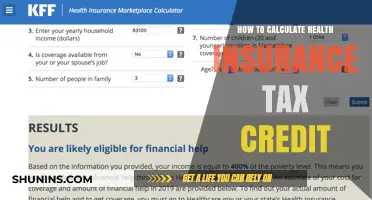

Calculating your health insurance tax can seem daunting, but it’s an essential step in understanding your financial obligations and potential savings. Health insurance tax, often tied to premiums or subsidies, varies based on factors like income, family size, and the type of plan you have. For individuals with employer-sponsored coverage, the tax implications may be minimal, as premiums are typically deducted pre-tax. However, for those purchasing plans through the marketplace, tax credits or deductions may apply, depending on your income level and whether you qualify for the Premium Tax Credit. To accurately calculate your health insurance tax, you’ll need to gather key documents, such as your income statements and insurance premium records, and use IRS guidelines or tax software to determine your liability or potential refund. Understanding these calculations ensures you maximize benefits while staying compliant with tax laws.

| Characteristics | Values |

|---|---|

| Taxable Income | Your total income subject to tax, including salary, wages, and other taxable earnings. |

| Filing Status | Single, Married Filing Jointly, Married Filing Separately, Head of Household. |

| Health Insurance Premiums | Total premiums paid for qualifying health insurance plans during the tax year. |

| Adjusted Gross Income (AGI) | Your total income minus certain deductions (e.g., student loan interest, IRA contributions). |

| Modified Adjusted Gross Income (MAGI) | AGI plus certain exclusions (e.g., foreign earned income, tax-exempt interest). |

| Premium Tax Credit (PTC) | A refundable tax credit for individuals and families with incomes between 100% and 400% of the Federal Poverty Level (FPL) who purchase insurance through the Marketplace. |

| Federal Poverty Level (FPL) | Income threshold used to determine eligibility for subsidies; varies by household size and state. |

| Employer-Sponsored Insurance | Premiums paid by your employer are generally tax-free; contributions to Health Savings Accounts (HSAs) may reduce taxable income. |

| Self-Employed Health Insurance Deduction | Self-employed individuals can deduct health insurance premiums from taxable income. |

| Itemized Deductions | Medical expenses exceeding 7.5% of AGI can be deducted if itemizing deductions. |

| ACA Individual Mandate Penalty | Repealed as of 2019; no federal penalty for not having health insurance. |

| State-Specific Mandates | Some states (e.g., California, New Jersey) have their own penalties for not having health insurance. |

| Tax Forms | Form 1040, Form 8962 (for Premium Tax Credit), Schedule A (for itemized deductions). |

| Tax Year | Calculations are based on the calendar year (January 1 - December 31). |

| IRS Guidelines | Follow IRS Publication 974 and instructions for Form 8962 for detailed calculations. |

| Professional Assistance | Consult a tax professional or use tax software for accurate calculations. |

Explore related products

What You'll Learn

- Understand Taxable Premiums: Identify which health insurance premiums qualify for tax deductions under IRS rules

- Use IRS Form 1040: Report deductible premiums on Schedule A of Form 1040 for itemized deductions

- Check Eligibility Limits: Ensure your medical expenses exceed 7.5% of AGI for tax deductions

- Employer-Sponsored Plans: Premiums paid pre-tax via employer plans are not deductible

- Self-Employed Deductions: Self-employed individuals can deduct health insurance premiums above the line

![]()

Understand Taxable Premiums: Identify which health insurance premiums qualify for tax deductions under IRS rules

Health insurance premiums can be a significant expense, but understanding which ones qualify for tax deductions can help you maximize your savings. The IRS allows deductions for certain health insurance premiums, but not all plans or payments meet the criteria. To start, self-employed individuals can typically deduct 100% of their health insurance premiums, including plans covering medical, dental, and long-term care. This deduction is claimed on Form 1040, reducing your taxable income directly. For example, if you’re self-employed and paid $6,000 in health insurance premiums last year, you could deduct the full amount, lowering your taxable income by $6,000.

For those with employer-sponsored plans, the landscape is different. Premiums paid through a workplace plan via payroll deductions are generally excluded from taxable income, meaning they’re already tax-free. However, if you pay additional premiums outside of this arrangement, such as for supplemental coverage, those payments may not qualify for a deduction unless they meet specific IRS criteria. For instance, premiums for a standalone vision or dental plan not included in your employer’s group plan might be deductible if you itemize deductions and your total medical expenses exceed 7.5% of your adjusted gross income (AGI) for tax year 2023.

