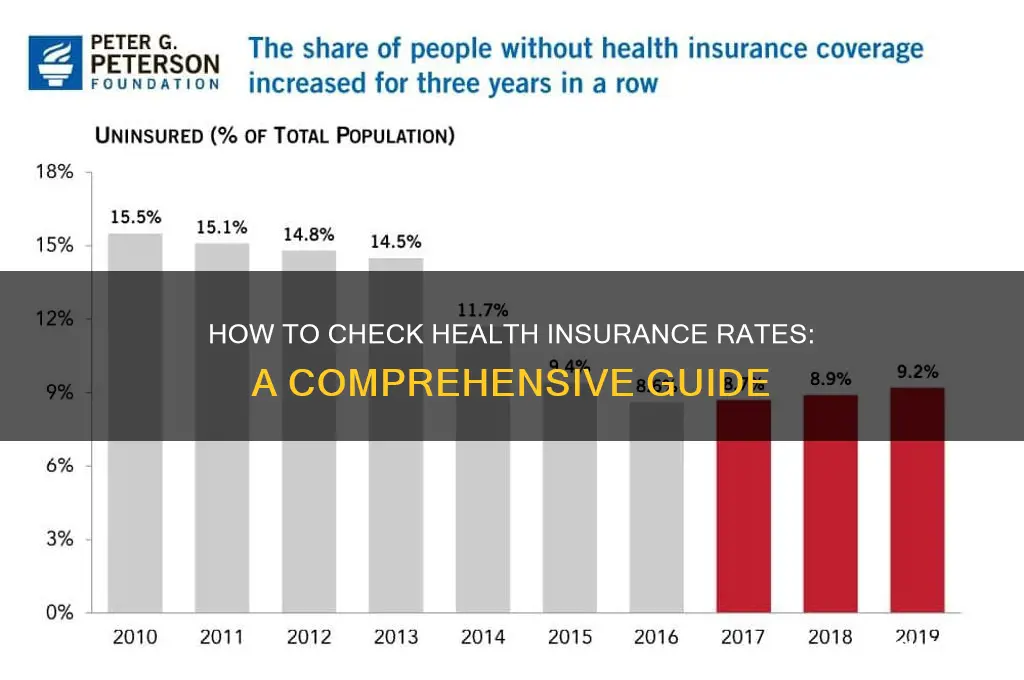

Checking health insurance rates is a crucial step in finding a plan that fits your budget and meets your healthcare needs. To begin, gather personal information such as age, location, and medical history, as these factors significantly influence premiums. Utilize online comparison tools or insurance marketplaces to explore various plans from different providers, ensuring you compare both monthly premiums and out-of-pocket costs like deductibles and copays. Additionally, consider reaching out to insurance agents or brokers for personalized guidance and to uncover potential discounts or subsidies you may qualify for, such as those available through the Affordable Care Act. Regularly reviewing and comparing rates annually during open enrollment can also help you stay informed about changes in pricing and coverage options.

Explore related products

What You'll Learn

- Compare plans online using insurance comparison tools for quick rate estimates

- Check provider networks to ensure preferred doctors and hospitals are included

- Review deductible and out-of-pocket costs to understand total expenses

- Assess coverage limits for specific services like prescriptions or maternity care

- Verify eligibility for subsidies or discounts based on income or location

![]()

Compare plans online using insurance comparison tools for quick rate estimates

One of the most efficient ways to gauge health insurance costs is by leveraging online comparison tools. These platforms aggregate data from multiple insurers, allowing you to input basic information like age, location, and coverage needs to receive instant rate estimates. For instance, tools like eHealth, Policygenius, or Healthcare.gov streamline the process by presenting side-by-side comparisons of premiums, deductibles, and out-of-pocket maximums. This approach saves time and eliminates the need to visit individual insurer websites or speak with agents for preliminary research.

However, not all comparison tools are created equal. Some may prioritize partnerships with specific insurers, potentially skewing results. To ensure accuracy, cross-reference estimates from at least two different platforms. Additionally, pay attention to the fine print regarding data privacy, as some tools may sell your information to third parties. A practical tip is to use incognito mode when browsing to avoid targeted ads that could inflate future quotes.

