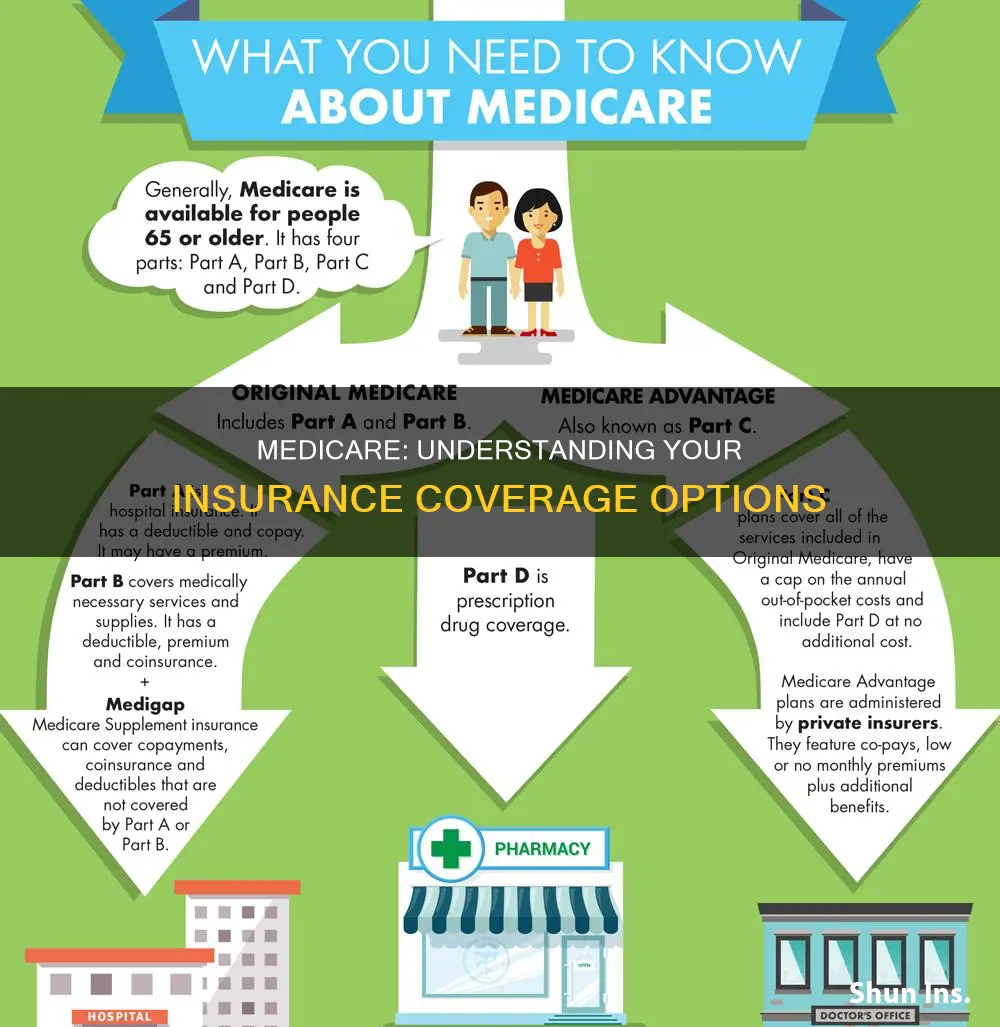

Medicare is a federal health insurance program for people aged 65 and over, and some people under 65 with certain disabilities or conditions. Original Medicare includes two parts: Part A (Hospital Insurance) and Part B (Medical Insurance). After meeting your deductible, you pay your share of costs for services and supplies as you get them. There is no limit on what you pay out-of-pocket annually unless you have other coverage, such as Medigap, Medicaid, or employer insurance. Medicare Advantage Plans (Part C) are private insurance options that cover hospital and medical costs, while Part D covers prescription medications.

