Property mortgage insurance, also known as private mortgage insurance (PMI), is an extra expense for borrowers who take out a conventional mortgage with a down payment of less than 20%. It is designed to protect the lender in the event that the borrower defaults on their loan payments. While PMI is not required for all types of mortgages, it is a common requirement for borrowers who obtain a conventional mortgage with a low down payment. The cost of PMI depends on various factors, including the loan amount, down payment size, credit score, and mortgage type. It is typically paid monthly, added to the borrower's mortgage payment, but can also be paid upfront or through a combination of upfront and monthly payments. To avoid paying PMI, borrowers can aim for a 20% down payment or explore alternative loan options such as FHA or USDA loans, which have their own mortgage insurance requirements. Understanding the lender's PMI choices and calculating the total costs over different timeframes can help individuals make informed decisions when availing property mortgage insurance.

| Characteristics | Values |

|---|---|

| Who is it for? | Borrowers making a down payment of less than 20% of the purchase price of the home. |

| What does it do? | Lowers the risk to the lender of making a loan to you, so you can qualify for a loan that you might not otherwise be able to get. |

| Who does it protect? | The lender, not the borrower. |

| How much does it cost? | Private mortgage insurance (PMI) rates vary by down payment amount and credit score. |

| How is it paid? | PMI is usually paid monthly, with little or no initial payment required at closing. However, you may also have the option to pay for PMI upfront or through a combination of an upfront fee and a lower monthly premium. |

| Can it be cancelled? | Yes, once you've paid off some of your loan, you may be eligible to cancel your mortgage insurance. |

Explore related products

$4.99 $14.99

What You'll Learn

![]()

Private mortgage insurance (PMI)

The requirement to buy PMI usually applies when you refinance a conventional loan and your equity is less than 20% of the home's value. PMI is arranged by the lender and provided by private insurance companies. The cost of PMI depends on your loan, down payment size, interest rate, type of mortgage, and credit score. You can pay PMI monthly, upfront, or a combination of both.

Borrower-paid PMI is the most common type, where the insurance payment is added to your monthly mortgage payment. With lender-paid PMI, your lender pays for mortgage insurance upfront when you close your loan, and in return, you accept a higher interest rate on your mortgage.

You can request to cancel PMI when your mortgage balance reaches 80% of your home's value, or when you have paid off enough of your loan to reach 22% equity in your home. Federal law dictates that your lender must automatically end PMI when your loan-to-value (LTV) ratio drops to 78%, or halfway through your loan term.

Before agreeing to a mortgage, it is important to ask lenders about their PMI choices and compare different options to find the best deal.

Understanding Your True Worth: Insurance Estimation Explained

You may want to see also

Explore related products

![]()

FHA loans

When considering an FHA loan, it is important to ask the lender about their specific requirements and how they handle mortgage insurance. Lenders might offer different options, so it is beneficial to calculate the total costs over different timeframes to determine the best deal.

When to Report Accidents to Your Insurance Company

You may want to see also

Explore related products

![]()

Cancelling your mortgage insurance

Types of Mortgage Insurance

There are two main types of mortgage insurance: Private Mortgage Insurance (PMI) and Mortgage Protection Insurance. PMI is the most common type and is solely for the lender's protection. It reimburses the lender if you default on your mortgage payments. With PMI, your insurance payment is typically added to your monthly mortgage payment. Mortgage Protection Insurance, on the other hand, continues to cover your mortgage payments after your death, protecting your family members from foreclosure.

When to Cancel

You can typically cancel your PMI when you have paid down your mortgage to a specified point, usually when you reach 20% equity in your home. At this point, your lender may automatically cancel your PMI, or you may need to submit a written request for cancellation. If you have a multi-unit primary property or investment property, the requirements for cancellation may vary. For example, Fannie Mae allows cancellation at 30% equity, while Freddie Mac requires 35% equity.

How to Cancel

To cancel your PMI, you must be current on your mortgage payments and have an appraisal to verify the current property value. You may also want to consider refinancing your mortgage, especially if you have other high-interest debt. By consolidating your debt into a new home loan, you may be able to reduce your monthly payments significantly.

Saving Money

Endurance Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![]()

How it impacts monthly payments

When it comes to property mortgage insurance, there are a few different types to consider, each impacting your monthly payments differently. The type of insurance you'll need will depend on the type of loan you take out and the size of your down payment. Here's how each type of insurance impacts your monthly payments:

Private Mortgage Insurance (PMI)

PMI is typically required when you take out a conventional loan with a down payment of less than 20% of the purchase price of the property. PMI rates vary by down payment amount and credit score but are generally cheaper for borrowers with good credit. The premium for PMI is added to your monthly mortgage payment. This type of insurance protects the lender if you fail to make your mortgage payments and can help you qualify for a loan you might not otherwise get approved for. However, it's important to note that PMI does not protect you; you can still lose your home through foreclosure if you fall behind on payments.