Another critical aspect is understanding the variables that influence the estimates. For example, a 30-year-old nonsmoker in Texas might receive a quote of $300–$500 monthly for a mid-tier plan, while a 55-year-old in California could see rates of $700–$1,200. Factors like pre-existing conditions, family size, and desired coverage level (e.g., bronze, silver, gold) significantly impact these numbers. Most tools allow you to adjust these parameters to see how they affect costs, providing a clearer picture of what to expect.

While online comparisons offer convenience, they should not replace a deeper analysis. Estimates are just that—estimates. Actual rates may vary based on additional underwriting factors or regional nuances. For instance, some insurers offer discounts for healthy lifestyles, such as gym memberships or smoking cessation programs, which might not be reflected in initial quotes. Use these tools as a starting point, then follow up with insurers directly or consult an independent broker to finalize details.

Finally, consider the timing of your search. Open enrollment periods, typically in the fall, are the best times to compare plans, as insurers update their offerings annually. However, if you qualify for a special enrollment period (e.g., due to job loss or marriage), these tools remain invaluable. Keep in mind that rates can fluctuate based on market trends, policy changes, and even your personal health status, so periodic re-evaluation is essential to ensure you’re getting the best value.

Understanding DGA Residuals and Their Impact on Health Insurance Coverage

You may want to see also

Explore related products

![]()

Check provider networks to ensure preferred doctors and hospitals are included

Provider networks are the backbone of any health insurance plan, dictating where and from whom you can receive care. Before committing to a plan, verify that your preferred doctors, specialists, and hospitals are in-network. Out-of-network providers often come with significantly higher out-of-pocket costs, sometimes rendering insurance coverage nearly useless for those visits. Start by compiling a list of your current healthcare providers, including primary care physicians, specialists, and any hospitals you’ve used or prefer. Most insurance companies offer online tools where you can input provider names or locations to check their network status. If you’re unsure, call the provider’s office directly to confirm their participation in specific insurance networks.

Consider this scenario: You’ve been seeing the same endocrinologist for years to manage a chronic condition. Switching to a new plan without verifying their network status could force you to choose between paying exorbitant out-of-network fees or starting over with a new doctor. This disruption can lead to gaps in care, especially for complex or ongoing treatments. Similarly, if you have a preferred hospital for its specialized services or proximity, ensure it’s in-network. Emergency situations or unexpected hospitalizations can quickly become financial burdens if the facility falls outside your plan’s coverage.

For families, the stakes are even higher. Pediatricians, OB/GYNs, and therapists for children or spouses must align with your chosen plan. If you’re planning for pregnancy, for instance, confirm that your preferred OB/GYN and birthing center are in-network, as maternity care costs can skyrocket without proper coverage. Use the plan’s provider directory to cross-reference your list, but don’t stop there. Directories can be outdated or incomplete, so always double-check with both the insurer and the provider’s office.

If your preferred providers aren’t in-network, weigh your options carefully. Some plans offer out-of-network coverage, but it typically comes with higher deductibles, copays, and coinsurance. Alternatively, consider whether switching providers is feasible. Ask your current doctors if they have colleagues or affiliated practices within the plan’s network. In some cases, you may find a suitable alternative without compromising care quality.

Ultimately, failing to check provider networks can undermine the value of your health insurance. What seems like a cost-effective plan on paper may become a financial strain if your trusted providers are excluded. Take the time to research thoroughly, ask questions, and prioritize continuity of care. Your health—and your wallet—will thank you.

Adding Your Newborn to Health Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

$9.98 $12.99

![]()

Review deductible and out-of-pocket costs to understand total expenses

Deductible and out-of-pocket costs are the silent architects of your healthcare expenses, often overlooked until they become a financial burden. These two components dictate how much you’ll pay before your insurance kicks in and caps your annual spending, respectively. For instance, a plan with a $1,500 deductible means you’ll cover the first $1,500 of covered medical expenses out of pocket before insurance benefits apply. Meanwhile, an out-of-pocket maximum of $5,000 limits your total yearly liability, including deductibles, copays, and coinsurance. Understanding these figures is critical, as they directly impact your budget and financial planning.

