Health insurance is a critical aspect of financial planning, offering protection against the high costs of medical care. The amount one pays for health insurance varies widely depending on factors such as age, location, coverage level, and provider. Premiums can range from a few hundred to several thousand dollars annually, with additional costs like deductibles, copayments, and coinsurance further influencing overall expenses. Understanding these variables is essential for individuals and families to choose a plan that balances affordability with comprehensive coverage, ensuring access to necessary healthcare without undue financial strain.

Explore related products

What You'll Learn

- Average Monthly Premiums: National and state-specific costs for individual and family plans

- Factors Affecting Costs: Age, location, coverage level, and provider impact on premiums

- Types of Plans: HMO, PPO, EPO, and HDHP differences in pricing and benefits

- Subsidies and Assistance: ACA subsidies, Medicaid, and employer contributions to reduce costs

- Out-of-Pocket Expenses: Deductibles, copays, and coinsurance beyond monthly premiums

![]()

Average Monthly Premiums: National and state-specific costs for individual and family plans

The average monthly premium for health insurance in the United States varies significantly depending on whether you’re purchasing an individual or family plan, as well as your location. Nationally, as of recent data, the average monthly premium for an individual plan hovers around $456, while family plans average approximately $1,218. These figures, however, are just starting points. Factors such as age, income, and the level of coverage (bronze, silver, gold, or platinum) play a critical role in determining your actual cost. For instance, a 40-year-old nonsmoker might pay around $480 monthly for a mid-tier silver plan, while a family of four could face premiums exceeding $1,500 for similar coverage.

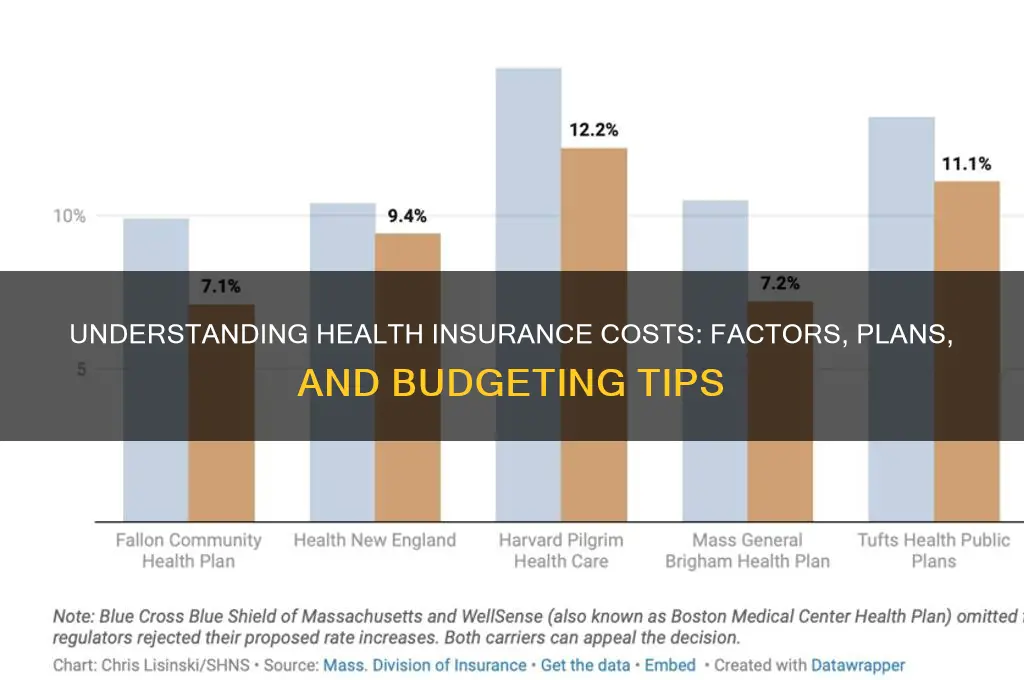

State-specific costs reveal even greater disparities, driven by differences in healthcare regulations, provider networks, and cost of living. In states like Wyoming or West Virginia, premiums tend to be higher, with individual plans averaging over $600 monthly due to limited competition among insurers. Conversely, states like Minnesota or Massachusetts often see lower averages, around $350 for individuals, thanks to robust state-run marketplaces and subsidies. For families, the gap widens: in California, a family plan might cost $1,300 monthly, whereas in Alabama, it could surpass $1,800. These variations underscore the importance of researching your state’s specific market dynamics.

