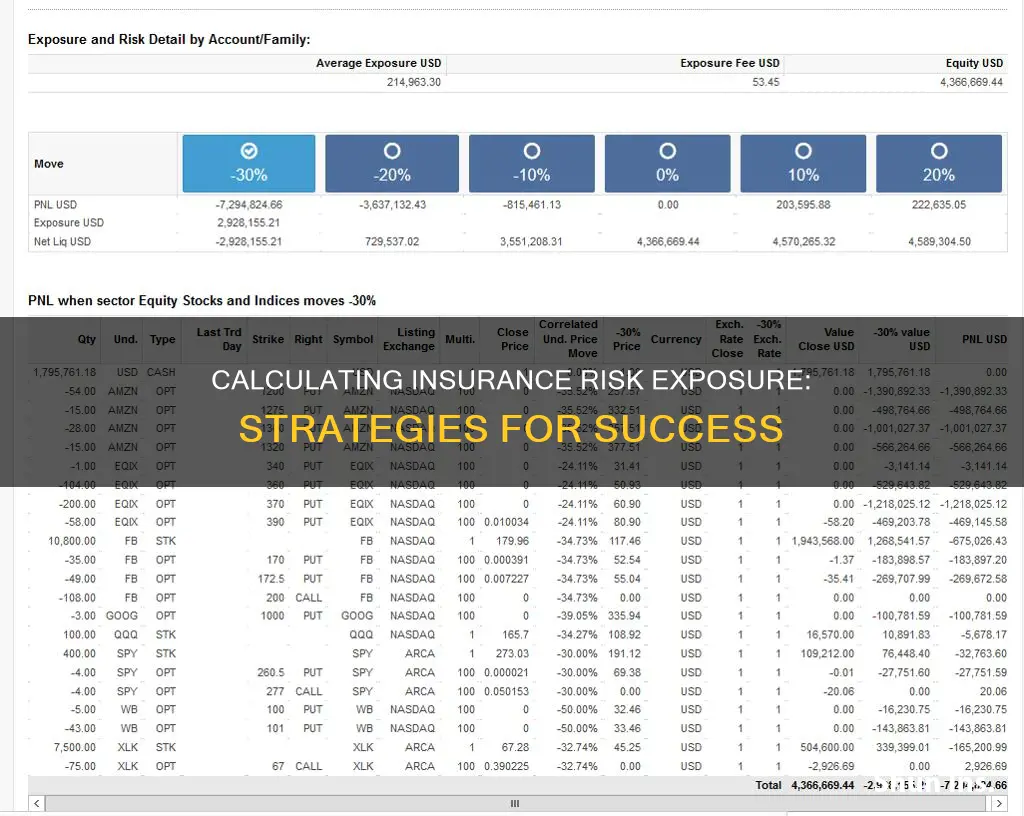

Risk exposure is a measure of an organization's vulnerability to risks and the potential losses or damages resulting from business activities and events. It is an essential concept in the insurance industry, where companies use exposure to determine rates for different classes of businesses or individuals. For example, in health insurance, the risk pool's average health care costs determine the premiums. Similarly, in other types of insurance, exposure rating is used to calculate risk exposure by examining the loss experience of similar risks to estimate potential losses. This helps insurance companies assess their risk exposure and set premiums accordingly.

| Characteristics | Values |

|---|---|

| Purpose | To determine the rates for each class of business |

| Basis | The total exposure associated with the policies issued during a policy term |

| Risk Calculation Methods | Exposure rating, experience rating method |

| Exposure Rating | Examining the loss experience of a portfolio of similar but not identical risks to estimate potential losses |

| Experience Rating Method | Examining historical loss data the company has experienced in association with a specific risk event |

| Risk Exposure Formula | Probability of Event x Expected Loss due to Risk Impact |

| Risk Impact | Financial, reputational, operational |

| Risk Exposure Calculation Steps | List all possible risks, determine the likelihood of each risk occurring, evaluate the potential impact of each risk, calculate expected loss, aggregate expected losses, consider correlations, adjust for mitigation measures, report and analyze |

| Risk Pooling | Combining the medical costs of a group of individuals to calculate premiums |

Explore related products

$39.57 $71.99

$19.13 $29.99

What You'll Learn

- Exposure rating: Examining similar risks to estimate potential losses

- Experience rating: Using historical loss data to assess risk

- Pure risk: Natural disasters or global pandemics

- Speculative risk: Choosing vulnerable software or susceptible backup systems

- Risk management: Avoidance, mitigation, transfer, and retention

![]()

Exposure rating: Examining similar risks to estimate potential losses

Exposure rating is a method used to calculate risk exposure in a reinsurance treaty. It is one of the two risk calculations used in the insurance industry, the other being the experience rating method.

