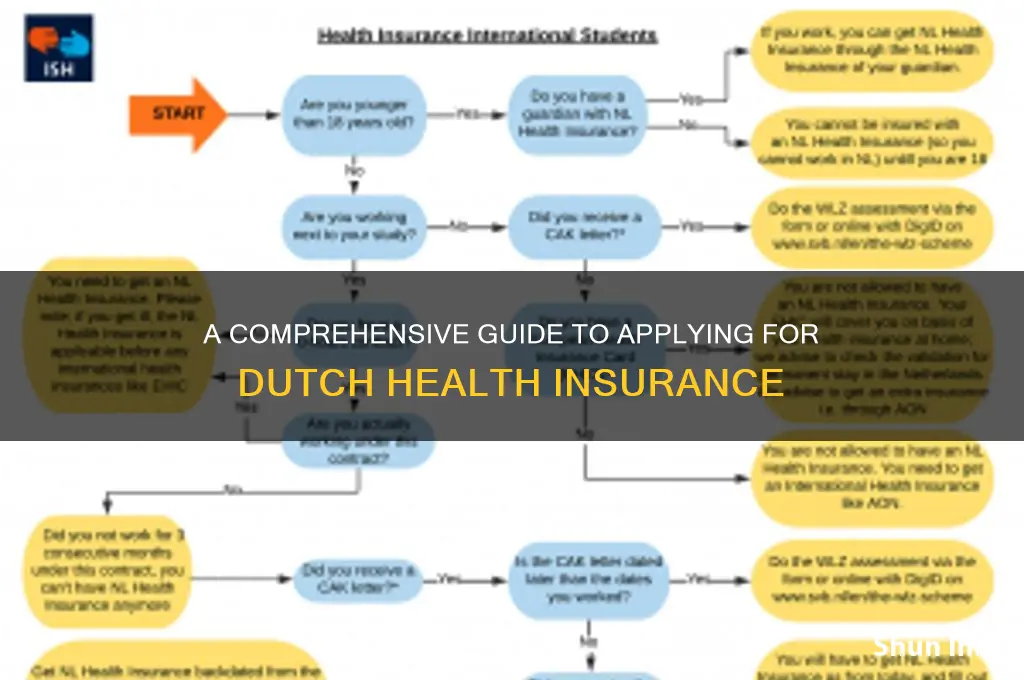

Applying for Dutch health insurance is a straightforward process, but it’s essential for anyone living or working in the Netherlands, as it is mandatory by law. The first step is to choose a health insurance provider, known as a *zorgverzekeraar*, from the many options available, comparing coverage, premiums, and additional services to find the best fit for your needs. Once you’ve selected a provider, you can apply online, by phone, or in person, typically requiring personal details such as your BSN (citizen service number), address, and bank information. After submitting your application, the insurer will process it and send you a confirmation, usually within a few days, after which you’ll receive your insurance card and policy details. It’s important to note that you must apply within four months of registering with your municipality to avoid gaps in coverage, and premiums are automatically deducted monthly from your bank account. Understanding the basics of Dutch health insurance, including the mandatory basic package (*basisverzekering*) and optional additional coverage (*aanvullende verzekering*), will help ensure you make an informed decision tailored to your health and financial situation.

| Characteristics | Values |

|---|---|

| Eligibility | All residents of the Netherlands are legally required to have health insurance. Non-residents may also need it depending on their visa type. |

| Type of Insurance | Basic health insurance (basisverzekering) is mandatory. Optional supplementary insurance (aanvullende verzekering) is available. |

| Application Period | You must apply within 4 months of becoming a resident. If you miss this, you may face a fine. |

| Application Method | Apply directly through an insurance provider (online, by phone, or in person). |

| Required Documents | - Proof of identity (passport/ID card) - BSN (Burgerservicenummer) - Proof of residency (registration with municipality) |

| Insurance Providers | Examples: Zilveren Kruis, CZ, Menzis, VGZ, etc. Compare plans using comparison tools like Zorgwijzer or Independer. |

| Premiums | Monthly premiums vary by provider. The government sets a mandatory excess (eigen risico) of €385 (2023). |

| Coverage Start Date | Coverage typically starts on the first day of the month following your application. |

| Healthcare Allowance (Zorgtoeslag) | Low-income individuals may qualify for a healthcare allowance to help pay premiums. Apply via the Tax Authority (Belastingdienst). |

| Switching Insurers | You can switch insurers annually during the switching period (November-December) for coverage starting January 1. |

| Cancellation | You can cancel your insurance if you leave the Netherlands. Notify your insurer and deregister from the municipality. |

| Mandatory Excess (Eigen Risico) | €385 (2023). You pay the first €385 of healthcare costs annually before insurance covers additional costs. |

| Supplementary Insurance | Covers additional services like dental, physiotherapy, or alternative medicine. Not mandatory. |

| European Health Insurance Card (EHIC) | Included with basic insurance for healthcare coverage within the EU/EEA. |

| Student Insurance | Students under 27 may qualify for a discounted premium. Check eligibility with insurers. |

