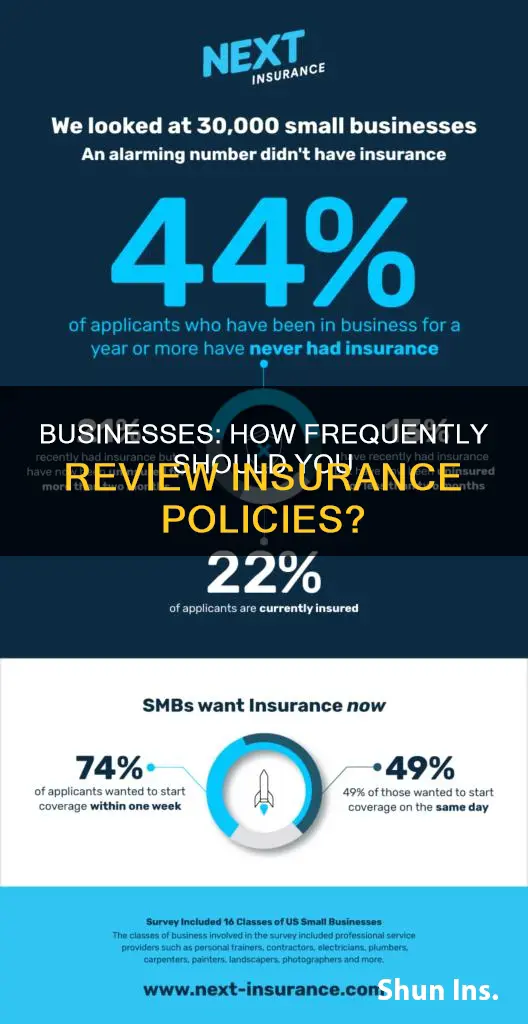

Business insurance is essential to protect yourself from the unexpected costs of running a business. Accidents, natural disasters, and lawsuits can be extremely costly, and insurance can help ensure that both your personal and business assets are fully protected. When it comes to checking insurance, businesses typically engage in a formal process called insurance verification, which involves requesting and reviewing important documents called Certificates of Insurance (COIs). These certificates provide official evidence and a summary of an insurance policy. While businesses should regularly review their own insurance policies and coverage, there is limited information on how often they check the insurance of their partners, contractors, or vendors. It is important to note that due diligence is required to ensure that all parties involved have adequate coverage.

| Characteristics | Values |

|---|---|

| Frequency of checking business insurance | Not specified |

| Formal process for insurance verification | COI (Certificate of Insurance) |

| Who can generate COI | Insurance provider of the policy in question |

| Who reviews COI | Hiring party/company |

| When to check | When hiring a contractor/third-party service provider |

| How to request COI | Email, letter, or verbal instruction |

| How often do car insurance companies check driving records | When applying for a new policy, getting a new quote, renewing an existing policy, changing the level of coverage, changing cars, adding an extra driver, or moving |

Explore related products

What You'll Learn

![]()

Importance of business insurance

Business insurance is essential to the success of your company. It protects you from the unexpected costs of running a business, including accidents, natural disasters, and lawsuits. Without insurance, you could be forced to pay for repairs, legal fees, replacement costs, and medical costs out of pocket, potentially running you out of business. With the right types of coverage, you can focus on running and growing your business, safe in the knowledge that you are protected from financial loss.

There are many types of business insurance, and it can be tricky to know where to start. Most businesses begin with a Business Owner's Policy (BOP), which combines general liability, business property, and business income insurance into one convenient policy. A BOP can help protect your business from property damage and claims of bodily injury or damage to someone else's property. It can also help replace lost income if you can't operate due to a covered property loss.

Other common types of business insurance include commercial auto insurance, workers' compensation insurance, and management liability insurance. Commercial auto insurance is required in most states if you use business-owned vehicles for work. Workers' compensation insurance is also required in most states and provides benefits to employees who suffer work-related injuries or illnesses. Management liability insurance can help protect your business from costly lawsuits and is especially important for nonprofits and publicly traded companies.

