatives. These programs can include workplace exercise programs, gym discounts, and incentives for regular visits to primary care providers. By encouraging employees to take care of their physical and mental health, companies can contribute to a healthier and more productive workforce, potentially reducing the number of health insurance claims over time.

Another option for additional benefits is to provide Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). These accounts allow employees to save money tax-free for future medical expenses, and they can be paired with certain high-deductible insurance plans. With an HSA, employees can carry over any unused funds from year to year, providing a long-term savings option. On the other hand, FSAs are typically used for more immediate expenses, as the funds do not roll over.

Furthermore, companies can explore Individual Coverage Health Reimbursement Arrangements (ICHRAs) or Qualified Small Employer Health Reimbursement Arrangements (QSEHRAs). These arrangements allow employers to reimburse employees for medical expenses, including health insurance premiums and out-of-pocket costs, with certain limits and tax advantages. This gives employees more control over their healthcare choices while still providing financial support.

By offering a range of additional benefits, companies can create a comprehensive and attractive benefits package that meets the diverse needs of their employees. These benefits not only support the physical and mental well-being of employees but also provide financial peace of mind, contributing to a positive and productive work environment.

State Farm Life Insurance: Medical Exam Needed?

You may want to see also

Frequently asked questions

The cost of medical insurance varies depending on factors such as the type of plan, the number of people covered, and the location. In 2022, the average monthly cost of an employer-sponsored health insurance policy was $111 for an individual and $509 for a family.

The cost of workplace medical insurance is influenced by the size of the company, the demographics of the employees, and the chosen plan's specifics. For example, older employees may have higher medical costs, and plans with broader networks of doctors and hospitals tend to have higher premiums.

Employers typically offer a range of group health insurance plans, from comprehensive plans with low deductibles to high-deductible plans. Employees who opt for lower-deductible plans will generally pay higher premiums, while those who choose high-deductible plans will pay lower premiums but higher out-of-pocket costs. Employers often pay a larger share of the premium, making it cheaper for employees to get insurance through their workplace.

![Chucks® Premium Disposable Underpads 30”x36” Ultra Thick Super Absorbent Chux Incontinence Bed Pads Disposable Adult with Adhesive Tape, Extra Large Pee Pads, Pet Training Pads 30x36 [25-Pack]](https://m.media-amazon.com/images/I/81ihMoZ7+CL._AC_UL320_.jpg)