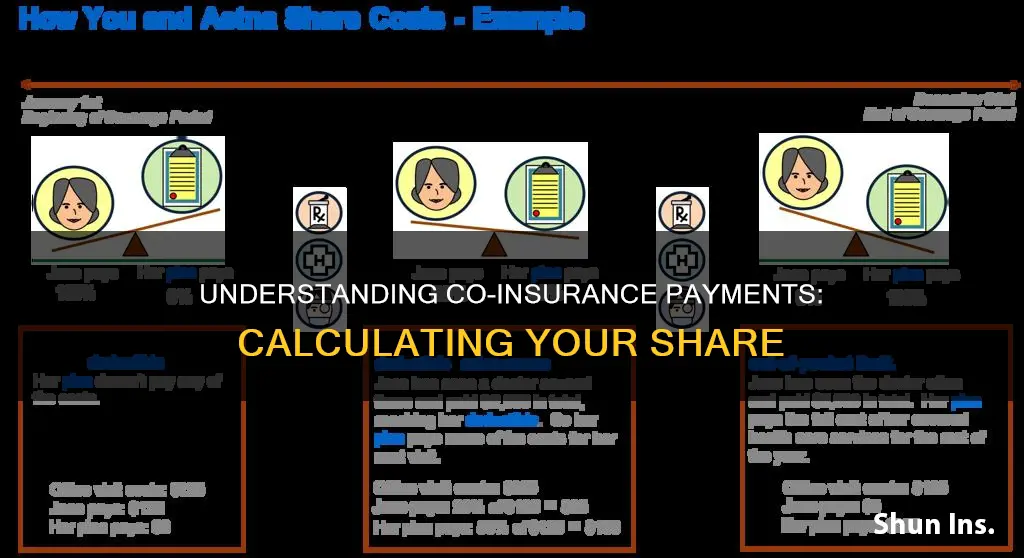

Coinsurance is a type of out-of-pocket cost that you may need to pay for healthcare services, and it's important to understand how to calculate your coinsurance payment to know how much you'll owe and budget for it. Coinsurance is the percentage of covered health costs you're responsible for paying after meeting your deductible, and it operates on a fixed ratio, meaning you'll always be charged the same percentage of the total bill each time. To calculate your coinsurance payment, you need to first determine the total cost of the healthcare service received and then convert your coinsurance rate into a decimal figure. You can then calculate the coinsurance penalty by dividing the amount of current insurance coverage by the required insurance amount and multiplying that result by the cost of repair or loss.

| Characteristics | Values |

|---|---|

| Coinsurance calculation | The percentage of covered health costs you're responsible for paying after meeting your deductible |

| Coinsurance penalty | A reduction in payout due to insufficient coverage |

| Coinsurance and copayments | Copayments are fixed amounts, whereas coinsurance payments vary depending on the cost of the service |

| Coinsurance and deductibles | Deductibles are the initial amount you're required to pay before coinsurance kicks in |

| Coinsurance and out-of-pocket maximum | Once you meet your plan's annual out-of-pocket maximum, the insurance company is responsible for your healthcare costs |

| Coinsurance and in-network providers | If you use an in-network provider, your health plan has already negotiated discounts, and you calculate your coinsurance payment based on this discounted rate |

Explore related products

What You'll Learn

![]()

Understanding co-insurance, co-pays, and deductibles

Co-insurance refers to the percentage of a medical charge that you pay after meeting your deductible. For example, if you have 20% co-insurance, you'll pay 20% of each medical bill, while your health insurance plan covers the remaining 80%total cost of the healthcare service received and your co-insurance rate. If you use an in-network provider, your health plan may have already negotiated discounts, and you'll calculate your co-insurance payment based on this discounted rate.

Co-pays, or co-payments, are fixed amounts that you pay for specific health services, such as doctor visits or filling a prescription. A co-pay is typically a predetermined rate that you pay at the time of service, regardless of the total bill for the office visit or prescription.

Deductibles, on the other hand, are separate from the monthly premiums you pay. Once you've met your deductible, you continue paying your monthly premium, but your medical costs are covered, excluding any co-pay or co-insurance charges. Deductibles represent the amount you need to pay before your insurance company starts contributing to your healthcare costs.

It's important to note that your health insurance plan may include both co-pays and deductibles, and whether you pay one or the other depends on the specific services you receive. Understanding these terms and how they work together can help you anticipate your financial responsibility when seeking healthcare services.

Insurance Expiry: How to Stay Alert and Avoid Lapses

You may want to see also

Explore related products

![]()

How to calculate your health insurance co-insurance payment

Coinsurance is the percentage of covered health costs that you are responsible for paying after you've met your deductible. It is important to understand how to calculate your health insurance coinsurance payment so that you know how much you will owe and can budget for it.

Firstly, you need to determine the total cost of the healthcare service you received. If you are using an in-network provider, your health plan will have already negotiated discounts from that provider. You will then calculate your health insurance coinsurance payment based on the discounted rate, not the standard rate charged to people who don't belong to your health plan.

Secondly, you need to convert your coinsurance percentage into a decimal figure. For example, if the coinsurance percentage is 20%, the decimal figure is 0.20.

Finally, multiply the total cost of the healthcare service by the decimal figure. For example, if the total cost of the healthcare service is $100 and the coinsurance percentage is 20% (0.20), the coinsurance payment would be $20.

