Calculating health insurance rates involves a complex process that takes into account various factors to determine the cost of coverage for individuals or groups. Insurance companies typically consider elements such as age, location, medical history, lifestyle choices, and the level of coverage desired when assessing risk and setting premiums. Understanding these components is essential for consumers to make informed decisions about their healthcare plans, as it allows them to anticipate costs, compare different policies, and select the most suitable option based on their needs and budget. By grasping the fundamentals of rate calculation, individuals can navigate the health insurance market more effectively and ensure they are adequately protected without overpaying.

Explore related products

What You'll Learn

- Demographics and Lifestyle Factors: Age, location, smoking, occupation, and health habits influence premium calculations

- Coverage Level and Type: Higher coverage limits and comprehensive plans increase insurance rates significantly

- Policyholder Health History: Pre-existing conditions, medical claims, and family history impact rate assessments

- Deductibles and Copays: Choosing higher deductibles or copays can lower monthly premium costs

- Insurance Company Rating: Provider’s financial stability, claims processing, and customer service affect pricing strategies

![]()

Demographics and Lifestyle Factors: Age, location, smoking, occupation, and health habits influence premium calculations

Age is the cornerstone of health insurance premium calculations, with rates typically increasing as policyholders grow older. Insurers use actuarial tables to predict healthcare costs based on age groups. For instance, a 25-year-old might pay $200 monthly for a basic plan, while a 55-year-old could face premiums of $800 or more for similar coverage. This disparity reflects the higher likelihood of chronic conditions and medical interventions in older populations. To mitigate costs, younger individuals should consider high-deductible plans paired with health savings accounts (HSAs), while older adults may benefit from comprehensive plans with lower out-of-pocket maximums.

Location dramatically shapes health insurance rates due to variations in healthcare costs and state regulations. For example, urban areas like New York City or San Francisco often have higher premiums due to elevated medical service costs, while rural regions may offer lower rates but limited provider networks. Additionally, states with mandated coverage for specific services (e.g., fertility treatments in Massachusetts) tend to have higher average premiums. When relocating, policyholders should compare plans using state-specific marketplaces and consider the trade-offs between cost and access to care.

Smoking remains one of the most significant lifestyle factors affecting premiums, with smokers often paying 50% more than nonsmokers for the same coverage. Insurers view smoking as a high-risk behavior linked to chronic illnesses like heart disease and cancer. Some states allow tobacco surcharges of up to 50% of the base premium. Quitting smoking not only improves health but can also reduce insurance costs after 12 consecutive tobacco-free months. Programs like nicotine replacement therapy or counseling can aid cessation efforts, potentially saving hundreds annually in premiums.

Occupation and health habits intersect to influence premium calculations, as certain jobs carry higher health risks. For example, construction workers or firefighters may face elevated rates due to increased injury risks, while desk-bound professionals might see premiums rise if their sedentary lifestyle contributes to obesity or diabetes. Employers can offset these costs by offering wellness programs that incentivize healthy behaviors, such as gym memberships or smoking cessation support. Individuals in high-risk occupations should prioritize preventive care and consider supplemental insurance to cover job-related injuries.

Health habits, such as diet, exercise, and preventive care utilization, play a subtle but critical role in premium calculations. Insurers increasingly use wearable technology data (e.g., Fitbit or Apple Watch) to offer discounts to policyholders who meet activity benchmarks. For example, walking 10,000 steps daily or maintaining a healthy BMI could reduce premiums by 10-15%. Similarly, regular check-ups and screenings can prevent costly treatments later, indirectly lowering long-term insurance costs. Policyholders should leverage wellness incentives and proactively manage their health to optimize both well-being and insurance expenses.

Understanding Grace Periods in Medical Insurance Coverage

You may want to see also

Explore related products

![]()

