Mortgage insurance is a policy that protects the lender in case the borrower defaults on their payments. It is usually required when the borrower's down payment is less than 20% of the purchase price. The insurance can be paid in a lump sum upfront or through monthly payments, and it increases the overall cost of the loan. Private Mortgage Insurance (PMI) is one type of mortgage insurance that is often required for conventional loans. Borrowers can request their lenders to cancel PMI once they have built up enough equity in their homes, which is typically when the loan-to-value (LTV) ratio reaches 78-80% of the original value of the home. To avoid paying PMI, borrowers can also consider refinancing, getting a new appraisal, or paying down their mortgage faster.

| Characteristics | Values |

|---|---|

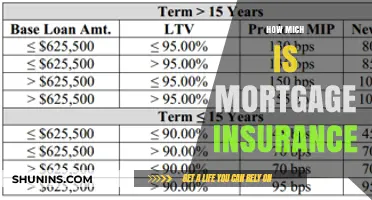

| When to ask the lender to forgo mortgage insurance | When your loan-to-value (LTV) ratio reaches 78% of the home's purchase price, or when the loan term is halfway through. |

| How to ask the lender to forgo mortgage insurance | Submit a written request to your mortgage servicer to cancel PMI once you've built up the required amount of equity in your home. |

| What to do if the lender doesn't agree to forgo mortgage insurance | Consider refinancing to a new loan with a lower balance, getting a reappraisal, or paying down your mortgage faster. |

Explore related products

$10.65 $22.99

What You'll Learn

![]()

Check your PMI disclosure form

Private mortgage insurance (PMI) is a type of insurance that you may be required to purchase if you take out a conventional loan with a down payment of less than 20% of the purchase price. It lowers the risk to the lender of making a loan to you, so you can qualify for a loan that you might not otherwise be able to get. However, it increases the cost of your loan.

If you are required to pay mortgage insurance, you have the right to ask your lender to cancel PMI on the date the principal balance of your mortgage is scheduled to fall to 80% of the original value of your home. The first date you can make the request should appear on your PMI disclosure form, which you would have received along with your mortgage. If you can't find the disclosure form, contact your lender.

Your lender must automatically terminate PMI on the date when your principal balance is scheduled to reach 78% of the original value of your home, provided that you are current on your payments. You can also ask to cancel PMI ahead of the scheduled date if you have made additional payments that reduce the principal balance of your mortgage to 80% of the original value of your home. To do this, you may submit a written request to have your mortgage servicer cancel your PMI.

You can calculate your loan-to-original-value (LTOV) ratio by dividing your current unpaid principal balance by the purchase price of your home or the appraised value at closing, whichever is less. If your loan has met certain conditions and your LTOV ratio falls below 80%, you may be able to cancel your PMI.

Additionally, if you have an FHA loan, you may be able to refinance to a conventional loan and eliminate your mortgage insurance premium (MIP). With soaring home values, you may have the equity you need to refinance and avoid paying PMI. However, it's important to check with your lender for any rules or requirements before ordering an appraisal.

House Insurance: A French Legal Requirement?

You may want to see also

Explore related products

![]()

Make additional payments

Making additional payments on your mortgage is a way to get rid of private mortgage insurance (PMI). PMI is typically required when you take out a mortgage loan and your down payment is less than 20% of the purchase amount. It protects the lender in case you default on your payments.

You can prepay your mortgage by making additional payments in several ways, including biweekly payments, an extra payment each year, or a lump sum at any time. It is important to check with your lender to ensure that these extra payments go towards the loan's principal and not your next payment or interest.

If you make additional payments that reduce the principal balance of your mortgage to 80% of the original value of your home, you can ask your lender to cancel the PMI ahead of the scheduled date. This is known as the PMI cancellation window. You can calculate your loan-to-original-value (LTOV) ratio by dividing your current unpaid principal balance by the purchase price of your home or the appraised value at closing, whichever is less.

Keep in mind that the rules for cancelling PMI may vary depending on the type of loan you have. For example, if you have a Federal Housing Administration (FHA) loan, you may be paying a mortgage insurance premium (MIP) instead, which has different requirements for cancellation.

Petronas Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![]()

Refinance

Refinancing is one way to get rid of mortgage insurance. If you have an FHA loan, you can refinance to a conventional loan to eliminate your mortgage insurance premium (MIP). You may also have the equity required to refinance and avoid paying private mortgage insurance (PMI).

Mortgage insurance is typically required when a borrower makes a down payment of less than 20% of the purchase price of the home. It lowers the risk to the lender of making a loan to you, but it increases the cost of your loan.