It is worth noting that coinsurance payments contribute to your out-of-pocket maximum. Once you meet your plan's annual out-of-pocket maximum in medical bills, the insurance company will be responsible for your healthcare costs.

Chapter 7: Insurance Payments and Exemptions

You may want to see also

Explore related products

![]()

Converting your co-insurance percentage into a decimal figure

When calculating your health insurance coinsurance payment, you must first determine the total cost of the healthcare service received. This is because coinsurance is a percentage of the total cost for the service, so you'll owe a different amount for each service.

To calculate the coinsurance you owe, you first need to convert your co-insurance percentage figure into a decimal figure. You can do this by moving the decimal point two spaces to the left. For example, 35% becomes 0.35.

Once you have the decimal figure, you multiply this by the network-approved amount for the service. This will give you the coinsurance amount you owe. It's important to note that this calculation is based on the network-approved price, not the amount initially billed by the medical provider.

For example, let's say Antoine's health plan requires 20% cost-sharing to fill a prescription. The network-approved cost of the prescription is $100. To calculate Antoine's coinsurance payment, we first convert 20% to a decimal, which is 0.20. Then, we multiply this by the network-approved cost: 0.20 x $100 = $20. So, Antoine's coinsurance payment for this prescription is $20.

It's worth noting that some health plans have different coinsurance rates for various services. For instance, you might have a 35% coinsurance rate for hospitalization but only a 20% coinsurance rate for surgery at an outpatient surgery center.

Salvage Titles: What Insurance Companies Know

You may want to see also

Explore related products

![]()

Coinsurance penalties and payouts

Coinsurance clauses are most commonly found in commercial property insurance or inland marine insurance policies. They are designed to encourage individuals to insure their assets for an appropriate value. When a loss occurs, and the purchased insurance coverage falls short of the required amount, a coinsurance penalty may be applied, and the insurer is only obligated to cover a portion of the loss.

Coinsurance penalties are dependent on the coinsurance percentage stipulated in the contract, which is usually 80% or 90% but can vary. The penalty is calculated based on the ratio of the purchased coverage to the required amount, which can significantly reduce the payout to the policyholder. For example, if a policy with a 90% coinsurance provision aims to cover a property valued at $1,000,000, the property must be insured for a minimum of $900,000 to avoid a coinsurance penalty.

To calculate the coinsurance penalty, the actual insurance coverage amount is divided by the required insurance coverage amount, and this figure is multiplied by the loss amount. For instance, if the actual insurance coverage amount is $600,000 and the required insurance coverage amount is $800,000, the policyholder would receive $75,000 on a $100,000 claim ($600,000 / $800,000 x $100,000). If the policyholder had maintained the required coverage amount, they would have received the full amount of the claim without penalty.

It is important to note that coinsurance in homeowners' insurance is different from medical insurance. In medical insurance, the insurance company typically pays a set percentage of the loss, and the individual is responsible for the remaining percentage. In homeowners' insurance, the term "coinsurance" is not commonly used, and the concept is referred to as an "insured to value" clause. This clause requires the homeowner to insure their home for an amount of no less than 80% of the home's replacement cost value.

Driving Record Insurance Checks: How Far Back Do They Go?

You may want to see also

Explore related products

![]()

Co-insurance for home insurance

Co-insurance is a clause in your home insurance policy that specifies the minimum amount of insurance that should be maintained on the property. It is calculated as a percentage of the total value of the insured property.

When a loss occurs, and the purchased insurance coverage falls short of the required amount, a coinsurance penalty may be applied. In such cases, the insurer is only obligated to cover a portion of the loss. This penalty is calculated based on the ratio of the purchased coverage to the required amount, which can significantly reduce the payout to the policyholder. For example, if the value of the building at the time of loss is $100,000 and the coinsurance percentage is 90%, the limit of insurance should be at least $90,000. If the amount of insurance purchased is only 50% of the amount required, coverage is afforded for only 50% of the repair cost.

Home insurance provides financial protection against damage to your home and many permanent structures on your property. This includes damage from fire, smoke, wind, falling trees, hail, and theft. Personal Property coverage protects belongings that have been damaged or stolen, such as furniture, appliances, clothing, and electronics. Personal Liability coverage protects against damage to others caused by you or members of your household, including most pets. This can include medical expenses or property damage, and it could also help with legal expenses in the case of a lawsuit.

Is Your Vehicle Insured? How to Check in the UK

You may want to see also

Frequently asked questions

Coinsurance is the percentage of covered health costs you're responsible for paying after you've met your deductible.

Copay is a fixed amount you pay every time you fill a prescription or see your care provider. On the other hand, coinsurance is a percentage of the total bill and is paid only after the insurance approves the charges.

To calculate your coinsurance payment, first, convert your coinsurance percentage into a decimal figure by moving the decimal point two spaces to the left. Then, multiply that decimal figure by the total cost of the healthcare service you received.

Deductibles are the initial amount you're required to pay before coinsurance kicks in. For example, if you have a $2,000 deductible, you’re responsible for paying the full $2,000 for the year before your insurance will help cover a portion of the costs.

A coinsurance penalty is applied when the purchased insurance coverage falls short of the required amount. In such cases, the insurer is only obligated to cover a portion of the loss. The penalty is calculated based on the ratio of the purchased coverage to the required amount, which can significantly reduce the payout to the policyholder.