The cost of homeowners insurance is a crucial consideration for anyone looking to purchase a property. Various factors influence the price of insurance, and it is essential to understand these elements to make an informed decision. From location and construction materials to claims history and coverage limits, the cost of insuring a home can vary significantly. This article will explore the key considerations for homeowners and provide insights into calculating the appropriate level of coverage to ensure adequate protection without incurring excessive expenses.

| Characteristics | Values |

|---|---|

| Average cost of homeowners insurance in the U.S. | $2,110 per year for $300,000 worth of dwelling coverage |

| Average cost of homeowners insurance as per National Association of Realtors | $2,377 per year |

| Average cost of homeowners insurance as per Progressive | $1,090.08 to $3,353.74 per year |

| Average cost of homeowners insurance as per Forbes | $1,678 per year for $350,000 in dwelling coverage, $175,000 for personal property coverage and $100,000 in liability coverage |

| Factors that affect the insurance rates | Location, claims history, coverage limits, home characteristics, construction materials, age of the home, home condition, home size, liability concerns, credit history, etc. |

Explore related products

What You'll Learn

- Home insurance rates vary by region, even by ZIP code

- The size of your home: Larger homes have higher rates

- The age of your home: Older homes are more expensive to insure

- The condition of your home: Carriers inspect homes before insuring

- The amount of dwelling coverage: The main factor determining how much you pay

![]()

Home insurance rates vary by region, even by ZIP code

Home insurance rates vary by region, and even by ZIP code. The average cost of homeowners insurance in the U.S. is about $2,110 a year for $300,000 worth of dwelling coverage, but rates differ by state. The national average cost of homeowners insurance is $1,678 per year, according to one analysis. This estimate is for a policy with $350,000 in dwelling coverage, $175,000 for personal property coverage, and $100,000 in liability coverage.