The exposure rating method is used to calculate the potential losses of a client by examining the loss experience of a portfolio of similar, but not identical, risks. This method is particularly useful when the insurance company does not have sufficient historical data or credible claims history from the insured party.

For example, an insurance company may not have enough data on the risk of earthquakes in a particular region. In this case, they would examine the value of claims they covered for similar earthquakes in other regions. By adjusting the historical loss data, they can estimate the potential losses for the specific region in question.

The data generated from exposure rating will form an exposure curve. As you move along the curve, the cumulative loss as a percentage of insured value approaches 100%. This allows reinsurers to examine loss severity in layers and set prices for risks that are estimated to fall within each layer.

It is important to note that one disadvantage of the exposure rating method is the reliance on data from other insurers and third-party rating systems. This can create a zone in each layer where the losses approach but do not reach the next level of retention, requiring the use of distribution tables to set rates.

The Art of Damage Assessment: Unraveling the Insurance Adjuster's Process

You may want to see also

Explore related products

$68.6 $74.99

![]()

Experience rating: Using historical loss data to assess risk

Experience rating is a method used by insurance companies to determine premiums based on the historical loss data of individual policyholders. This approach incentivises policyholders with lower loss histories by offering reduced premiums, while those with higher loss histories pay higher premiums. Experience rating is most commonly associated with workers' compensation insurance but is also used across auto, general liability, and property insurance.

Experience rating is one of two risk calculations used in the insurance industry, the other being exposure rating. Reinsurers often use exposure rating when there is insufficient historical data to develop an experience rating. Exposure rating involves examining the loss experience of a portfolio of similar but not identical risks to estimate the potential losses of a client. The assumption is that risks in similar risk groups will display similar loss experiences.

Experience rating, on the other hand, involves adjusting historical loss data to account for changes in exposure, inflation, and claim settlement patterns. This process, known as loss development, is crucial in determining an accurate and reliable experience modification factor (EMF). The EMF is a numerical value that represents the policyholder's loss experience relative to the industry average. A higher EMF leads to higher premiums, while a lower EMF leads to lower premiums.

In addition to loss development, the experience rating process also involves data collection and analysis, trending, and credibility factors. Trending involves analyzing historical data to identify patterns and project future losses. Credibility factors weigh the importance of a policyholder's historical loss experience relative to the industry average. By considering these factors, experience rating helps insurance companies determine the likelihood that a particular policyholder will file a claim.

Avoid Overpaying for Insurance: Save Money, Avoid Pitfalls

You may want to see also

Explore related products

![]()

Pure risk: Natural disasters or global pandemics

Pure risk refers to the risk associated with natural disasters or global pandemics, which can have a significant impact on businesses and individuals alike. Unlike other types of risks, such as hurricanes, earthquakes, and wildfires, which are typically limited in scope and duration, pandemics can affect a vast number of people, regardless of their location, and can continue to cause economic losses for months or even years.

In the context of insurance, pure risk presents unique challenges due to its unpredictable and far-reaching nature. Insurers must consider the potential for litigation, regulation, and legislation that may compel them to pay claims on policies that were not originally intended to cover pandemics. This uncertainty makes it difficult to quantify the ultimate cost of pandemic-related claims.

To calculate insurance risk exposure for pure risk, insurers use exposure rating and experience rating methods. Exposure rating involves examining a portfolio of similar risks to estimate potential losses when sufficient historical data is lacking. This method helps determine the rates for each class of business, with higher-risk businesses facing higher premiums. On the other hand, experience rating relies on historical loss data associated with specific risk events, allowing insurers to set prices based on the estimated frequency and severity of losses.

In the case of natural disasters, such as earthquakes, insurers can utilise their historical experience to adjust data and estimate future losses. However, with global pandemics, the lack of historical data and the unprecedented nature of the risk make it challenging to calculate exposure accurately. As a result, insurers may be reluctant to provide coverage for economic losses caused by pandemics, and the availability of private insurance in this area remains limited.

To address the challenges posed by pure risk, innovative insurance products, such as parametric insurance and specialised pandemic risk coverage, have emerged. Parametric insurance, which pays out based on the hazard of the disaster as defined in the contract, simplifies claims management and reduces administrative burdens. Meanwhile, products like PathogenRX, developed by global reinsurers and epidemic risk management companies, aim to provide dedicated coverage for pandemic-related risks.

Unraveling the Path to Becoming a Catastrophic Insurance Adjuster

You may want to see also

Explore related products

![]()

Speculative risk: Choosing vulnerable software or susceptible backup systems

Speculative risk refers to the potential for loss that arises from uncertain events. In the context of choosing vulnerable software or susceptible backup systems, the speculative risk is the potential for loss or damage due to insecure software or backup systems that can be exploited by malicious actors.