To effectively review these costs, start by comparing plans side by side. Use online tools like Healthcare.gov or insurance company websites to input your expected medical needs—such as prescriptions, specialist visits, or chronic care—and see how costs stack up. For example, a high-deductible plan might save you on monthly premiums but could leave you paying thousands upfront for unexpected surgeries or hospitalizations. Conversely, a low-deductible plan with higher premiums may offer more predictable costs but could be overkill if you’re generally healthy. Consider your health history and anticipated needs to strike the right balance.

A common pitfall is focusing solely on the deductible without accounting for other out-of-pocket costs. Coinsurance, typically a percentage of the cost of services after the deductible, can add up quickly. For instance, a 20% coinsurance on a $10,000 procedure means you’ll pay $2,000 out of pocket after meeting your deductible. Similarly, copays for doctor visits or prescriptions can accumulate, especially for those with ongoing medical needs. Always factor these into your total potential expenses to avoid surprises.

Practical tips can make this process less daunting. First, estimate your annual healthcare usage by reviewing past medical expenses or consulting with your healthcare provider. If you’re on regular medications, calculate the annual cost under different plans. Second, prioritize plans with lower out-of-pocket maximums if you have a chronic condition or anticipate significant medical needs. Finally, don’t hesitate to contact insurance providers directly to clarify cost structures or negotiate terms. Knowledge and preparation are your best tools in navigating these complexities.

In conclusion, reviewing deductibles and out-of-pocket costs isn’t just about comparing numbers—it’s about predicting your financial exposure in various scenarios. By analyzing these components thoughtfully, you can select a plan that aligns with your health needs and budget, ensuring you’re protected without overspending. This proactive approach transforms health insurance from a confusing necessity into a strategic financial decision.

Renters Insurance: Medical Coverage and Your Options

You may want to see also

Explore related products

![]()

Assess coverage limits for specific services like prescriptions or maternity care

Health insurance plans often cap coverage for specific services, leaving policyholders with unexpected out-of-pocket costs. For instance, a plan might cover only 70% of prescription drug costs after a $50 deductible, or limit maternity care to $10,000 per pregnancy. Understanding these limits is crucial for budgeting and avoiding financial surprises. Start by reviewing the Summary of Benefits and Coverage (SBC) provided by your insurer, which outlines coverage details in plain language. Look for terms like "coinsurance," "copay," and "out-of-pocket maximum" to gauge your financial responsibility.

Analyzing prescription drug coverage requires attention to tiers and formularies. Most plans categorize medications into tiers (e.g., generic, preferred brand, non-preferred brand, specialty), each with different cost-sharing structures. For example, a generic drug might cost $10, while a specialty medication could require a 30% coinsurance rate, potentially costing hundreds of dollars per month. If you take maintenance medications, such as insulin or asthma inhalers, verify if they’re covered and at what tier. Tools like the insurer’s drug lookup feature or a pharmacist consultation can help estimate costs.

Maternity care coverage varies widely, even among plans that comply with the Affordable Care Act (ACA). While ACA-compliant plans must cover prenatal visits, labor and delivery, and postpartum care, specific limits and exclusions differ. For example, some plans may restrict coverage for fertility treatments or limit the number of ultrasounds. If you’re planning a family, scrutinize the policy for details on high-risk pregnancy coverage, NICU stays, and breastfeeding support. Additionally, check if the plan requires preauthorization for certain procedures, such as a C-section, to avoid claim denials.

Comparing coverage limits across plans can highlight significant differences. For instance, Plan A might offer $5,000 for maternity care with a $2,000 deductible, while Plan B provides $15,000 with a $500 deductible. To evaluate which plan offers better value, consider your anticipated needs. If you’re expecting a high-risk pregnancy, Plan B’s higher coverage and lower deductible may outweigh its higher premium. Similarly, for prescriptions, compare the total annual cost of your medications under each plan, factoring in premiums, deductibles, and copays.