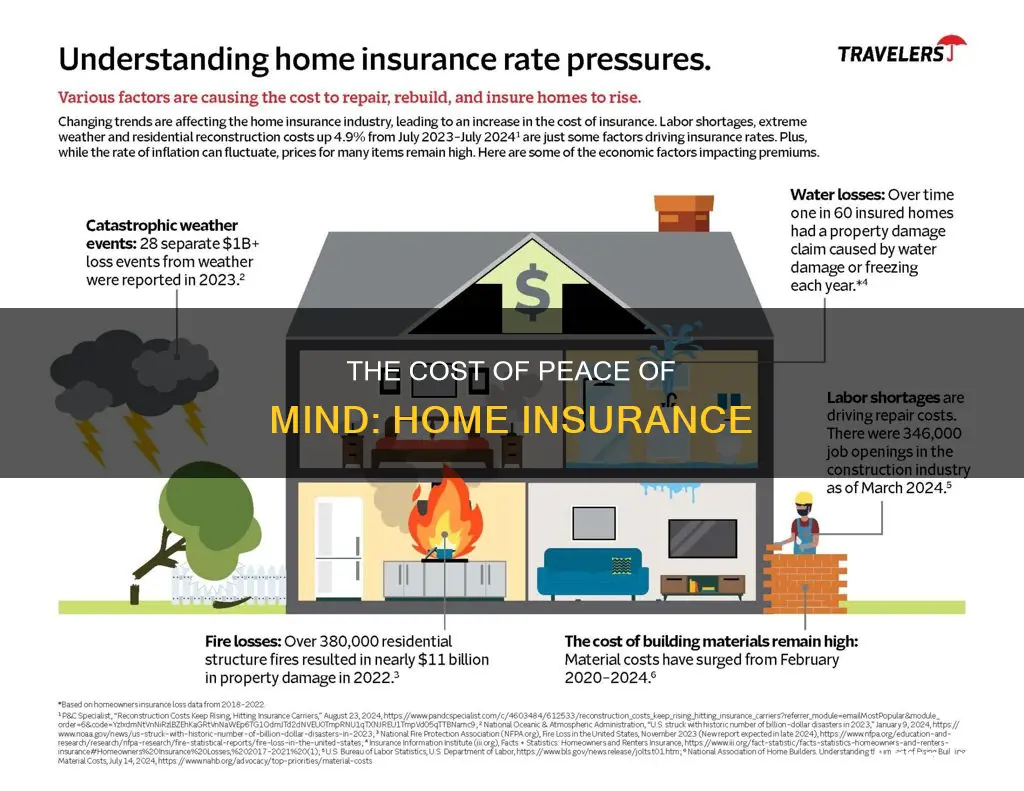

The cost of home insurance is influenced by the impact of inflation on previous losses, the elevated cost of building materials, and the high likelihood of future extreme weather-related losses. The age of your home, its location, and its characteristics are also factors that determine the cost of home insurance. For instance, homes in areas prone to severe weather issues like tornadoes, hurricanes, and hail will likely pay more for homeowners insurance. Similarly, homes near woods and brush are susceptible to damage from wildfires and are therefore more expensive to insure.

The size of your home is another factor that influences the cost of insurance. Larger homes have higher insurance rates because there is more "surface area" that can be damaged or destroyed during a covered event, leading to higher repair and rebuilding costs. The age of your home is also considered when determining your premium. Older homes might be more expensive to build back after a loss, especially if you need to bring them up to modern safety and building codes. The type of construction and materials used to build your home can also increase the cost of your homeowners insurance. For example, concrete block homes may cost less to insure than wood frame houses because they are less susceptible to fires and strong winds.

The amount of dwelling coverage, or Coverage A, on your policy is the main factor that determines how much you pay for homeowners insurance. The more coverage you want or need, the higher your premiums will likely be. The size of your deductible also affects your premium. When your deductible is higher, your premiums will typically be lower, and vice versa.

Mortgage Insurance Rates: What You Need to Know

You may want to see also

Explore related products

![]()

The size of your home: Larger homes have higher rates

The average cost of homeowners insurance in the U.S. is about $2,110 a year for $300,000 worth of dwelling coverage. However, rates can vary depending on various factors, with the location of your home being one of the greatest factors impacting the cost. For instance, homes located in areas prone to extreme weather, flooding, wildfires, or crime will be more expensive to insure than homes in less risky areas.

Another critical factor that influences the cost of homeowners insurance is the size of your home. Larger homes have higher insurance rates because they have more surface area that can be damaged or destroyed during a covered event, leading to higher repair and rebuilding costs. To estimate the amount of insurance you need, you can multiply the total square footage of your home by the local per-square-foot building costs. It's important to note that the land is not factored into rebuilding estimates.

The construction type and materials used to build your home also play a role in determining the cost of insurance. Homes with more square footage typically cost more to rebuild, and certain construction types and materials are more expensive or prone to specific risks. For example, a wood-frame house may cost more to insure than a concrete block home because it is more susceptible to fires and strong winds.

Additionally, the age of your home can impact insurance rates. Older homes often cost more to insure because their electrical, plumbing, and heating systems may be more prone to issues and may need updating. They may also require specialized materials or workmanship for repairs, which can drive up costs.

Other factors that can influence homeowners insurance rates include your history of claims, credit score, marital status, and the presence of high-risk features such as swimming pools or certain types of roofing. Conducting a home inspection and regularly reviewing and updating your coverage can help you understand your insurance needs and potentially lower your rates.

Seattle Home Insurance: What's the Real Cost?

You may want to see also

Explore related products

![]()

The age of your home: Older homes are more expensive to insure

The cost of homeowners' insurance depends on a variety of factors, including location, construction materials, coverage selections, and prior claims. The average cost of homeowners insurance in the US is about $2,110 a year for $300,000 worth of dwelling coverage, but rates vary by state. The age of your home is one of the factors that can affect the cost of homeowners insurance.

Older homes are typically more expensive to insure than newer homes. Some insurers consider homes built more than 40 years ago as older properties. There are several reasons why older homes may be more costly to insure:

- Higher risk: Older homes are considered higher risk by insurance companies due to potential wear and tear, fragile structures, and outdated construction materials.

- Outdated materials and features: Older homes often contain obsolete building materials and ornate features that are specific to the time period in which they were built. These materials and features may be more expensive and less flexible than modern alternatives. For example, plaster walls, stucco, and custom architectural details are common in pre-war homes and can be costly to replace.

- Cost of labour: The specialised nature of renovating or repairing older homes may require skilled contractors in period architecture, who may charge higher rates than those working on modern homes.

