Florida's insurance market is in its best financial shape in almost a decade, according to industry analysts. However, homeowners in North Florida are still facing higher premiums than in previous years. In this context, how much has homeowners' insurance increased in St. Johns, Florida?

| Characteristics | Values |

|---|---|

| Average cost of homeowners insurance in Florida | $2,625 per year or $219 per month |

| Average cost of homeowners insurance in Miami, Florida | $5,095 per year |

| Average cost of homeowners insurance in Orlando, Florida | $2,510 per year |

| Average cost of homeowners insurance in St. Johns County, Florida | Varies depending on the company and the customer |

| Example quote from Brightway Insurance | $4,400 for $350,000 coverage and $11,000 deductible |

| Example quote from Robin Wilson Insurance Services | $4,840 for $390,000 coverage and $5,800 deductible |

| Example quote from Herbie Wiles Insurance | $7,940 for $620,000 coverage and $3,600 deductible |

| Property insurance premium increase in Duval, Clay, St. Johns, and Nassau counties from 2023 to 2024 | 13.5% |

Explore related products

What You'll Learn

![]()

St. Johns Insurance Company's transition to Slide Insurance

St. Johns Insurance Company was a property and casualty insurance company located in Orlando, Florida. The company was licensed in Florida in 2004 and had approximately 147,000 in-force policies at the time of receivership. On February 25, 2022, St. Johns Insurance Company was ordered into receivership for liquidation by the Second Judicial Circuit Court in Leon County, Florida.

The Florida Department of Financial Services is the court-appointed receiver of St. Johns Insurance Company. The Department has entered into an agreement with Slide Insurance Company ("Slide") to transition policies and provide policyholders with continued insurance coverage. The transition plan, approved by the Receivership Court, cancels St. Johns policies and provides replacement coverage from Slide, effective March 1, 2022, at 12:01 a.m. There will be no gaps in coverage, and policyholders' coverage and premiums will remain identical.

Slide, a Tampa-based insurtech startup, has assumed St. John's homeowners' policies, offering the same coverage for the same premium. Slide was founded by Bruce Lucas, the founder of Heritage Insurance, and has received support from the Florida Association of Insurance Agents. The company has a Financial Stability Rating of "A" (Exceptional) from Demotech.

During the transition, the Florida Insurance Guaranty Association ("FIGA") and the South Carolina Property and Casualty Insurance Guaranty Association ("SCPCIGA") will help pay outstanding claims for St. Johns' policies, which may cause slight delays in claim processing. Any unearned premium due back from St. Johns will be sent to Slide and applied to the Slide transition policy, and policyholders are not required to submit Proof of Claim forms.

St. Johns policyholders will continue to have their St. Johns Agent as a point of contact for coverage questions and servicing needs. When a replacement policy expires, eligible policyholders will receive a renewal offer for a twelve-month Slide policy, which may have different terms, coverage, and premiums. Slide coverage will begin immediately after the cancellation of the St. Johns policy and continue through the expiration of the current policy term, maintaining the same terms, conditions, and rates.

Navigating the Challenges of Homeowner Insurance

You may want to see also

Explore related products

![]()