If you have an FHA loan, you will pay MIP for either 11 years or the entire length of the loan, depending on the terms. You can request to cancel your PMI once you have reached 20% equity, or when your loan-to-value (LTV) ratio falls below 80%. Your lender must automatically terminate PMI when the LTV reaches 78%check with your lender for any rules or requirements before ordering an appraisal. You can also reach out to a mortgage loan officer to discuss your situation and determine your best course of action.

Insurance for Indian Parents: Is It Worth the Cost?

You may want to see also

![]()

Get a new appraisal

Getting a new appraisal is one way to forgo mortgage insurance. An appraisal can help you prove that your loan-to-value ratio (LTV) is now below 80%, which is the threshold for Private Mortgage Insurance (PMI) removal. The LTV is calculated by dividing your current unpaid principal balance by the appraised value of your home.

You can request a new appraisal if your home's current value has risen since you first purchased it. This could be due to rising home prices or because you've made improvements, such as upgrading your kitchen or remodelling your bathroom. An appraisal usually costs a few hundred dollars, depending on your location and property characteristics.

Before ordering an appraisal, check with your lender for any rules or requirements they may have. For example, some lenders might be willing to accept a broker price opinion, which is often cheaper than a full appraisal. It's also important to ensure your loan is in good standing, with no missed payments or other complicating factors such as a lien on the home.

Once you have the new appraisal, submit a formal request to your lender to cancel your PMI. If your loan is still relatively new, additional restrictions may apply, and you may need to hit a lower LTV for several years after signing. Check your loan terms or speak to your loan officer to understand the specific requirements.

Keep in mind that even without PMI, your lender may still require you to have mortgage insurance, especially if you have a Federal Housing Administration (FHA) loan. In this case, refinancing your FHA loan into a conventional loan without PMI may be an option if you have sufficient home equity (at least 20%).

Container Insurance: Necessary Protection or Unnecessary Cost?

You may want to see also

![]()

Check your loan estimate

A loan estimate is a useful tool that tells you important details about a mortgage loan you have requested. It is important to check your loan estimate to ensure that it reflects what you discussed with the lender. Here are some key things to look out for when reviewing your loan estimate:

Loan Amount and Down Payment

Check that the loan amount is what you expected and discussed with the lender. Ensure that the loan amount plus your down payment equals the sale price of the home. If it doesn't, ask the lender for an explanation. Typically, you will need to pay for mortgage insurance if your down payment is less than 20% of the home's purchase price.

Monthly Principal & Interest

Understand the components of your monthly payment. Principal refers to the amount you will borrow, while interest is the lender's charge for lending you money. Your total monthly payment will typically include additional charges such as taxes and insurance. Make sure your Estimated Total Monthly Payment matches your expectations.

Closing Costs

Review your estimated closing costs. Closing costs are one-time fees associated with getting a mortgage, typically ranging from 2% to 5% of the mortgage amount. These may include the lender's origination fee, recording fees, and settlement and title service fees. Ensure you have enough cash on hand to cover these costs.

Mortgage Insurance

Pay attention to any mention of mortgage insurance in your loan estimate. Mortgage insurance is typically required if your down payment is less than 20% of the home's price. It protects the lender in case you default on payments. If mortgage insurance is included, understand how it will impact your total monthly payment and overall loan costs.

Accuracy and Consistency

Check for any inaccuracies or inconsistencies in the loan estimate. Verify the spelling of your name and confirm that the loan term, purpose, product, and type match your discussions with the lender. If you notice any discrepancies, ask the lender to correct them.

Remember, you can request multiple loan estimates from different lenders to compare and choose the loan that best suits your needs. Don't hesitate to ask questions and seek clarification to ensure you fully understand the terms of your loan.

PSIP: Worth the Cost?

You may want to see also

Frequently asked questions

Mortgage insurance lowers the risk to the lender of making a loan to you, so you can qualify for a loan that you might not otherwise be able to get. Typically, you may be required to have mortgage insurance when you take out a mortgage loan and your down payment is less than 20% of the purchase amount.

You have the right to ask your mortgage lender or servicer to cancel PMI once you’ve built up the required amount of equity in your home. You can also ask for cancellation as soon as your balance hits 80% of the home's purchase price, so long as you’re in good standing with your payments.

The requirement to have mortgage insurance varies by lender and loan product. Consider asking your lender if PMI is required, and if so, if there are exceptions to their requirement for which you may qualify.

If you get a conventional loan, your lender could arrange for mortgage insurance with a private company, known as private mortgage insurance (PMI). If you get a Federal Housing Administration (FHA) loan, your mortgage insurance premiums are paid to the FHA, known as a mortgage insurance premium (MIP).