Explore related products

What You'll Learn

- Eligibility Requirements: Check residency status, age, and income criteria for Dutch health insurance eligibility

- Choosing a Provider: Compare insurers, coverage options, premiums, and additional services for the best fit

- Application Process: Gather documents, complete forms, and submit online or via mail to apply

- Coverage Details: Understand mandatory basic coverage and optional extras like dental or physiotherapy

- Payment & Deadlines: Set up premiums, know payment schedules, and avoid penalties for late applications

![]()

Eligibility Requirements: Check residency status, age, and income criteria for Dutch health insurance eligibility

To apply for Dutch health insurance, understanding the eligibility requirements is crucial. The Netherlands operates under a mandatory health insurance system, known as the Zorgverzekeringswet (ZVW), which requires all residents to have basic health coverage. However, not everyone automatically qualifies, and eligibility hinges on specific criteria: residency status, age, and income.

Residency Status: The Foundation of Eligibility

Eligibility for Dutch health insurance begins with residency. If you’re officially registered as a resident in the Netherlands, you’re required by law to purchase basic health insurance within four months of registration. This applies to Dutch citizens, EU/EEA nationals, and non-EU residents with a valid residence permit. Temporary visitors or those on short-term visas (e.g., tourists or business travelers) are generally exempt but may need travel insurance instead. Pro tip: Ensure your registration at the municipality (Gemeente) is complete, as this triggers your obligation to enroll in health insurance.

Age Considerations: No Discrimination, But Specifics Apply

Age is not a barrier to eligibility for Dutch health insurance, as the system is designed to be inclusive. Children under 18 are automatically covered under their parent’s or guardian’s policy, though some insurers offer additional child-specific packages. For adults, age does not affect eligibility, but it may influence premiums slightly due to risk assessments by insurers. Interestingly, retirees and pensioners are also required to maintain coverage, though they may qualify for healthcare allowances (zorgtoeslag) if their income is below a certain threshold.

Income Criteria: Affordability and Allowances

While income doesn’t determine eligibility for basic health insurance, it plays a role in accessing financial support. The Dutch government provides a healthcare allowance (zorgtoeslag) to low-to-middle-income earners to help cover premiums. For 2023, individuals earning up to €31,915 annually or joint earners up to €63,830 may qualify. To apply, you’ll need a DigiD (digital ID) and must submit your income details via the Tax Authority’s website. Caution: Failing to apply for zorgtoeslag if eligible means missing out on significant savings, as premiums can exceed €100 per month.

Practical Steps to Verify Eligibility

To confirm your eligibility, start by checking your residency status through the IND (Immigration and Naturalisation Service) or your local municipality. Next, review your age category to understand if additional coverage is needed for dependents. Finally, calculate your annual income to assess whether you qualify for zorgtoeslag. Tools like the Tax Authority’s online calculator can streamline this process. Remember, eligibility is not just about meeting criteria—it’s about understanding your rights and obligations within the Dutch healthcare system.

By carefully examining these factors, you can navigate the eligibility requirements with confidence, ensuring compliance with Dutch law and access to essential healthcare services.

Why Renters Insurance Companies Need Your Mailing Address Explained

You may want to see also

Explore related products

![]()

Choosing a Provider: Compare insurers, coverage options, premiums, and additional services for the best fit

Selecting the right health insurance provider in the Netherlands is akin to tailoring a suit—it must fit your specific needs, lifestyle, and budget. Start by identifying your priorities: Are you a young professional seeking basic coverage, or a family needing comprehensive care? The Dutch market offers a range of insurers, each with unique plans, so clarity on your requirements is essential. For instance, if you frequently travel within Europe, ensure your insurer provides adequate coverage under the European Health Insurance Card (EHIC). Conversely, if you rarely visit a doctor, a lower premium plan with higher deductibles might suffice.