To navigate these costs effectively, consider leveraging subsidies through the Affordable Care Act (ACA) if your income qualifies. For example, a single adult earning up to $54,360 annually (or a family of four earning up to $111,000) may be eligible for premium tax credits that reduce monthly payments. Additionally, choosing a plan with a higher deductible can lower your premium, but ensure you have savings to cover out-of-pocket costs if needed. For families, compare the cost of a single family plan versus individual plans for each member—sometimes, separate policies are more affordable.

A practical tip for cost-conscious consumers: use state or federal health insurance marketplaces to compare plans side by side. These platforms provide transparent pricing and highlight available subsidies. For instance, a 30-year-old in Colorado might find a bronze plan for $300 monthly, while a gold plan could cost $600 but offer lower copays and deductibles. Families should also explore Health Savings Accounts (HSAs) paired with high-deductible plans to offset expenses tax-free.

In conclusion, understanding average monthly premiums requires a tailored approach. While national averages provide a baseline, state-specific costs and individual circumstances dictate the final price. By researching subsidies, comparing plan types, and considering your healthcare needs, you can find a balance between affordability and coverage. Whether you’re an individual or part of a family, proactive planning ensures you’re not overpaying for health insurance.

Transportation Coverage: Medical Insurance Options

You may want to see also

Explore related products

![]()

Factors Affecting Costs: Age, location, coverage level, and provider impact on premiums

Health insurance premiums are not one-size-fits-all. A 25-year-old in rural Nebraska will pay significantly less than a 55-year-old in Manhattan, even for similar coverage. Age is a primary driver of costs, with older individuals facing higher premiums due to increased health risks and utilization. For instance, a healthy 30-year-old might pay $200–$400 monthly for a mid-tier plan, while someone in their 60s could see premiums double or triple, reaching $800–$1,200, depending on location and provider.

Location plays a pivotal role, too. Urban areas with higher living costs and denser populations often have more expensive healthcare services, translating to pricier premiums. For example, a Silver-level plan in Texas might cost $350 monthly, while the same coverage in California could exceed $600. Rural areas may offer lower premiums but limit provider networks, forcing policyholders to travel for specialized care. Proximity to top-tier hospitals or areas with high healthcare demand can inflate costs further.

Coverage level is another critical factor. A Bronze plan, with 60% coverage and a $6,000 deductible, may cost $250–$350 monthly but leaves you paying more out-of-pocket for services. In contrast, a Platinum plan, covering 90% of costs with a $1,000 deductible, could cost $700–$1,000 monthly. The trade-off? Lower premiums mean higher risk for unexpected medical expenses, while higher premiums offer financial predictability.

Finally, the provider you choose can dramatically alter costs. Non-profit insurers often offer lower premiums than for-profit companies, but their networks may be smaller. For instance, a plan with a national provider like Blue Cross Blue Shield might cost $400 monthly, while a regional insurer could offer the same coverage for $300. Shopping around and comparing provider reputations, network sizes, and customer satisfaction ratings can save hundreds annually.

To navigate these factors, start by assessing your health needs and budget. If you’re young and healthy, a high-deductible Bronze plan might suffice. If you’re older or have chronic conditions, a Gold or Platinum plan could provide better value. Use state or federal marketplaces to compare plans side-by-side, and don’t overlook subsidies or employer contributions, which can significantly reduce costs. Understanding these variables empowers you to make informed decisions, ensuring you get the coverage you need without overpaying.