Business insurance is also important when working with partners, vendors, and third-party service providers. It is your responsibility to ensure that these parties have adequate insurance coverage. You can do this by requesting a COI (Certificate of Insurance), which is an official document providing evidence and a summary of an insurance policy.

Overall, business insurance is crucial for protecting your business from unexpected costs and liabilities. It can help you attract and retain employees, negotiate with customers, and give you peace of mind that you are protected from financial loss.

Western Union and Insurance Checks: What You Need to Know

You may want to see also

Explore related products

$20.47 $177.12

$43.95 $43.95

![]()

Checking insurance of partners and contractors

When hiring contractors, it is crucial to verify their insurance coverage to protect yourself and your business. Here are some detailed steps and considerations for checking the insurance of contractors:

Checking Insurance of Contractors

Obtaining proof of insurance from contractors is essential before allowing them to work for you. Request a certificate of insurance (COI) from the contractor, their insurance agent, or their insurance company. This document provides official evidence and a summary of their insurance policy. Verify that their coverage meets your requirements, including coverage types, policy limits, and effective dates. Ensure it aligns with the level of risk associated with the project and complies with contractual obligations, vendor requirements, and industry regulations.

In some cases, you may want to request to be added as an additional insured to their liability coverage for extra protection. Additionally, check with your state's licensing board to verify the contractor's license status. This two-pronged approach ensures that you are protected in case of mishaps, injuries, or property damage.

Understanding Insurance Types

Different types of insurance are relevant to contractors, and it's important to know which ones apply to your situation. General liability insurance, for example, covers common business risks such as customer injuries, property damage, and advertising injuries. It is often required by law or to secure certain contracts. Professional liability insurance, or errors and omissions insurance, covers mistakes and oversights made by contractors when providing professional services. If you or your contractors use personal or rented vehicles for business, consider hired and non-owned auto insurance (HNOA), as personal or commercial auto insurance may not cover work-related accidents.

Working with Insurance Companies

Insurance companies often maintain lists of preferred contractors or vendors, but you are not obligated to choose from these lists. Conduct your own research, read reviews, and obtain referrals to find a reputable contractor. Obtain estimates from multiple contractors to compare costs, services, and the scope of work. Once you've selected a contractor, communicate your decision to your insurance company and provide them with the contractor's license and insurance details. Keep in mind that the insurance company may need to approve the contractor's estimates and scope of work.

Handling Insurance Claims

When dealing with insurance claims and invoices, it's important to establish a repair payment schedule with your contractor to avoid potential payment issues. Be wary of contractors who offer to take over your claim, and always inspect their work before agreeing to payment. Typically, insurance companies will pay the contractor directly, and receipts are crucial for showing proof of loss in insurance claims.

By diligently checking the insurance of your contractors and understanding the different types of insurance and how to handle claims, you can effectively manage risks and protect your business interests.

The Federal Insurance Office: Its Role and Responsibilities

You may want to see also

Explore related products

![]()

Certificates of Insurance (COIs)

A Certificate of Insurance (COI) is a document issued by an insurance company or broker that confirms that an insurance policy is in place and outlines its terms and conditions. It is a formal process for verifying that a company carries the proper insurance. It is also known as a certificate of liability insurance or proof of insurance.

COIs are typically requested by clients or independent contractors before agreeing to work with a business. This is to ensure that the business has the necessary insurance coverage and that the client will not assume any risk in the event of damage, injury, or substandard work. For example, a landscaping company may be required to provide a COI to prove they have an active policy that can protect against claims of bodily injury and property damage.

A COI is also important for business owners and contractors to secure contracts. It demonstrates that they have liability insurance, which protects against workplace accidents or injuries. A standard COI includes the policyholder's name, mailing address, policy coverage dates, policy limits, and a description of the operations the insured performs. It may also include additional insureds, special conditions, and the insurance company's contact information.