Practical tips can streamline the assessment process. First, create a checklist of essential services (e.g., prescriptions, maternity care, mental health) and prioritize them based on your needs. Second, use online tools like Healthcare.gov’s plan comparison feature or third-party platforms to analyze coverage side by side. Third, consult a broker or insurance navigator for personalized guidance, especially if you have complex medical needs. Finally, don’t overlook the provider network—ensure your preferred doctors and pharmacies are in-network to maximize coverage benefits.

Health Insurance Discrimination: Uncovering the Deadly Impact on Lives

You may want to see also

Explore related products

$12.98 $15.99

![]()

Verify eligibility for subsidies or discounts based on income or location

Income and location significantly influence health insurance costs, but many overlook the subsidies and discounts available to lower these expenses. For instance, the Affordable Care Act (ACA) offers premium tax credits for individuals earning between 100% and 400% of the federal poverty level (FPL). In 2023, this translates to an annual income range of $13,590 to $54,360 for a single person. To verify eligibility, use the Healthcare.gov subsidy calculator, which requires your household income, family size, and zip code. This tool instantly estimates potential savings, ensuring you don’t pay more than 8.5% of your income for premiums.

Geographic location also plays a critical role in subsidy eligibility. For example, residents of states that expanded Medicaid under the ACA may qualify for coverage if their income is below 138% of the FPL. In contrast, non-expansion states have stricter eligibility criteria, often leaving low-income individuals in a coverage gap. To check if your state expanded Medicaid, visit the Kaiser Family Foundation’s Medicaid expansion tracker. Additionally, some states offer their own health insurance discounts or programs, such as California’s Covered California, which provides additional financial assistance beyond federal subsidies.

The process of verifying eligibility involves gathering specific documents and completing an application. Start by collecting proof of income, such as tax returns, pay stubs, or W-2 forms. For location-based subsidies, ensure your address is accurate, as some programs have county-specific benefits. When applying through a state or federal marketplace, answer all income and household questions accurately. Errors can lead to incorrect subsidy amounts, requiring repayment at tax time. If you’re unsure, consult a certified navigator or broker who can guide you through the process.

A common misconception is that subsidies are only for the unemployed or extremely low-income individuals. In reality, middle-income earners often qualify for substantial discounts. For example, a family of four earning up to $111,000 in 2023 may still be eligible for premium tax credits. Moreover, cost-sharing reductions (CSRs) are available for those earning up to 250% of the FPL, reducing out-of-pocket costs like deductibles and copays. These reductions are only available through marketplace plans, so enrolling directly through an insurer bypasses these savings.

Finally, timing matters when verifying eligibility. Open enrollment periods typically run from November 1 to January 15, but qualifying life events (e.g., marriage, job loss) allow for special enrollment. Subsidies are applied monthly, so enrolling early maximizes savings. For example, a $200 monthly premium reduction over 12 months saves $2,400 annually. Use the marketplace’s eligibility tool to estimate savings before enrolling, and update your income information annually to avoid overpaying or losing subsidies. By leveraging these programs, you can significantly reduce health insurance costs tailored to your income and location.

Selling Medicaid Health Insurance in Colorado: Profitable?

You may want to see also

Frequently asked questions

You can compare health insurance rates by using online comparison tools, visiting insurance company websites, or consulting with a licensed insurance broker. Provide your personal details, such as age, location, and coverage needs, to receive accurate quotes.

Health insurance rates are influenced by factors like age, location, tobacco use, pre-existing conditions, coverage level, and the type of plan (e.g., HMO, PPO). Additionally, family size and income (for subsidized plans) can impact costs.

While you can get general estimates without personal information, accurate rate quotes typically require details like age, ZIP code, and health status. Providing this information ensures the rates reflect your specific circumstances.

Health insurance rates can change annually during open enrollment periods or when life events (e.g., marriage, job loss) qualify you for a special enrollment period. It’s advisable to check rates yearly or whenever your coverage needs or circumstances change.