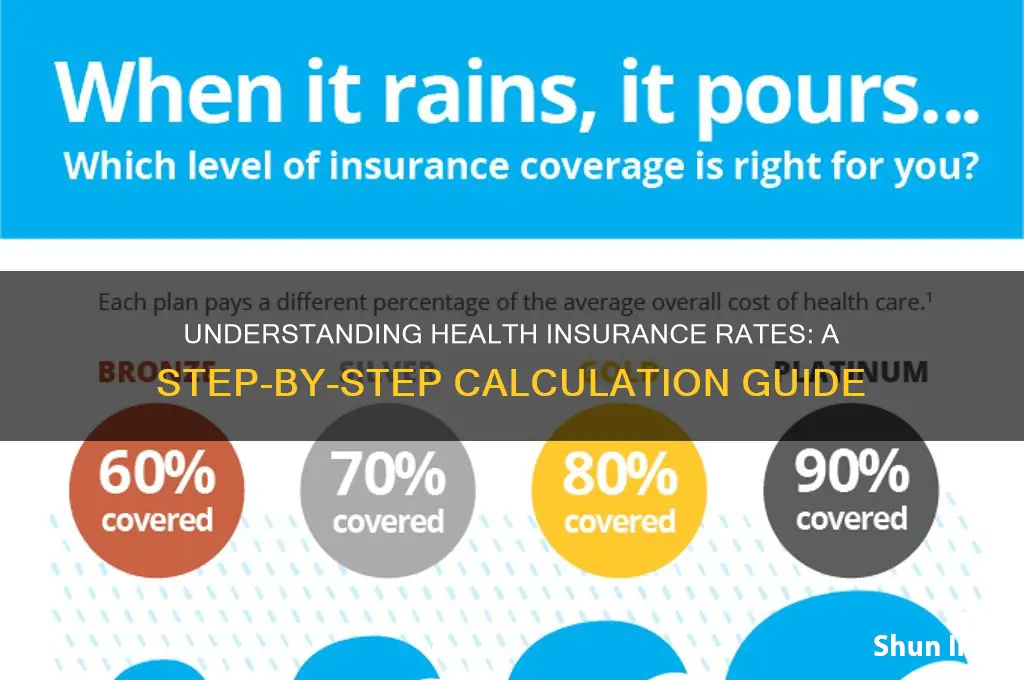

Coverage Level and Type: Higher coverage limits and comprehensive plans increase insurance rates significantly

The coverage level and type you choose are pivotal in determining your health insurance rates. Opting for higher coverage limits means the insurer assumes greater financial risk, which translates into higher premiums. For instance, a plan with a $1 million lifetime maximum will cost more than one with a $500,000 cap. Similarly, comprehensive plans that cover a wide range of services—such as preventive care, specialist visits, mental health, and prescription drugs—demand higher premiums compared to basic plans that only cover hospitalization and emergency care. Understanding this trade-off between coverage breadth and cost is essential for tailoring a plan to your needs and budget.

Consider the example of a 35-year-old nonsmoker in California. A basic plan with a $6,000 deductible and 70% coinsurance might cost around $300 monthly, while a comprehensive plan with a $1,500 deductible, 90% coinsurance, and added benefits like dental and vision could double the premium to $600. The difference lies in the insurer’s liability: the comprehensive plan covers more services at higher rates, increasing their potential payout. This example illustrates how coverage level and type directly correlate with premium costs, making it crucial to evaluate which benefits are worth the added expense.

When selecting coverage, analyze your health needs and financial situation. If you’re generally healthy and rarely visit the doctor, a high-deductible plan with lower premiums might suffice. However, if you have chronic conditions or a family history of illness, investing in a comprehensive plan could save you money in the long run by reducing out-of-pocket costs. For instance, a diabetic individual would benefit from a plan that covers regular specialist visits, insulin, and monitoring devices, even if it means paying higher monthly premiums.

A practical tip is to use online calculators or consult an insurance broker to compare plans. Input your age, location, and health status to see how coverage levels affect premiums. For example, increasing your deductible from $1,000 to $3,000 could reduce your monthly premium by 15–20%, but ensure you have savings to cover the higher out-of-pocket costs if needed. Additionally, check if your employer offers group plans, which often provide comprehensive coverage at discounted rates due to pooled risk.

In conclusion, higher coverage limits and comprehensive plans significantly increase insurance rates because they expand the insurer’s financial responsibility. By carefully assessing your health needs and financial capacity, you can strike a balance between robust coverage and affordability. Remember, the goal is not to pay the least but to ensure you’re adequately protected without overpaying for unnecessary benefits.

Medicare and Aetna: Can You Have Both?

