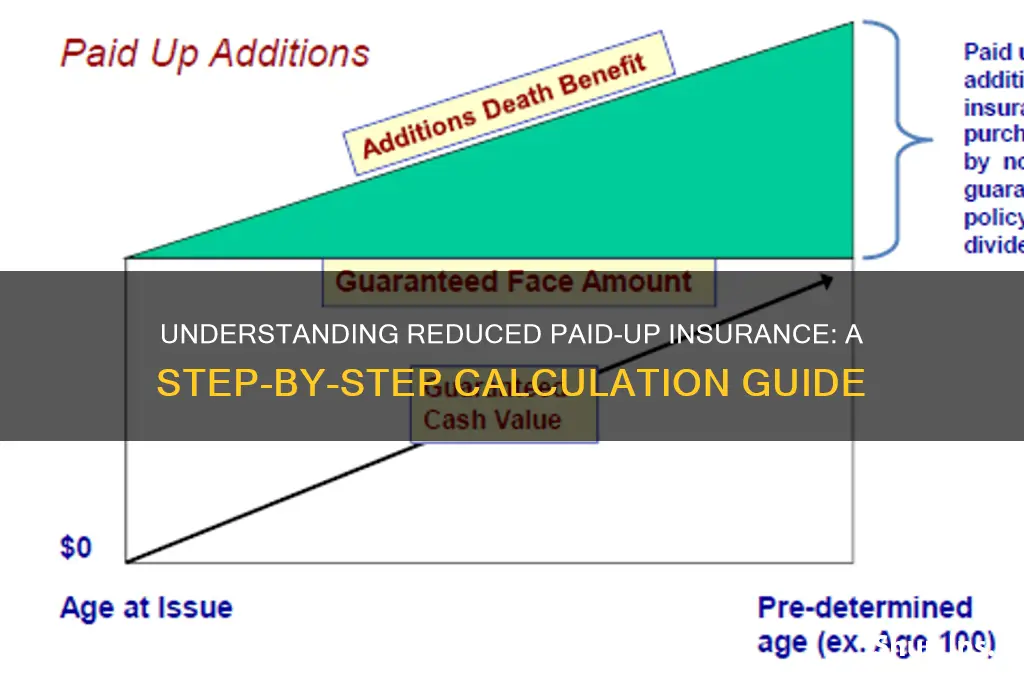

Reduced paid-up insurance is a valuable option available to policyholders who can no longer afford their life insurance premiums but wish to retain some coverage. This option allows the policyholder to stop paying premiums while keeping the policy active with a reduced death benefit. To calculate the reduced paid-up insurance amount, the insurer typically uses a formula based on the policy’s cash value and the original death benefit. The cash value accumulated in the policy is applied to purchase a smaller, permanent insurance benefit, ensuring continued coverage without further premium payments. Understanding this calculation is essential for policyholders to make informed decisions about their financial security and long-term planning.

| Characteristics | Values |

|---|---|

| Definition | A reduced paid-up insurance policy is a life insurance policy that continues with a reduced death benefit after the policyholder stops paying premiums. |

| Calculation Formula | Reduced Paid-Up Amount = (Original Face Amount) × (Ratio of Cash Value to Total Premiums Paid) |

| Key Factors | 1. Original Face Amount: The initial death benefit of the policy. 2. Cash Value: The accumulated savings component of the policy. 3. Total Premiums Paid: The cumulative premiums paid into the policy. |

| Purpose | Allows policyholders to retain some coverage without further premium payments. |

| Eligibility | Typically available for whole life or universal life policies with cash value. |

| Impact on Death Benefit | The death benefit is reduced proportionally based on the cash value and premiums paid. |

| Tax Implications | Generally no immediate tax consequences, as it’s a non-forfeiture option. |

| Policy Continuation | The policy remains in force with the reduced death benefit until the insured’s death. |

| Example | If a $100,000 policy has a cash value of $20,000 and total premiums paid of $40,000, the reduced paid-up amount would be $50,000 ($100,000 × ($20,000 / $40,000)). |

| Alternative Options | 1. Cash Surrender: Cancel the policy and receive the cash value. 2. Extended Term Insurance: Use the cash value to provide temporary coverage for a higher amount. |

| Policy Lapse Prevention | Acts as a safety net to prevent policy lapse due to missed premiums. |