| Characteristics | Values |

|---|---|

| Number of people insured by Medicare in 2022 | 65 million |

| Age group | 57 million people aged 65 and older, 8 million younger people |

| Percentage of healthcare expenses covered | 50% |

| Additional coverage | Medigap insurance, Medicare Part D prescription drug plan, or a private Medicare Part C (Medicare Advantage) plan |

| Spending in 2022 | Over $900 billion |

| Funding sources | U.S. Treasury, Part A Trust Fund (funded by payroll taxes), and premiums paid by beneficiaries |

| Eligibility | U.S. citizens or permanent residents living in the U.S. for at least 5 continuous years, aged 65 and older, or under 65 with certain disabilities or conditions |

| Parts of Medicare | Part A (Hospital Insurance), Part B (Medical Insurance), Part C (Medicare Advantage), and Part D (prescription drug coverage) |

| Cost structure | Premiums, deductibles, and coinsurance paid out-of-pocket; additional costs for monthly premiums and services in Medicare Advantage Plans |

| Coverage limitations | Doesn't cover all medical costs; excludes long-term care, vision, dental, hearing aids, private-duty nursing, and prescription drugs |

| Role of private companies | Medicare-approved private companies offer plans that follow Medicare rules; extra insurance can be purchased from private companies to help with cost-sharing |

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

What You'll Learn

![]()

Medicare Part A and Part B

Medicare Part A

Medicare Part A (Hospital Insurance) helps to pay for inpatient care in hospitals, critical access hospitals, and skilled nursing facilities. It also covers hospice care, some home health care, and inpatient hospital care. Most people get Part A for free, but some have to pay a premium for this coverage. To be eligible for premium-free Part A, an individual must be entitled to receive Medicare based on their own earnings or those of a spouse, parent, or child. To receive premium-free Part A, the worker must have a specified number of quarters of coverage (QCs) and file an application for Social Security or Railroad Retirement Board (RRB) benefits. The exact number of QCs required depends on whether the person is filing for Part A on the basis of age, disability, or End Stage Renal Disease (ESRD). If you are receiving monthly Social Security or RRB benefits, at least 4 months before turning 65, you will get Part A automatically at age 65.

Medicare Part B

Medicare Part B (Medical Insurance) helps cover two types of services: medically necessary services and preventive services. Medically necessary services are services or supplies that meet accepted standards of medical practice to diagnose or treat your medical condition. Preventive services are healthcare to prevent illness (like the flu) or detect it at an early stage when treatment is likely to be most effective. Most people pay a monthly premium for Part B, and the exact premium depends on your income level. If you have Part B and Medicare Supplement Insurance (Medigap) that pays your Part B coinsurance, your Medigap plan should cover the cost of insulin. If you've been covered by an active employer group health plan (either yours or your spouse's) since turning 65, and it ended within the last 8 months, you can enroll in Part B without any penalty. This is considered a "Special Enrollment Period."

Transitioning from COBRA to Individual Medical Insurance: A Guide

You may want to see also

Explore related products

![]()

Medicare Advantage Plans

It is important to note that Medicare Advantage Plans can disenroll you for various reasons, such as moving outside their service area or losing Medicare eligibility. Before enrolling, it is recommended to consult your employer, union, or benefits administrator, as doing so may impact your existing coverage.

When considering Medicare Advantage Plans, it is essential to review the specific details, including coverage, network restrictions, and potential disenrollment factors, to ensure that it aligns with your healthcare requirements and preferences.

Transferring Medical Insurance to a New Company: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Medicare for those under 65

Medicare is typically available for people aged 65 and over. However, there are provisions in place for those under 65 to access Medicare earlier in certain circumstances.

If you are under 65 and receiving disability benefits from Social Security, you will automatically receive Medicare after receiving disability benefits for 24 months, or when you turn 65, whichever comes first. This applies to those with End-Stage Renal Disease (ESRD), or ALS (Lou Gehrig's Disease). Medicare coverage for those qualifying based on disability is the same as for those qualifying based on age, and there are no illnesses or underlying conditions that disqualify people from coverage. Beneficiaries are entitled to an individualized assessment of whether they meet the coverage criteria.