Ohio Medical Insurance: Free Coverage Options Explained

You may want to see also

Explore related products

![]()

Types of Plans: HMO, PPO, EPO, and HDHP differences in pricing and benefits

Health insurance costs vary widely based on plan type, with HMO, PPO, EPO, and HDHP options offering distinct pricing structures and benefits. Understanding these differences is crucial for selecting a plan that aligns with your healthcare needs and budget. Let’s break down each type to clarify their unique features.

HMO (Health Maintenance Organization) plans are typically the most cost-effective option, with lower monthly premiums and out-of-pocket costs. They require you to choose a primary care physician (PCP) who coordinates all your care and provides referrals to specialists within the network. For example, a 30-year-old individual might pay $200–$300 monthly for an HMO plan, with a $20 copay for primary care visits. The trade-off? Limited flexibility—care outside the network is rarely covered, except in emergencies. This plan suits those who prioritize affordability and are comfortable with a structured healthcare approach.

PPO (Preferred Provider Organization) plans offer greater flexibility but at a higher cost. Monthly premiums can range from $400 to $600 for the same age group, with higher deductibles and copays. For instance, a specialist visit might cost $50 instead of $20. The advantage is the ability to see out-of-network providers, though at a significantly higher cost. PPOs are ideal for individuals who value choice and are willing to pay more for it. A practical tip: if you frequently travel or prefer specific specialists, a PPO might outweigh the extra expense.

EPO (Exclusive Provider Organization) plans combine elements of HMO and PPO plans. They offer lower premiums than PPOs (around $300–$400 monthly) but restrict care to in-network providers, similar to HMOs. The key difference? No referrals are needed to see specialists. This plan is a middle ground for those who want lower costs without the hassle of referrals. However, out-of-network care is not covered, so it’s essential to ensure your preferred providers are included.

HDHP (High Deductible Health Plan) plans pair with Health Savings Accounts (HSAs) and are designed for those who want to save on premiums while planning for future healthcare expenses. Monthly premiums are low—often $150–$250—but deductibles are high, typically $1,500–$3,000 for individuals. For example, you’ll pay full price for most services until the deductible is met, after which coinsurance applies. HDHPs are best for healthy individuals or families who rarely need medical care. A practical tip: contribute to your HSA to cover out-of-pocket costs tax-free and build a healthcare safety net.

In summary, HMOs offer affordability with restrictions, PPOs provide flexibility at a premium, EPOs balance cost and convenience, and HDHPs cater to those willing to trade immediate savings for higher risk. Analyze your healthcare usage, budget, and preferences to choose the plan that best fits your needs.

Denied Benefits? Understanding Why Insurance Companies Reject Claims

You may want to see also

Explore related products

![]()

Subsidies and Assistance: ACA subsidies, Medicaid, and employer contributions to reduce costs

Health insurance costs can be daunting, but subsidies and assistance programs significantly reduce the financial burden for millions of Americans. The Affordable Care Act (ACA) introduced premium tax credits, which lower monthly premiums for individuals and families earning between 100% and 400% of the federal poverty level (FPL). For example, a family of four earning up to $111,000 annually in 2023 may qualify. These credits are applied directly to your monthly premium, making coverage more affordable. To determine eligibility, use the Health Insurance Marketplace’s online calculator, which factors in income, household size, and location.

Medicaid serves as another critical safety net, offering free or low-cost coverage to low-income individuals and families. Eligibility varies by state but generally includes adults earning up to 138% of the FPL, pregnant women, children, and people with disabilities. For instance, in states that expanded Medicaid, a single adult earning up to $18,754 annually in 2023 could qualify. Unlike ACA subsidies, Medicaid covers additional services like long-term care and transportation to medical appointments, providing comprehensive support for vulnerable populations.

Employer-sponsored health insurance remains the most common coverage source, with over 150 million Americans benefiting from this arrangement. Employers typically cover 70-80% of premium costs, significantly reducing out-of-pocket expenses for employees. For example, a family plan that costs $22,000 annually might only require the employee to pay $4,400-$6,600. To maximize this benefit, enroll during your company’s open enrollment period and consider contributing to a Health Savings Account (HSA) if available, as it offers tax advantages for medical expenses.