You may want to see also

Explore related products

![]()

Policyholder Health History: Pre-existing conditions, medical claims, and family history impact rate assessments

Health insurance rates are not arbitrary; they are meticulously calculated based on a variety of factors, with policyholder health history playing a pivotal role. Among the most influential elements are pre-existing conditions, medical claims, and family history. These factors provide insurers with a snapshot of an individual’s health risks, directly impacting the premiums they pay. For instance, a 45-year-old with a history of hypertension and diabetes will likely face higher rates than a peer with no chronic conditions, as these pre-existing conditions signal a higher likelihood of future medical expenses.

Pre-existing conditions are a cornerstone of rate assessments because they represent ongoing or recurring health issues that require continuous management. Insurers analyze the type, severity, and treatment costs associated with these conditions. For example, a policyholder with well-managed asthma may see a moderate increase in premiums, while someone with uncontrolled type 2 diabetes requiring insulin therapy could face significantly higher rates. The key takeaway is that the more complex or costly the condition, the greater its impact on insurance rates. Policyholders can mitigate this by maintaining detailed records of their health management efforts, such as regular check-ups or adherence to prescribed treatments, which may demonstrate lower risk to insurers.

Medical claims history is another critical factor, as it reflects past healthcare utilization and potential future needs. Insurers scrutinize the frequency, nature, and cost of claims to predict future behavior. A policyholder who files multiple claims annually for emergency room visits or specialist consultations will likely be assessed as higher risk compared to someone with minimal claims. Interestingly, even claims for preventive care, such as annual physicals or vaccinations, can influence rates. While these services are generally encouraged, frequent use may signal underlying health concerns. To optimize rates, policyholders should focus on preventive care while minimizing unnecessary claims, such as opting for telemedicine consultations for minor ailments instead of in-person visits.

Family medical history adds another layer to rate assessments, particularly for conditions with strong genetic links. Insurers often inquire about familial occurrences of diseases like cancer, heart disease, or Alzheimer’s, especially if they affected first-degree relatives at an early age. For example, a 30-year-old with a parent diagnosed with colorectal cancer at 40 may face higher premiums due to the increased hereditary risk. However, this factor is often balanced against other health indicators. Policyholders can proactively address this by undergoing recommended screenings or genetic testing, which may provide insurers with reassurance about their health management strategies.

In conclusion, policyholder health history is a multifaceted determinant of health insurance rates, with pre-existing conditions, medical claims, and family history each contributing uniquely. By understanding these factors and taking proactive steps—such as managing chronic conditions, optimizing claims behavior, and staying informed about familial risks—individuals can potentially influence their rate assessments. While insurers rely on these data points to calculate premiums, policyholders are not powerless; informed decisions and preventive actions can lead to more favorable outcomes.

Step-by-Step Guide to Applying for Maxicare Health Insurance Easily

You may want to see also

Explore related products

![]()

Deductibles and Copays: Choosing higher deductibles or copays can lower monthly premium costs

Health insurance premiums are a balancing act between monthly affordability and out-of-pocket costs when you need care. One powerful lever in this equation is your choice of deductibles and copays. Opting for higher deductibles or copays directly reduces your monthly premium, but it shifts more financial risk to you when you use healthcare services. This trade-off demands careful consideration of your health status, budget, and risk tolerance.

Consider a 35-year-old individual choosing between two plans. Plan A has a $1,500 deductible and $20 copays for doctor visits, with a monthly premium of $350. Plan B raises the deductible to $3,000 and the copay to $30, lowering the premium to $250. If this person rarely visits the doctor and has no chronic conditions, the $100 monthly savings from Plan B could outweigh the risk of higher out-of-pocket costs. However, someone with frequent medical needs might find Plan A’s lower deductible and copays more cost-effective in the long run.

The key is to estimate your annual healthcare expenses. For instance, if you anticipate $1,000 in medical costs, Plan B’s higher deductible means you’d pay the full $1,000 out-of-pocket before insurance kicks in, plus the $250 premium savings. In contrast, Plan A’s lower deductible would cap your out-of-pocket costs at $1,500 (including premiums and copays). Tools like healthcare expense calculators can help you model these scenarios based on your expected usage.

A persuasive argument for higher deductibles is their alignment with Health Savings Accounts (HSAs). HSAs allow tax-free contributions to cover qualified medical expenses, making high-deductible plans more palatable. For example, contributing $2,000 annually to an HSA could offset Plan B’s deductible while offering tax advantages. This strategy is particularly appealing for healthy individuals or families who want to save for future medical expenses.