- Outdated plumbing and roofing: Older plumbing systems may be more susceptible to leaks, blockages, and burst pipes. Similarly, older roofs may be less likely to withstand damage, leading to potential claims.

- Higher rebuilding costs: The cost of rebuilding an older home can be higher than its market value, especially if rare or handmade materials were used that are no longer easily available or up to current building codes.

If you own an older home, you may need to purchase specialised coverage, such as an HO-8 policy, which is designed for older homes and covers certain perils and dwelling coverage limits. You can also consider adding extended replacement cost coverage or guaranteed replacement cost coverage to ensure adequate protection for your older home.

Homeowners Insurance: Faulty Gutters Covered?

You may want to see also

Explore related products

![]()

The condition of your home: Carriers inspect homes before insuring

The cost of homeowners insurance depends on a variety of factors, including location, construction materials, coverage selections, and prior claims. The average cost of homeowners insurance in the US is about $2,110 per year for $300,000 worth of dwelling coverage, but rates vary by state.

Home insurance inspections are not always necessary but are becoming more common as part of the underwriting process. Carriers inspect homes to determine the full risk of insuring the property and to set accurate premiums and coverage limits. They will examine the condition of the home's frame, interior, exterior structures, walls, ceilings, floors, plumbing, HVAC, electrical systems, and more. This helps them identify significant risks, such as pest infestations, that would not be covered by standard insurance policies.

During an inspection, an inspector will typically check the following:

- Roof: The age, condition, and material of the roof are important factors in determining the risk of insuring a home. Asphalt shingles, for example, are less flammable and may result in lower insurance costs than a cedar or wood-shake roof.

- Exterior: The inspector will examine the windows, doors, chimney, and foundation for any signs of damage or wear.

- Interior: In addition to the walls, ceilings, and floors, the inspector will check the plumbing, HVAC, and electrical systems to ensure they are up to date and in good condition.

It is important to note that consenting to occasional inspections is typically a basic condition of maintaining a home insurance policy. Homeowners should be prepared for inspections and address any issues that may impact their coverage.

QuickBooks Mortgage Insurance: Where to Enter It?

You may want to see also

Explore related products

$8

![]()

The amount of dwelling coverage: The main factor determining how much you pay

The amount of dwelling coverage is the main factor in determining how much you pay for homeowners insurance. This is because, in the event of a total loss, your insurance company will pay to rebuild or repair your house, so the cost of your insurance will be directly related to the cost of rebuilding your home.

The price you paid for your home, or its current market value, may be more or less than the cost to rebuild it. This is because the cost of rebuilding includes the cost of construction materials and labour, which can be influenced by inflation and may increase suddenly after a major catastrophe such as a hurricane, tornado, or wildfire.

To get an estimate of how much insurance you need, you can multiply the total square footage of your home by the local per-square-foot building costs. You can find out the construction costs in your community by contacting your local real estate agent, builders association, or insurance agent. You can also use online home insurance calculators to estimate the coverage you need.

It's important to note that the amount of dwelling coverage you choose will impact your monthly premiums. The more coverage you want or need, the higher your premiums will likely be. Therefore, when deciding on the amount of dwelling coverage, you need to find a balance between having enough coverage to feel secure and not paying more than you need to.

Short-Term Disability Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

The national average cost of homeowners insurance is $1,678 per year, according to Forbes Advisor's analysis. This estimate is for a policy with $350,000 in dwelling coverage, $175,000 for personal property coverage, and $100,000 in liability coverage. However, rates vary significantly from one insurance company to another and by state.

Most homeowners insurance policies provide coverage for your belongings at about 50% to 70% of the insurance on your dwelling. To determine how much coverage you need, it is advisable to conduct a home inventory, which will help you assess the value of your belongings.

The location of your home is one of the most significant factors influencing the cost of insurance. Homes located in areas prone to extreme weather, flooding, wildfires, or high crime rates are more expensive to insure. Additionally, homes in coastal regions may be riskier to insure due to the possibility of natural disasters.

The age, size, and condition of your home can affect the cost. Older and larger homes tend to have higher insurance rates due to increased risks and potential repair costs. The construction materials used, improvements made, and features such as swimming pools or playground equipment can also influence the cost of insurance.