Health Savings Account (HSA) contributions offer another avenue for tax savings. If you have a high-deductible health plan (HDHP), you can contribute to an HSA and deduct those contributions, up to $3,850 for individuals or $7,750 for families in 2023. These funds grow tax-free and can be used for qualified medical expenses, providing a triple tax advantage. However, not all plans qualify as HDHPs, so verify your plan’s eligibility before contributing. For example, a plan with a $1,500 deductible for an individual would not qualify, as the minimum deductible for an HDHP in 2023 is $1,500 with a maximum out-of-pocket limit of $7,500.

Lastly, be cautious of missteps that could disqualify your premiums from deductions. For instance, if you’re self-employed but also eligible for an employer-sponsored plan through a spouse’s job, you cannot deduct premiums for a separate individual plan. Similarly, premiums for life insurance, non-prescription medications, or general wellness programs typically do not qualify. Always consult IRS Publication 502 or a tax professional to ensure your premiums meet the specific rules for deductions, as misinterpretation could lead to errors or audits. By carefully identifying which premiums qualify, you can optimize your tax strategy and reduce your overall tax burden.

Medical Provider Suing Insurance Company: Is It Possible?

You may want to see also

Explore related products

![]()

Use IRS Form 1040: Report deductible premiums on Schedule A of Form 1040 for itemized deductions

Reporting health insurance premiums on your taxes can feel like navigating a maze, but IRS Form 1040 and Schedule A offer a clear path for those eligible to claim deductions. The key lies in understanding which premiums qualify and how to accurately report them.

Not all health insurance premiums are created equal in the eyes of the IRS. Only those paid with after-tax dollars, meaning from your own pocket and not through a pre-tax employer plan, are potentially deductible. This includes premiums for individual policies, family plans, and even long-term care insurance, provided they meet specific criteria.

Schedule A of Form 1040 is your deduction canvas. Line 1 of this schedule is dedicated to medical and dental expenses, including eligible health insurance premiums. It's crucial to remember that these deductions are subject to a threshold: you can only deduct expenses that exceed 7.5% of your adjusted gross income (AGI) for tax year 2023. This means if your AGI is $50,000, you can only deduct medical expenses, including health insurance premiums, that surpass $3,750.

Think of it as a hurdle you need to clear before your deductions take effect.

Accuracy is paramount when reporting on Schedule A. Gather all documentation related to your health insurance premiums, including payment receipts and policy details. Double-check the amounts and ensure they fall within the eligible categories. Mistakes can lead to delays in processing your return or even trigger an audit.

While navigating tax forms can be daunting, utilizing Schedule A to claim deductible health insurance premiums can result in significant savings. Remember, this is a targeted strategy for those with substantial medical expenses. If you're unsure about eligibility or have complex situations, consulting a tax professional is always advisable. They can provide personalized guidance and ensure you maximize your deductions while staying compliant with IRS regulations.

Naftin: Why Isn't Generic Covered by Insurance?

You may want to see also

Explore related products

![]()

Check Eligibility Limits: Ensure your medical expenses exceed 7.5% of AGI for tax deductions

Medical expenses can be a significant financial burden, but the IRS offers a silver lining: tax deductions. However, not all expenses qualify. A crucial threshold exists: your medical costs must surpass 7.5% of your Adjusted Gross Income (AGI) to be deductible. This means if your AGI is $50,000, your medical expenses need to exceed $3,750 to qualify.

Calculating this limit involves two key steps. First, determine your AGI, found on line 11 of your Form 1040. This figure represents your total income minus certain adjustments like student loan interest or IRA contributions. Second, tally your eligible medical expenses. This includes a wide range: doctor visits, prescriptions, hospital stays, insurance premiums (if self-employed), and even transportation to medical appointments.

It's important to note that only expenses paid during the tax year count, not those billed or incurred. Keep meticulous records – receipts, statements, and explanations for any unusual expenses. While exceeding the 7.5% threshold is necessary, it's not sufficient on its own. You must also itemize deductions on Schedule A of your tax return, foregoing the standard deduction.

STI Testing: What Does My Medical Insurance Cover?

You may want to see also

Explore related products

![]()

Employer-Sponsored Plans: Premiums paid pre-tax via employer plans are not deductible

Premiums paid through employer-sponsored health insurance plans on a pre-tax basis offer a significant financial advantage: they reduce your taxable income. This means you pay less in federal income tax and, in most cases, Social Security and Medicare taxes. However, this benefit comes with a trade-off. Since these premiums are already excluded from your taxable income, they cannot be claimed as a deduction on your tax return. Attempting to do so would result in double-dipping, allowing you to unfairly reduce your tax liability twice for the same expense.

Understanding this distinction is crucial for accurate tax planning.