Ultimately, the decision hinges on your financial flexibility and health predictability. Higher deductibles and copays are a gamble—they save money if you stay healthy but can lead to unexpected costs if you need significant care. For those with stable health and emergency savings, this trade-off can be a smart way to reduce monthly expenses. However, individuals with chronic conditions or families with children may find lower deductibles and copays more secure, despite the higher premiums. Always weigh your options using concrete numbers and realistic health scenarios.

Report an Accident: Erie Insurance Claims Process

You may want to see also

Explore related products

![]()

Insurance Company Rating: Provider’s financial stability, claims processing, and customer service affect pricing strategies

Health insurance rates are not arbitrary; they are meticulously calculated based on a provider's financial stability, claims processing efficiency, and customer service quality. These factors directly influence pricing strategies, as insurers must balance risk, operational costs, and customer satisfaction. A financially stable insurer, for instance, can offer lower premiums because it has the reserves to handle large payouts without compromising its solvency. Conversely, a company with a history of delayed claims or poor customer service may need to charge higher rates to offset potential reputational damage and customer churn. Understanding these dynamics empowers consumers to evaluate plans beyond surface-level costs, ensuring they choose a provider that offers both affordability and reliability.

Consider claims processing efficiency as a critical metric. Insurers with streamlined systems can settle claims faster, reducing administrative costs and passing those savings onto policyholders. For example, companies that leverage AI and automation to process claims often have lower operational expenses compared to those relying on manual, paper-based systems. However, this efficiency must be balanced with accuracy; errors in claims processing can lead to disputes, legal fees, and increased costs. Consumers should look for providers with high claims settlement ratios and positive customer reviews regarding the ease and speed of the claims process. A 2023 study found that insurers with automated claims systems had a 30% faster resolution time, translating to lower premiums for policyholders.

Customer service quality is another pivotal factor in pricing strategies. Insurers with robust customer support—including 24/7 helplines, digital portals, and personalized assistance—often invest more in these services, which can slightly elevate premiums. However, this investment pays off in customer retention and loyalty, reducing acquisition costs over time. Poor customer service, on the other hand, can lead to higher churn rates, forcing insurers to continually spend on marketing and onboarding new clients. For instance, a provider with a 90% customer satisfaction rate may charge 5-10% more than competitors but retains 80% of its customers annually, compared to the industry average of 60%. This stability allows them to offer long-term discounts and rewards programs, ultimately benefiting policyholders.

Financial stability is perhaps the most straightforward yet critical aspect of insurance company ratings. Providers with high credit ratings from agencies like A.M. Best or Moody’s are better equipped to handle economic downturns, natural disasters, or sudden spikes in claims. These companies can afford to price their policies more competitively because they have lower risk exposure. For example, an insurer with an A++ rating (the highest possible) is statistically less likely to default on claims, making it a safer choice for consumers. However, this stability often comes at a premium, as these companies invest heavily in reserves and risk management. Consumers should weigh the added cost against the peace of mind and long-term reliability such providers offer.

In practice, consumers can use these insights to decode health insurance rates and make informed decisions. Start by checking an insurer’s financial rating through agencies like A.M. Best or Standard & Poor’s. Next, research their claims processing efficiency by reviewing annual reports or third-party evaluations. Finally, assess customer service quality through reviews, awards, and available support channels. For instance, a family of four might prioritize a provider with excellent customer service and fast claims processing, even if it means paying slightly higher premiums. Conversely, a young, healthy individual might opt for a more affordable plan from a financially stable insurer with average customer service. By aligning these factors with personal needs, consumers can secure a plan that offers the best value for their unique situation.

Understanding Your Medical Insurance Start Date

You may want to see also

Frequently asked questions

Health insurance rates are influenced by factors such as age, location, tobacco use, medical history, coverage level, and the type of plan chosen.

Younger individuals typically pay lower premiums because they are considered lower risk, while older individuals often pay more due to increased health risks and medical needs.

Yes, lifestyle choices like smoking or tobacco use can significantly increase premiums, as they are associated with higher health risks and medical costs.

Rates vary by location due to differences in healthcare costs, state regulations, local medical trends, and the availability of healthcare providers in the area.

Higher levels of coverage, such as lower deductibles or more comprehensive benefits, typically result in higher premiums, while lower coverage levels generally reduce costs.