Explore related products

What You'll Learn

![]()

Understanding Reduced Paid-Up Insurance

Reduced paid-up insurance is a lesser-known yet valuable option for policyholders facing financial strain. When premiums become unmanageable, this provision allows you to eliminate future payments while retaining a reduced death benefit. The calculation hinges on two key factors: the policy’s cash value and the original face amount. Essentially, the insurer uses the accumulated cash value to purchase a smaller, paid-up whole life policy, ensuring coverage continues without additional cost.

To calculate the reduced paid-up value, insurers typically apply a formula based on the policy’s cash surrender value and the original death benefit. For example, if a $250,000 whole life policy has a cash value of $50,000, the reduced paid-up amount might be calculated as a percentage of the original face value, proportional to the cash value. This results in a smaller, permanent benefit—say, $100,000—that remains in force without further premiums. The exact formula varies by insurer, but it generally ensures the cash value is sufficient to fund the reduced benefit over the policyholder’s lifetime.

One practical tip for policyholders is to review their policy’s cash value annually, especially as they approach retirement or face financial challenges. Knowing this value beforehand helps in making informed decisions about whether to exercise the reduced paid-up option. Additionally, compare this option with others like surrendering the policy for cash value or taking a policy loan, as each has distinct implications for your financial future.

A critical caution: reduced paid-up insurance is not a temporary solution. Once elected, the original policy terms, including the death benefit, are permanently altered. This option is best suited for those who no longer need high coverage but wish to retain some protection without ongoing costs. For instance, a 65-year-old retiree with grown children might find this option ideal, whereas a young family with dependents may need to explore alternatives.

In conclusion, understanding reduced paid-up insurance requires a clear grasp of its mechanics and implications. By focusing on the policy’s cash value and the insurer’s calculation method, policyholders can make a strategic decision that aligns with their long-term financial goals. It’s a powerful tool for preserving life insurance protection during times of financial hardship, but it demands careful consideration and proactive planning.

Public Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Calculating Cash Value for Reduced Paid-Up

Reduced paid-up insurance is a non-forfeiture option that allows policyholders to keep a smaller, permanent death benefit without further premiums. Calculating the cash value for this option requires understanding the policy’s accumulated cash value and how it translates into a reduced death benefit. The formula typically involves dividing the policy’s cash value by the net single premium for a single-life whole life insurance policy at the insured’s current age. For example, if a 50-year-old has a policy with a cash value of $20,000, the insurer calculates the net single premium for a new policy at age 50 and uses the cash value to purchase a smaller, paid-up policy.

The process begins with identifying the policy’s cash surrender value, which is the amount the insurer pays if the policy is surrendered. This value is then used to determine the reduced death benefit. For instance, if the cash value is $15,000 and the net single premium for a $50,000 death benefit at age 60 is $10 per $1,000 of coverage, the reduced paid-up benefit would be $15,000 ÷ $10 = $1,500 per $1,000, resulting in a $7,500 death benefit. This calculation ensures the policy remains in force without additional premiums, though at a lower coverage level.

A critical factor in this calculation is the insured’s age and the policy’s original terms. Younger policyholders may find the reduced benefit less appealing due to lower cash values, while older individuals with substantial cash accumulation may retain a meaningful death benefit. For example, a 70-year-old with a $50,000 cash value could secure a reduced paid-up benefit of $250,000 if the net single premium is $20 per $1,000. This highlights the importance of timing and policy maturity when considering this option.