To obtain a COI, a business owner can request one from their insurance company, either through their online account or by contacting their insurance agent. It is recommended to use a written format for the request to keep proper documentation. Once the COI is received, it is important to review and verify that the coverage meets the required needs and that all details are correct.

Federal Insurance: What is PMI and Why it Matters

You may want to see also

Explore related products

![]()

Insurance for businesses as primary income

Business income insurance, also known as business interruption insurance, is an important form of protection for companies, ensuring they can cover lost income in the event of damage to their property. This type of insurance is particularly relevant for businesses in areas prone to severe weather events or natural disasters, as well as those with a high risk of fire or other specific risks. It can also cover lost income due to damage at the premises of key suppliers.

Business income insurance is often included in a Business Owners Policy (BOP) or can be added as an extra. It typically covers lost net income, payroll expenses, loan payments, and mortgage, lease, and rental payments. It may also cover temporary relocation expenses. The cost of business income insurance is determined by a risk assessment, which takes into account factors such as the coverage amount, type of business, number of employees, location, and prior claims history.

To ensure adequate coverage, businesses should assess their risks, including the likelihood of accidents, natural disasters, or lawsuits. Commercial property insurance, for example, can protect against loss due to damage to physical property. It is also important to consider the legal requirements for business insurance, which can vary by state.

When working with contractors or third-party service providers, it is crucial to verify their insurance coverage. This can be done by requesting a Certificate of Insurance (COI), which serves as official evidence and a summary of their insurance policy.

Overall, business income insurance provides essential financial protection, helping businesses stay afloat during unexpected disruptions and ensuring they can meet their financial obligations until they can resume normal operations.

Logging Insurance Checks in QuickBooks: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Driving records for auto insurance

Driving records are an important factor in determining auto insurance rates. Insurers view accidents, excessive insurance claims, and traffic violations as red flags, indicating that a driver may be high-risk. A clean driving record typically means having no violations or claims, but different insurance providers may have varying definitions of a good record. For example, some companies may significantly increase rates after a speeding ticket, while others may only impose a small increase for a first offence.

Insurance companies usually check driving records when a driver applies for a new policy and at renewal. They can retrieve this information by using a driver's license number. The specific details included in a driving record can vary depending on state law. For instance, in North Carolina, a driving record includes license status, such as whether it is valid, expired, or suspended.

It is recommended that individuals check their driving records regularly, such as once a year, to ensure accuracy and be aware of any negative marks. They can do this by requesting a copy from their state's Department of Motor Vehicles (DMV) or their insurance carrier, which may provide it for free or a small fee. Some states offer different types of driving records, such as an "unattested" record for personal information purposes and a "true and attested" record for official and court use.

Over time, accidents and traffic violations may age off a driving record, improving insurance rates if no new incidents occur. Individuals can also explore other options to reduce their premiums, such as discounts or raising their deductibles. Shopping around for the best insurance rates can help individuals find the most suitable coverage for their driving history.

Federal Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Businesses can verify insurance coverage by requesting a COI (Certificate of Insurance) from their partners, contractors, or vendors. A COI is a legal document that serves as official evidence and a summary of an insurance policy.

Businesses should review their insurance policies regularly, especially after making significant changes or improvements. For example, if a business expands its physical location, adds new structures, or makes substantial purchases, it should update its insurance company to ensure adequate coverage.

Car insurance companies typically check driving records when individuals apply for a new policy, request a new quote, or renew their existing coverage. They may also check driving records if policyholders request changes to their coverage, such as adding a new driver or vehicle. Most companies review the previous three to five years of driving history, but some may go back further.

Car insurance companies primarily aim to assess the risk associated with insuring a driver. They look for accidents, traffic violations, speeding tickets, and claims history. These factors help determine whether an individual is a high-risk or low-risk driver, which impacts the insurance premium.