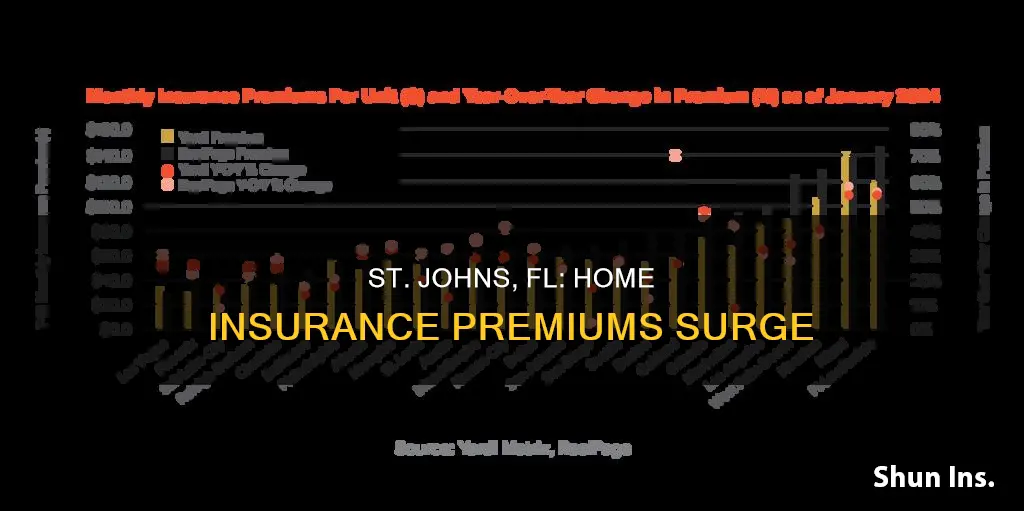

Rising property insurance premiums in North Florida

Despite Florida's insurance market being in its best financial shape in almost a decade, homeowners in North Florida are facing higher premiums compared to the previous year. In Duval, Clay, St. Johns, and Nassau counties, property insurance premiums rose by an average of 13.5% from 2023 to 2024.

The reasons for the surge in insurance premiums are varied. Firstly, the state of Florida is particularly susceptible to hurricanes and flooding, which are costly for insurance companies. Secondly, the population of Florida has increased by about 3% in the last few years, while the number of homes in the state has grown by double digits. This increased demand for housing, coupled with the state's vulnerability to natural disasters, has resulted in higher premiums.

Additionally, the cost of goods and services in Florida has risen by about 8% in recent years, contributing to the overall increase in insurance premiums. The average premium in the state reached $3,023 in 2025, a 34% increase from the last quarter of 2022.

The impact of these rising premiums is felt differently across the state. Coastal counties like Miami-Dade tend to have higher rates than inland counties. For example, Miami-Dade policies soared over 300%, while Jacksonville, somewhat protected by its geography, still saw a 226% increase.

To combat these rising costs, Florida Senator Rick Scott has proposed legislation to provide homeowners with a tax deduction of up to $10,000 on their yearly premiums, called the Homeowners Premium Tax Reduction Act. In the meantime, homeowners are encouraged to stay informed about legislation that may affect their rights and rates and to consider umbrella policies or higher deductibles to lower their premiums.

Principle Mortgage Insurance: What You Need to Know

You may want to see also

Explore related products

$9.69 $12.49

![]()

Florida's insurance market financial health

Florida's insurance market is in its best financial shape in almost a decade, according to industry analysts. However, homeowners in North Florida are facing higher premiums than the previous year. In Duval, Clay, St. Johns, and Nassau counties, property insurance premiums rose by an average of 13.5% from 2023 to 2024. This increase is attributed to insurance companies reducing their exposure to losses and passing on their increased costs to consumers.

The Florida homeowner's insurance market is considered a "hard" market, characterised by rising prices and decreasing product availability. This situation is partly due to the potential for increased tropical storm activity and the mounting cost of claims. As a result, insurance companies are more selective about the coverage they offer, and obtaining new or replacement coverage has become challenging.

The year a home was built, its location, and its wind mitigation features are significant factors influencing insurance rates and insurability in Florida. Homes built after the updated Florida Building Code in 2002 and 2008 are designed with stronger requirements to protect against wind-related damage, which can impact insurance costs.

To navigate the complexities of the Florida insurance market, homeowners can seek advice from insurance brokers specialising in Florida homeowner's insurance. These brokers can provide insights into carrier financial ratings and coverage options, ensuring that homeowners have the necessary information to make informed decisions about their coverage and pricing.

While the overall financial health of Florida's insurance market is positive, the impact on consumers, especially in North Florida, is noticeable through higher premiums and reduced coverage options.