Practical tips include reviewing the policy’s illustration to understand cash value growth and consulting an actuary or financial advisor to ensure accurate calculations. Policyholders should also compare this option with others, such as cash surrender or extended term insurance, to determine the best fit for their financial goals. For instance, if the cash value is $30,000 and the reduced paid-up benefit is $100,000, but the extended term option provides $200,000 in coverage for 10 years, the choice depends on whether immediate permanence or temporary higher coverage is preferred.

In conclusion, calculating cash value for reduced paid-up insurance involves precise steps tied to the policy’s cash value, the insured’s age, and the net single premium. By understanding these elements, policyholders can make informed decisions to maintain coverage without future premiums. This option is particularly valuable for those seeking permanent insurance with reduced financial burden, making it a strategic choice in long-term financial planning.

Contacting Publix Insurance Benefits: A Step-by-Step Guide for Employees

You may want to see also

Explore related products

![]()

Formula for Reduced Paid-Up Insurance

Reduced paid-up insurance is a non-forfeiture option that allows policyholders to keep their life insurance coverage without paying further premiums, albeit at a reduced benefit amount. The formula for calculating this reduced benefit is rooted in the relationship between the policy’s cash value and its original face value. At its core, the formula is: Reduced Paid-Up Amount = (Cash Value ÷ Original Premium) × Original Face Value. This equation ensures the benefit is proportionate to the premiums already paid and the policy’s accumulated cash value. For instance, if a policy has a $100,000 face value, a $20,000 cash value, and an annual premium of $2,000, the reduced paid-up amount would be $100,000 × ($20,000 ÷ $2,000) = $100,000 × 10 = $100,000. However, this example assumes a simplified scenario; real-world calculations often involve additional factors like policy duration and insurer-specific adjustments.

To apply this formula effectively, policyholders must first understand their policy’s cash value, which grows over time as premiums are paid. For example, a 40-year-old who has paid into a whole life policy for 10 years will likely have a higher cash value than someone who has paid for only 2 years. The cash value acts as the foundation for the reduced paid-up benefit, ensuring the policy remains active without further premium payments. However, the trade-off is a lower death benefit, which may require policyholders to reassess their coverage needs. For instance, a policy with a $500,000 face value and a $50,000 cash value might reduce to a $100,000 benefit, depending on the premium structure and insurer’s formula.

A critical caution when using this formula is that insurers may apply their own variations, often incorporating actuarial tables and policy-specific terms. For example, some insurers use a "net single premium" factor, which accounts for the policy’s remaining duration and interest rates. This can complicate the calculation, making it essential to consult the policy document or insurer directly. Additionally, policyholders should be aware that reduced paid-up insurance is not a one-size-fits-all solution. It is most beneficial for those who can no longer afford premiums but still require some level of coverage, such as retirees or individuals facing financial hardship.

In practice, the formula serves as a starting point, but real-world application requires careful consideration of individual circumstances. For instance, a 55-year-old with a $250,000 policy and a $30,000 cash value might opt for reduced paid-up insurance to maintain coverage without straining their budget. However, they should weigh this against alternatives like surrendering the policy for its cash value or converting it to a term policy. Ultimately, the formula for reduced paid-up insurance is a tool for preserving coverage, but its effectiveness depends on aligning it with the policyholder’s financial and life stage needs.

Does CPH Insurance Include Free Consultation? What You Need to Know

You may want to see also

Explore related products

![]()

Impact of Policy Duration on Calculation

The duration of an insurance policy significantly influences the calculation of reduced paid-up insurance (RPU), a benefit that keeps a policy active with a reduced death benefit when premiums are no longer paid. Longer policy durations generally result in higher cash value accumulation, which directly impacts the RPU amount. For instance, a 20-year policy will typically have a higher cash value compared to a 10-year policy of the same face amount, assuming identical premium payments and interest rates. This higher cash value translates to a larger RPU benefit, as the insurer uses the accumulated cash value to fund the reduced coverage.