If you are still working when you turn 65, you may be able to delay your Medicare enrollment, depending on your employer's insurance coverage. If your employer has 20 or more employees, you can generally choose to delay Medicare enrollment, drop your employer's coverage for Medicare, or have both. If your employer has fewer than 20 employees, you will likely need to enroll in Medicare during your Initial Enrollment Period.

The Initial Enrollment Period for Medicare begins 3 months before you turn 65 and ends 3 months after the month you turn 65, a total of 7 months. If you miss this period, you may have to pay a penalty.

The Center for Medicare Advocacy is currently working on a project to assist State Health Insurance Assistance Programs (SHIPs) and Senior Medicare Patrol Programs (SMPs) in reaching and serving Medicare beneficiaries under 65. The project will test different approaches in Connecticut, California, and Louisiana.

California's Medical Insurance: Penalty for the Uninsured?

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UY218_.jpg)

![]()

Medicare with other insurance

Medicare is a public health insurance program, while Medicaid is a public health insurance program run by individual states. Medicare is available to people over 65 and those with disabilities. It is also available to people with End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS).

Medicare consists of two parts: Part A (Hospital Insurance) and Part B (Medical Insurance). Original Medicare covers most, but not all, of the costs for approved health care services and supplies. After meeting the deductible, the patient pays their share of the costs for services and supplies as they receive them. There is no limit on out-of-pocket annual payments unless the patient has other coverage.

Medicare can be combined with other insurance plans, such as private insurance, Medicaid, employer coverage, or Tricare military health insurance. When an individual has Medicare and another health insurance plan, one insurance provider is designated the "primary payer" and the other is the "secondary payer". The primary payer pays for any covered services until the coverage limit has been reached, after which the secondary payer covers any remaining expenses. The order of payment is called "coordination of benefits". If the secondary payer does not cover the remaining balance, the patient may be responsible for the remaining costs.

If an individual has Medicare and private insurance, the primary payer depends on the type of private insurance and their situation. For example, if they have insurance through their employer, it is usually the primary payer, and Medicare is the secondary payer. However, if an individual has private insurance through their spouse's employer, Medicare may be the primary payer.

The Tedium of Medical Coding: Why It's Unpopular

You may want to see also

Explore related products

![]()

Medicare drug plans

Medicare is a health insurance program that provides coverage for people aged 65 and over, as well as some younger people with disabilities or end-stage renal disease. Original Medicare includes two parts: Part A (Hospital Insurance) and Part B (Medical Insurance).

Medicare drug coverage, also known as Part D, is optional supplemental coverage that helps pay for prescription drugs. It is available to everyone with Medicare, and most Medicare Advantage Plans include this coverage. In most cases, you cannot join a separate Medicare drug plan if you are already enrolled in a Medicare Advantage Plan.

Each Medicare drug plan has a list of covered drugs called a "formulary," which varies in cost and specific medications covered. Most plans have a monthly premium that you pay in addition to your Part B premium. The costs for prescription drugs under Medicare drug plans can vary depending on the specific plan and the medications covered.

When choosing a Medicare drug plan, it is important to review the formulary to ensure that your prescribed medications are covered. Additionally, it is worth considering the cost of the plan, including any premiums, deductibles, and copayments or coinsurance associated with the prescription drugs.

Home Ownership and Medicaid: What You Need to Know

You may want to see also

Frequently asked questions

Medicare is federal health insurance for anyone aged 65 and older, and some people under 65 with certain disabilities or conditions. The two parts of Original Medicare are Part A (Hospital Insurance) and Part B (Medical Insurance). Medicare Part C is also known as Medicare Advantage, a private insurance option that covers hospital and medical costs. Part D covers prescription medications.

The Initial Enrollment Period to sign up for Medicare begins 3 months before you turn 65 and ends 3 months after the month you turn 65. If you miss this period, you may have to pay a penalty. If you are still working at 65, you can apply online for Medicare only.

Original Medicare covers most of the costs for approved health care services and supplies. Medicare also covers many preventive services, like shots and screenings. If you get a service that Medicare doesn't cover, you pay the full cost.