Next, compare insurers systematically. Use comparison tools like *Zorgwijzer* or *Independer* to evaluate premiums, coverage options, and customer satisfaction ratings. Premiums vary widely—as of 2023, monthly costs range from €120 to €150 for basic plans—but don’t let price alone dictate your choice. Analyze what’s included: Does the insurer cover alternative therapies like physiotherapy or acupuncture? Are dental care or vision services part of the package, or do they require additional premiums? For example, some insurers offer *aanvullende verzekering* (supplementary insurance) for these services, which can be cost-effective if you anticipate such needs.

Coverage options extend beyond medical treatments. Consider additional services that enhance your overall experience. Some insurers provide access to digital health platforms, offering 24/7 medical advice or online consultations. Others include preventive care programs, such as discounted gym memberships or mental health support. For instance, CZ Zorgverzekering offers a *Vitality* program that rewards healthy behaviors with discounts on premiums. These perks can add significant value, especially if you’re proactive about wellness.

Finally, scrutinize the fine print. Deductibles (*eigen risico*) in the Netherlands are set at €385 for 2023, but some insurers allow you to voluntarily increase this amount to lower your premium. However, this strategy is risky if you anticipate high medical expenses. Also, check for exclusions and limitations. For example, certain insurers may not cover pre-existing conditions during the first year of your policy. By weighing these factors against your health history and future needs, you can avoid unexpected costs and ensure your chosen provider aligns with your long-term goals.

In conclusion, choosing a Dutch health insurance provider requires a balance of research, self-awareness, and foresight. By comparing insurers, understanding coverage nuances, and valuing additional services, you can secure a plan that not only meets your current needs but also adapts to your evolving health journey. Remember, the goal isn’t just to find the cheapest option—it’s to find the best fit.

Doerfer Wilsey Insurance in Dowagiac, Michigan: What to Expect

You may want to see also

Explore related products

![]()

Application Process: Gather documents, complete forms, and submit online or via mail to apply

Applying for Dutch health insurance begins with gathering the necessary documents, a step that can feel overwhelming but is straightforward with the right preparation. You’ll need proof of identity, such as a passport or ID card, and residency documents like a BSN (Burgerservicenummer) or proof of address. If you’re employed, include a recent payslip or employment contract. Non-EU residents may require additional paperwork, such as a visa or residence permit. Organizing these documents in advance streamlines the process, ensuring you’re not scrambling at the last minute.

Once your documents are in order, the next step is completing the required forms, which vary depending on the insurer. Most providers offer digital application forms on their websites, designed to guide you through questions about your health, lifestyle, and coverage preferences. Be honest and thorough—inaccuracies can lead to complications later. For instance, if you have pre-existing conditions, disclose them to avoid coverage gaps. Some insurers may also ask for a recent health declaration, so be prepared to provide details if needed.

Submitting your application is where you decide between online convenience and traditional mail. Online submissions are faster and often preferred, with instant confirmations and shorter processing times. Most insurers provide secure portals for uploading documents and forms. If you opt for mail, ensure your package includes all required documents and is sent via registered post for tracking. Keep copies of everything you submit, as these may be needed for future reference. Processing times vary, but you’ll typically receive a response within two weeks.

A practical tip: double-check the insurer’s requirements before submitting. Some may have specific formats for documents (e.g., PDFs for online uploads) or additional forms for certain demographics, like students or freelancers. If you’re unsure, contact the insurer’s customer service for clarification. This proactive approach minimizes delays and ensures your application is processed smoothly. Remember, the goal is not just to apply but to secure the right coverage for your needs.

Finally, consider the timing of your application. In the Netherlands, you’re required to have health insurance within four months of receiving your residence permit or registering with the municipality. Missing this deadline can result in fines. Plan ahead, especially if you’re relocating, to avoid unnecessary stress. By gathering documents, completing forms accurately, and submitting your application promptly, you’ll navigate the process efficiently and start your coverage without hiccups.

Uber's Medical Insurance: Work Comp Coverage?

You may want to see also

Explore related products

![]()

Coverage Details: Understand mandatory basic coverage and optional extras like dental or physiotherapy

In the Netherlands, every resident is legally required to have basic health insurance, known as the *basisverzekering*. This mandatory coverage is designed to ensure that everyone has access to essential medical services, including general practitioner visits, hospital care, maternity care, and emergency treatments. The government sets the minimum requirements for this policy, ensuring a standardized level of care across providers. However, while the coverage is comprehensive in many areas, it does not include everything—a fact that often surprises newcomers to the Dutch system.