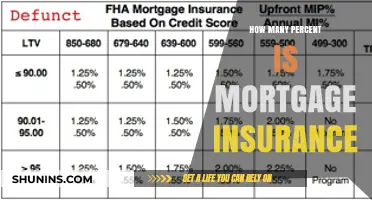

Federal Housing Administration (FHA) Mortgage Insurance

FHA mortgage insurance is required for all FHA loans. It includes an upfront cost, paid as part of your closing costs, and a monthly cost included in your monthly payment. FHA insurance costs the same regardless of your credit score, with a slight increase for down payments of less than 5%. Like PMI, FHA insurance protects the lender, not you.

U.S. Department of Agriculture (USDA) Loan Insurance

The USDA loan program is similar to the FHA program but typically cheaper. With a USDA loan, you pay for insurance at closing and as part of your monthly payment. Like FHA loans, you can roll the upfront cost into your mortgage, but this increases your overall loan amount and costs.

Department of Veterans' Affairs (VA)-Backed Loans

With VA-backed loans, there is no monthly mortgage insurance premium. Instead, you pay an upfront "funding fee," which can be rolled into your mortgage, increasing your overall costs.

Cancelling Mortgage Insurance

It's important to note that you may be able to cancel your mortgage insurance once you've paid off a certain amount of your loan, which will reduce your monthly payments. The requirements for cancelling mortgage insurance vary depending on the type of property and the loan provider.

In summary, property mortgage insurance is an added expense that increases the overall cost of your loan. The impact on your monthly payments will depend on the type of insurance, the size of your down payment, and your credit score. By understanding these factors, you can make informed decisions about your mortgage and choose the option that best suits your financial situation.

Genetic Testing: Insurance Risks and Rewards

You may want to see also

Explore related products

![]()

Lender-paid vs borrower-paid PMI

Lender-paid mortgage insurance (LPMI) and borrower-paid mortgage insurance (BPMI), also known as private mortgage insurance (PMI), are two types of mortgage insurance that protect the lender if the borrower defaults on their loan. The key difference between the two is who pays for the mortgage insurance costs. With LPMI, the lender pays the insurance costs upfront, resulting in a higher interest rate for the borrower. On the other hand, BPMI or PMI is paid by the borrower directly as a monthly charge added to their mortgage payment.

LPMI can be a good option for those who want to lower their monthly mortgage payments. By choosing LPMI, borrowers may qualify for a higher mortgage amount as it reduces their projected debt-to-income ratio. Additionally, LPMI may be tax-deductible if the borrower itemizes deductions. However, it's important to note that LPMI cannot be removed from the loan, even when the borrower reaches 20% equity in their home. The higher interest rate associated with LPMI remains for the life of the loan, potentially resulting in higher costs in the long run.

On the other hand, BPMI or PMI provides borrowers with more flexibility. It can be paid monthly or as a lump sum at closing. This type of mortgage insurance is typically required for conventional loans with down payments under 20%. Borrowers can request PMI cancellation once they have at least 20% equity in their home. Additionally, BPMI offers the potential for a refundable rate, which is not available with LPMI.

The choice between LPMI and BPMI/PMI depends on various factors, including the lender's policies, available loan products, and market conditions. It's important to consider the advantages and disadvantages of each option, such as short-term and long-term costs, tax implications, and the impact on monthly payments. By comparing the differences between LPMI and BPMI/PMI, borrowers can make an informed decision that aligns with their financial goals and circumstances.

To avail of property mortgage insurance, individuals can connect with loan officers or mortgage specialists who can guide them through the different options and help them assess their eligibility. It is essential to carefully review the terms and conditions of the loan and insurance products to make a well-informed decision.

FHA Loan Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Mortgage insurance lowers the risk to the lender of loaning money to the borrower. This means that the borrower may qualify for a loan that they might not otherwise be able to get. Mortgage insurance is required for borrowers who take out a conventional loan with a down payment of less than 20% of the purchase price.

Private Mortgage Insurance (PMI) is solely for the lender's protection. It reimburses the lender if the borrower defaults on their mortgage payments. FHA mortgage insurance, on the other hand, is required for all Federal Housing Administration (FHA) loans. It costs the same regardless of your credit score, with a slight increase for down payments of less than 5%.

You can request to cancel your PMI when your mortgage balance reaches 80% of your home's value, or once you have achieved 20% equity in your home. For FHA loans, cancellation is more complicated and may involve refinancing.

With borrower-paid PMI, the insurance payment is added to your monthly mortgage payment. You may also have the option to pay upfront or through a combination of upfront and monthly fees. With lender-paid PMI, the lender pays the insurance with a lump sum and the borrower pays a higher interest rate on the loan.

To avail of property mortgage insurance, you must speak to your lender about your options. Lenders might offer you more than one option, so it is important to ask for detailed pricing for different options.