To illustrate, consider a $100,000 whole life policy with annual premiums of $1,500. After 15 years, the cash value might reach $20,000. If the policyholder stops paying premiums, the RPU calculation would use this cash value to determine the new death benefit. A longer policy duration, such as 25 years, might yield a cash value of $35,000, resulting in a significantly higher RPU benefit. This example highlights how policy duration directly correlates with cash value growth and, consequently, the RPU amount.

When calculating RPU, insurers often apply a formula that considers the policy’s cash value, the original face amount, and the remaining duration. For shorter policies, the cash value may not be sufficient to sustain a meaningful RPU benefit, as the policy hasn’t had enough time to accumulate funds. Conversely, longer policies provide a buffer, allowing for a more substantial RPU benefit even if premiums cease. Policyholders should review their policy’s cash value projections to understand how duration affects their RPU potential.

A practical tip for maximizing RPU benefits is to opt for longer policy durations when purchasing insurance, especially if there’s a possibility of discontinuing premium payments in the future. For example, a 30-year policy will generally offer a more robust RPU benefit compared to a 15-year policy, assuming similar premium structures. Additionally, policyholders should monitor their cash value growth annually and consider partial withdrawals or loans cautiously, as these actions can reduce the available funds for RPU calculations.

In conclusion, policy duration plays a pivotal role in determining the reduced paid-up insurance benefit. Longer durations foster greater cash value accumulation, leading to higher RPU amounts. Policyholders should strategically choose policy lengths and monitor cash value growth to optimize their RPU potential. Understanding this relationship empowers individuals to make informed decisions about their insurance coverage and financial planning.

Wood Stoves and Home Insurance: Understanding Potential Premium Increases

You may want to see also

Explore related products

![]()

Steps to Apply for Reduced Paid-Up Insurance

Reduced paid-up insurance is a non-forfeiture option that allows policyholders to keep a smaller death benefit without paying future premiums. To apply for this option, you must first understand the eligibility criteria. Typically, the policy must have accumulated sufficient cash value, and the policyholder must have paid premiums for a minimum number of years, often 3 to 5, depending on the insurer. Check your policy document or contact your insurance provider to confirm these requirements.

Once eligibility is confirmed, the next step is to calculate the reduced paid-up insurance amount. This involves determining the policy's cash value and applying a formula specified by the insurer. For instance, some companies use a ratio of the policy's cash value to the original death benefit, multiplied by the original face amount. Others may provide a table or calculator to simplify the process. It’s crucial to request this calculation from your insurer to ensure accuracy, as errors can lead to unexpected reductions in coverage.

After calculating the reduced paid-up amount, formally request the conversion by submitting a written application to your insurance company. Include your policy number, the desired effective date, and any required documentation. Some insurers may also require a statement confirming your understanding of the changes, such as the reduced death benefit and the cessation of premium payments. Be prepared for a waiting period, as processing times vary by company.

Finally, review the implications of this decision. Reduced paid-up insurance permanently lowers the death benefit and eliminates the need for future premiums, but it also limits the policy’s flexibility. For example, you may no longer be able to take policy loans or increase coverage. Compare this option with alternatives like surrendering the policy for cash value or converting to extended term insurance to ensure it aligns with your financial goals. Consulting a financial advisor can provide additional clarity tailored to your situation.

Understanding the Timeline of Life Insurance Underwriting

You may want to see also

Frequently asked questions

Reduced paid-up insurance is a non-forfeiture option that allows a policyholder to keep a reduced insurance benefit without paying further premiums after stopping payments. It is calculated by dividing the total premiums paid by the total premiums required for a paid-up policy at the same rate, then multiplying the result by the original face value of the policy.

The longer the premiums were paid before stopping, the higher the reduced paid-up insurance amount will be. This is because more premiums paid contribute to a larger portion of the policy's value, resulting in a higher benefit under the reduced paid-up option.

While the insurance company typically provides the exact reduced paid-up amount, it can be estimated manually using the formula: (Total Premiums Paid / Total Premiums Required for Paid-Up Policy) × Original Face Value. However, the final amount may vary based on the insurer's specific calculations and policy terms.