Builders Risk vs. Homeowners Insurance: What's the Difference?

You may want to see also

Explore related products

$9.59 $16.99

![]()

Homeowners' tax deduction on yearly premiums

St. Johns Insurance Company, Inc. was liquidated, and its policies were transitioned to Slide Insurance Company with no gaps in coverage. The transition plan was approved by the Receivership Court, and St. John's policies were cancelled on March 1, 2022, at 12:01 a.m.

In August 2024, Florida Senator Rick Scott proposed legislation to provide a tax deduction on yearly homeowners' insurance premiums. The proposed legislation is called the Homeowners Premium Tax Reduction Act and would provide an above-the-line tax deduction of up to $10,000 at primary residences. This comes as data shows that homeowners in North Florida, including St. Johns County, are facing higher property insurance premiums than the previous year, with an average increase of 13.5% from 2023 to 2024.

While the proposed legislation would provide some relief to Florida homeowners facing rising insurance costs, it is worth noting that there are currently other tax benefits available to Florida homeowners. These include the Florida Homestead Exemption, which can decrease the taxable value of a primary residence by up to $50,000, resulting in lower real estate taxes. Additionally, Florida homeowners may be eligible for deductions on mortgage interest and tax credits if they have received a qualified Mortgage Credit Certificate (MCC) from their state or local government.

Florida homeowners affected by hurricanes may also qualify for special tax relief programs, including extended federal tax filing deadlines. It is recommended to consult a tax professional to understand the specific deductions and benefits applicable to an individual's circumstances.

Vacation Rentals: Are You Covered by Home Insurance?

You may want to see also

Explore related products

![]()

Home insurance rates in Florida

The prevalence of lawsuits within the state has also played a significant role in increasing insurance rates. Despite accounting for only 9% of the nation's homeowners insurance claims, Florida was responsible for 79% of all lawsuits filed against insurance companies nationwide in 2022. This disproportionate level of litigation has resulted in increased legal expenses for insurers, who have, in turn, passed these costs on to homeowners through higher premiums. Recognizing the issue, Florida lawmakers have enacted legislation aimed at curbing lawsuit abuse and stabilizing insurance rates.

The location of a property within Florida also influences insurance rates, with coastal areas like Miami and Fort Lauderdale facing higher premiums due to their increased risk of hurricane damage. For example, the average annual insurance cost in Miami is $5,315, while inland areas like Ocala have lower rates, with an average of $1,865 per year. Additionally, an individual's credit score can impact their insurance rates, with Floridians with poor credit paying an average of $3,855 per year, 47% more than those with good credit.

The rising insurance costs in Florida reflect the growing challenges posed by climate change and the state's vulnerability to extreme weather events. The combination of frequent hurricanes, rising litigation costs, and heavy claims has led to a reduction in insurance options for homeowners. The situation has improved slightly, with the insurance market showing positive signs of recovery, but homeowners in North Florida continue to face higher premiums than the previous year.

Homeowners Insurance: Sump Pump Failure Covered?

You may want to see also

Frequently asked questions

The average cost of homeowners insurance in Florida is $2,625 per year, or about $219 per month. However, the cost of insurance varies depending on the county and individual circumstances.

The cost of homeowners insurance in St. Johns, Florida, is influenced by factors such as the insured person's age, income, credit score, number of pets, and smoking status.

In St. Johns County, property insurance premiums rose by an average of 13.5% from 2023 to 2024.

Natural disasters, such as hurricanes and tropical storms, have contributed to the increase in homeowners insurance rates in St. Johns, Florida. Standard policies may not fully cover wind and water damage caused by these events.

Citizens is a government entity that serves as an "insurer of last resort" for eligible homeowners in Florida who cannot obtain coverage from standard insurers. Residents may qualify for Citizens insurance if they cannot find a standard insurer or if the premiums offered by other insurers are more than 20% higher than the Citizens rate.