Let's illustrate with an example. Imagine your annual salary is $60,000, and your employer-sponsored health insurance premium is $6,000. If you pay this premium pre-tax, your taxable income becomes $54,000. You're taxed on the lower amount, saving you money. However, you cannot then claim the $6,000 premium as a medical expense deduction on your tax return. The IRS considers it already accounted for in your reduced taxable income.

This rule applies to various employer-sponsored plans, including Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and High-Deductible Health Plans (HDHPs) paired with Health Savings Accounts (HSAs).

It's important to note that while pre-tax premiums themselves are not deductible, other qualified medical expenses might be. Expenses exceeding 7.5% of your adjusted gross income (AGI) can be deducted if you itemize deductions on Schedule A of Form 1040. This includes costs like deductibles, copays, prescription medications, and certain medical equipment. However, premiums paid pre-tax through your employer plan are explicitly excluded from this calculation.

Consulting a tax professional can help you navigate these complexities and ensure you're maximizing your deductions while adhering to IRS regulations.

Remember, the pre-tax treatment of employer-sponsored health insurance premiums is a valuable benefit, effectively lowering your overall tax burden. However, understanding the non-deductibility of these premiums is essential for accurate tax filing and avoiding potential penalties. By grasping this concept, you can make informed decisions about your healthcare coverage and tax strategy.

Will Your Insurance Company Sue You for Filing a Claim?

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UY218_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UY218_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UY218_.jpg)

![]()

Self-Employed Deductions: Self-employed individuals can deduct health insurance premiums above the line

Self-employed individuals often face unique financial challenges, but one significant advantage is the ability to deduct health insurance premiums "above the line" on their tax returns. This means the deduction reduces your adjusted gross income (AGI), potentially lowering your taxable income and overall tax liability. Unlike itemized deductions, which are limited and may not benefit all taxpayers, this deduction is available regardless of whether you itemize or take the standard deduction.

To qualify, the health insurance plan must cover medical care and be established under your business. This includes policies purchased through the Health Insurance Marketplace, COBRA coverage, or a spouse’s employer-sponsored plan if you’re eligible under their business. However, if you’re eligible for coverage under another employer’s plan (even if you don’t enroll), you can’t claim this deduction. For example, if your spouse’s employer offers you health insurance but you opt for a private plan, the deduction is disallowed.

Calculating the deduction requires careful attention to detail. First, ensure your premiums are solely for health insurance—dental, vision, or long-term care insurance don’t qualify unless bundled with a comprehensive health plan. Next, if your business has a net profit, you can deduct 100% of your premiums. However, if your business operates at a loss, the deduction is limited to your net profit from self-employment, and the excess can’t be carried over to future years. For instance, if your premiums are $6,000 annually but your business shows a $4,000 profit, your deduction is capped at $4,000.

A practical tip for maximizing this benefit is to time your premium payments strategically. If you’re close to the end of the tax year and expect a higher income, prepaying the next month’s premium could increase your current year’s deduction. Conversely, if you anticipate lower income next year, delaying payment until January might be advantageous. Always consult a tax professional to ensure compliance with IRS rules.

Finally, self-employed individuals should also consider Health Savings Accounts (HSAs) if they have a high-deductible health plan. While HSA contributions are a separate deduction, they work in tandem with health insurance premium deductions to reduce taxable income. For 2023, individuals can contribute up to $3,850, and families up to $7,750, with an additional $1,000 catch-up contribution for those over 55. Combining these strategies can significantly reduce your tax burden while ensuring comprehensive health coverage.

VA Medical Insurance: What Veterans Need to Know

You may want to see also

Frequently asked questions

The health insurance tax is a fee imposed on health insurance providers based on their market share, which may be passed on to consumers through higher premiums. Individuals do not calculate or pay this tax directly; it is handled by insurance companies.

Self-employed individuals can deduct health insurance premiums from their taxable income, reducing their overall tax liability. The calculation involves subtracting the premium amount from your adjusted gross income (AGI) on your tax return.

The ACA introduced subsidies and tax credits for eligible individuals purchasing health insurance through the Marketplace. To calculate these, use the IRS Form 8962, which compares your income to the federal poverty level and determines your eligibility for premium tax credits.

Health insurance premiums are tax-deductible if you itemize deductions and your medical expenses exceed 7.5% of your AGI (as of 2023). Self-employed individuals can deduct premiums directly, regardless of itemizing.

If you have health insurance, you’ll receive Form 1095-A (for Marketplace coverage), 1095-B, or 1095-C from your insurer. Report this information on your tax return to confirm compliance with the individual mandate or claim premium tax credits if applicable.

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UY218_.jpg)

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UY218_.jpg)