The *basisverzekering* excludes certain services, such as dental care for adults (covered only for those under 18), physiotherapy (except for chronic conditions), and cosmetic procedures. This is where optional extras come into play. Supplemental insurance, or *aanvullende verzekering*, allows you to tailor your coverage to your specific needs. For instance, if you frequently visit the dentist or require regular physiotherapy sessions, adding these as extras can save you from out-of-pocket expenses. Providers often offer tiered packages, ranging from basic to extensive, with premiums increasing accordingly.

When considering optional extras, it’s crucial to evaluate your lifestyle and health needs. For example, if you’re an athlete or have a physically demanding job, physiotherapy coverage might be a wise investment. Similarly, if you’re prone to dental issues, a package that includes adult dental care could prevent unexpected costs. However, be cautious not to over-insure. Some extras, like worldwide travel insurance or alternative medicine coverage, may be unnecessary depending on your circumstances. Always compare policies and read the fine print to understand exclusions and limitations.

One practical tip is to use comparison tools available on websites like *Zorgwijzer* or *Independer* to analyze different insurers and their offerings. These platforms allow you to filter by price, coverage, and customer reviews, making it easier to find a plan that aligns with your needs. Additionally, consider consulting an independent insurance advisor, especially if you have complex health requirements or are unsure about which extras to prioritize.

In conclusion, while the Dutch basic health insurance provides a robust foundation, understanding its limitations and strategically adding optional extras can enhance your coverage significantly. By assessing your personal health needs and using available resources to compare options, you can build a policy that offers both peace of mind and financial protection. Remember, the goal is not just to comply with legal requirements but to ensure you’re adequately covered for life’s uncertainties.

Leaking Pool Woes: Can Your Insurance Company Cover the Costs?

You may want to see also

Explore related products

![]()

Payment & Deadlines: Set up premiums, know payment schedules, and avoid penalties for late applications

In the Netherlands, health insurance premiums are a monthly commitment, typically ranging from €100 to €150, depending on the coverage level and insurer. Setting up automatic payments through direct debit is the most common method, ensuring timely payments and avoiding late fees. Most insurers offer digital platforms where you can manage your payment details, view invoices, and update your payment schedule. This streamlined approach not only simplifies the process but also reduces the risk of missed payments, which can lead to coverage gaps or administrative penalties.

Understanding payment schedules is crucial, as premiums are usually due at the end of each month. Insurers may offer flexibility, such as the option to pay annually for a slight discount, but monthly payments are the norm. It’s essential to check your policy for specific due dates and grace periods, as these can vary. For instance, some insurers allow a 10-day grace period after the due date, while others may charge a late fee immediately. Familiarizing yourself with these details can save you from unnecessary stress and financial strain.

Late applications for health insurance in the Netherlands can result in penalties, including a statutory excess of up to €385 (as of 2023) for each month you delay. This penalty is in addition to the regular mandatory excess of €385 per year. For example, if you apply three months late, your total excess for the year could rise to €1,540. To avoid this, ensure you apply for insurance within four months of moving to the Netherlands or becoming eligible. If you’re switching insurers, apply at least one month before your current policy ends to maintain continuous coverage and avoid penalties.

A practical tip for expats or new residents is to set reminders for key dates, such as the annual switching period (November 1 to December 31) and your policy renewal date. During the switching period, you can compare premiums and coverage options without penalties, potentially saving money. Additionally, keep an eye on policy changes from your insurer, as premiums may increase annually. By staying proactive and informed, you can manage your payments effectively and avoid unnecessary financial burdens.

In summary, managing premiums and deadlines in Dutch health insurance requires attention to detail and proactive planning. Automate payments, understand your schedule, and adhere to application timelines to avoid penalties. By leveraging digital tools and staying informed about policy changes, you can ensure seamless coverage and financial stability. Remember, timely action not only protects your health but also your wallet.

Understanding Medical Insurance Copayments in India

You may want to see also

Frequently asked questions

Everyone living or working in the Netherlands is legally obligated to have basic Dutch health insurance, known as *zorgverzekering*.

You can apply directly through an insurance provider’s website, by phone, or via an independent broker. Compare plans using comparison tools like *Zorgwijzer* or *Independer*.

Apply as soon as possible after registering in the Netherlands. You have a 4-month window to choose a policy, but coverage must start within this period to avoid fines.

You’ll typically need your BSN (citizen service number), proof of residence, and a valid ID. Some providers may also require a bank account number for direct debit payments.

Yes, you can choose from any licensed provider in the Netherlands. Compare premiums, coverage, and additional services to find the best fit for your needs.