While these programs are invaluable, navigating them requires attention to detail. ACA subsidies depend on accurate income reporting—underestimating could lead to repaying credits at tax time, while overestimating might result in smaller subsidies than you qualify for. Medicaid eligibility redeterminations occur annually, so keep your contact information updated with your state agency to avoid coverage gaps. For employer plans, review your Summary of Benefits and Coverage (SBC) to understand copays, deductibles, and out-of-network costs. By leveraging these subsidies and assistance programs strategically, you can make health insurance more manageable and accessible.

Medical Insurance Billing: Your Questions Answered

You may want to see also

Explore related products

$9.98 $12.99

![]()

Out-of-Pocket Expenses: Deductibles, copays, and coinsurance beyond monthly premiums

Health insurance isn’t just about monthly premiums. Beyond that recurring cost lies a complex web of out-of-pocket expenses—deductibles, copays, and coinsurance—that can significantly impact your wallet. Understanding these terms is crucial, as they dictate how much you’ll pay when you actually use your insurance. For instance, a deductible is the amount you must pay out of pocket before your insurance kicks in, while copays and coinsurance determine your share of costs for services like doctor visits or hospital stays. Ignoring these details can lead to unexpected financial strain, even with a seemingly affordable premium.

Consider this scenario: You have a health plan with a $2,000 deductible, a $30 copay for primary care visits, and 20% coinsurance for hospital stays. If you break your arm and require a $10,000 hospital visit, you’ll first pay the $2,000 deductible. After that, your 20% coinsurance means you’ll owe $1,600 ($10,000 - $2,000 = $8,000, then 20% of $8,000). Add in a few doctor follow-ups at $30 each, and your total out-of-pocket cost could easily surpass $3,700—far beyond your monthly premiums. This example underscores why scrutinizing these expenses is as vital as comparing premiums.

To navigate these costs effectively, start by reviewing your plan’s Summary of Benefits and Coverage (SBC). This document breaks down deductibles, copays, and coinsurance for various services. For families or individuals with chronic conditions, consider plans with lower deductibles and higher premiums, as they minimize out-of-pocket costs over time. Conversely, healthy individuals might opt for high-deductible plans paired with Health Savings Accounts (HSAs) to save on taxes and cover future expenses. Pro tip: Use online calculators to estimate annual costs based on your expected healthcare usage.

A common misconception is that copays are the only expense for routine care. While a $20 copay for a checkup seems straightforward, some plans apply deductibles to specialist visits or lab tests, meaning you’ll pay full price until your deductible is met. Coinsurance, too, can be deceptive—a 30% share of a $50,000 surgery translates to $15,000 out of pocket. To avoid surprises, ask your insurer for cost estimates before major procedures and verify which services are subject to deductibles versus copays.

Finally, don’t overlook out-of-pocket maximums—the most you’ll pay annually for covered services. Once you hit this limit, your insurer covers 100% of costs. For 2023, individual maximums range from $8,000 to $9,000, depending on the plan. While this cap offers financial protection, it doesn’t include premiums or non-covered services. By strategically planning around deductibles, copays, and coinsurance, you can maximize your insurance value and minimize unexpected expenses. Knowledge here isn’t just power—it’s savings.

Why Insurance Companies Refuse Settlements in Medical Malpractice Claims

You may want to see also

Frequently asked questions

The average cost of health insurance varies widely based on factors like location, age, coverage level, and provider. In the U.S., the average monthly premium for an individual is around $450, while family plans average about $1,200 per month.

Key factors include age (older individuals pay more), location (costs vary by state), type of plan (e.g., HMO, PPO), coverage level (deductibles, copays), and whether you qualify for subsidies or employer contributions.

Yes, you can reduce costs by choosing a high-deductible plan, qualifying for subsidies through the Affordable Care Act (ACA), using employer-sponsored insurance, maintaining a healthy lifestyle, or exploring Medicaid if eligible.