Software vulnerabilities can arise from various factors, including insecure data storage practices, unauthorized access to device sensors, and malware infiltration through app stores. For example, the Speculative Store Bypass (CVE-2018-3639) is a vulnerability that affects Intel processors, allowing a malicious actor to access stale data values. By exploiting this vulnerability, an attacker could gain unauthorized access to sensitive information.

To mitigate the speculative risk associated with vulnerable software, organizations should implement robust security measures. This includes performing regular vulnerability scans to identify potential weaknesses in their systems and applications. Additionally, organizations should follow best practices such as enabling speculative store bypass disable (SSBD) on processors and inserting register dependencies to prevent malicious attacks.

Backup systems are also vulnerable to speculative risk. On-site backups, cloud backups, and tape backups are all susceptible to unauthorized access, malware, and other cyber threats. To reduce the risk of data loss or breach, organizations should implement comprehensive backup strategies that include encryption, access controls, and offline storage of encryption keys.

Additionally, the frequency of backups plays a crucial role in mitigating speculative risk. A shorter Recovery Point Objective (RPO) between backups reduces the risk of data loss, but it also increases costs and requires more frequent backups. Organizations must carefully consider their data change rate and implement an optimal backup schedule to balance these factors effectively.

Insurance Gain: An Asset or Not?

You may want to see also

Explore related products

$41.11 $54.99

![]()

Risk management: Avoidance, mitigation, transfer, and retention

Risk management is a critical aspect of any business, and it involves various strategies such as avoidance, mitigation, transfer, and retention. Each strategy plays a unique role in safeguarding organisations from potential threats and their impact.

Risk avoidance, as the name suggests, involves steering a company away from potential hazards. It is a conservative approach, as it sacrifices potential benefits to eliminate danger. This strategy is particularly useful when a company wants to completely sidestep situations that could result in losses. For instance, a company might avoid a specific supplier with a history of quality issues, thus removing any possibility of problems related to that vendor. While risk avoidance can be highly effective, it may not suit every business, as it can be challenging to implement and may decrease efficiency during the transition.

Risk mitigation is a more balanced approach, where potential hazards are weighed against potential benefits, and measures are implemented to manage issues if they arise. This strategy aims to reduce the likelihood of risks occurring and to minimise their impact. A comprehensive risk mitigation plan involves a team of people, processes, and technology. It requires identifying and evaluating risks, prioritising them, and implementing and monitoring the established plan. Regular testing and analysis are crucial to ensure the plan remains up to date and compliant with regulations.

Risk transfer is a common strategy where the potential loss is shifted to a third party, such as an insurance company. In exchange for bearing the risk, the third party typically receives periodic payments or insurance premiums. This is a useful method for individuals or entities to protect themselves from financial risks. For example, purchasing car insurance transfers the risk of financial loss from traffic incidents to the insurance company.

Risk retention is a strategy where an organisation assumes responsibility for a certain level of risk or losses. It helps manage overall risk exposure and is a cost-effective way to limit financial losses. The amount of risk retained is determined by the organisation's tolerance for risk before transferring the excess to another party through insurance or other risk transfer methods.

In conclusion, each risk management strategy serves a unique purpose in safeguarding businesses from potential threats. While risk avoidance seeks to eliminate dangers, risk mitigation focuses on reducing their likelihood and impact. Risk transfer involves shifting the burden to a third party, while risk retention entails assuming responsibility for a manageable level of risk. Organisations can employ these strategies individually or in combination to effectively manage their risk exposure.

Generic Insurance: Commercial Benefits for All

You may want to see also

Frequently asked questions

Risk exposure is the potential loss or damage resulting from business activities, operations, or risk events. It is the measurement of potential future loss due to a specific event or business activity.

Insurance companies use exposure to determine the rates for each class of business. They closely monitor the claims and losses that come from the policies that they underwrite to determine whether certain classes of policyholders are more prone to claims and are thus more risky to insure.

The formula for calculating risk exposure is: Risk Exposure = Probability of Event x Expected Loss. The expected loss is calculated by multiplying the probability of the risk event by its potential impact.

Risk exposure refers to the probability of a risk event occurring and the potential conditions under which it might materialize. Risk impact deals with the consequences of those adverse events if they occur, including the potential damage to the organization's finances, reputation, and operations.

Exposure rating is a procedure used to calculate risk exposure in a reinsurance treaty. It involves examining the loss experience of a portfolio of similar but not identical risks to estimate the potential losses of a client. The data from exposure rating generates an exposure curve, which allows the reinsurer to set prices for risks that fall within various layers.