Choosing the right health insurance plan in the USA can be overwhelming, especially for newcomers. With a complex healthcare system and a wide range of options, it’s essential to understand the basics before making a decision. Key factors to consider include your budget, coverage needs, network of providers, and whether you qualify for government-subsidized plans like Medicaid or Affordable Care Act (ACA) marketplace plans. Familiarize yourself with terms like premiums, deductibles, copayments, and out-of-pocket maximums, as these will impact your overall costs. Additionally, consider your health status, anticipated medical needs, and whether you prefer a broader network of doctors or lower monthly premiums. Researching plans through the Health Insurance Marketplace or consulting with a licensed insurance broker can help you navigate the process and find a plan that aligns with your unique circumstances.

Explore related products

What You'll Learn

- Understand U.S. Healthcare Basics: Learn about HMOs, PPOs, deductibles, copays, and out-of-pocket maximums

- Assess Your Health Needs: Evaluate current health, medications, and potential future medical requirements

- Compare Plan Types: Marketplace, employer-sponsored, private, or government plans (Medicaid, Medicare)

- Check Network Coverage: Ensure preferred doctors, hospitals, and specialists are in-network

- Review Costs: Premiums, deductibles, copays, and subsidies to fit your budget

![]()

Understand U.S. Healthcare Basics: Learn about HMOs, PPOs, deductibles, copays, and out-of-pocket maximums

Navigating the U.S. healthcare system can feel like deciphering a foreign language, especially for newcomers. Terms like HMOs, PPOs, deductibles, copays, and out-of-pocket maximums are thrown around, leaving many scratching their heads. Understanding these basics is crucial for making informed decisions about health insurance. Let's break it down.

HMOs (Health Maintenance Organizations) and PPOs (Preferred Provider Organizations) are the two most common types of health insurance plans. HMOs typically offer lower premiums and out-of-pocket costs but require you to choose a primary care physician (PCP) and get referrals to see specialists. They also limit coverage to in-network providers, meaning you'll pay more (or nothing at all) if you go out-of-network. PPOs, on the other hand, offer more flexibility in choosing healthcare providers, both in-network and out-of-network, but usually come with higher premiums and out-of-pocket costs. Consider your healthcare needs, budget, and preferred level of flexibility when deciding between these two options.

Deductibles, copays, and out-of-pocket maximums are essential components of any health insurance plan, yet they're often misunderstood. A deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. For instance, if your plan has a $1,000 deductible, you'll be responsible for paying the first $1,000 of covered medical expenses. Copays, typically a fixed amount (e.g., $20 or $50), are what you pay for specific services, such as doctor visits or prescription drugs. Out-of-pocket maximums, usually ranging from $1,000 to $7,000, cap the total amount you'll pay for covered services in a given year. Once you reach this limit, your insurance will cover 100% of the costs. Be sure to review these details carefully when comparing plans.

To illustrate, let's consider a hypothetical scenario. Imagine you're a 30-year-old individual with no pre-existing conditions, looking for a health insurance plan. You've narrowed it down to two options: an HMO with a $1,500 deductible, $20 copays, and a $5,000 out-of-pocket maximum, and a PPO with a $3,000 deductible, $50 copays, and a $7,000 out-of-pocket maximum. If you prioritize lower costs and don't mind the restrictions of an HMO, the first option might be more appealing. However, if you value flexibility and can afford higher premiums, the PPO could be a better fit.

When choosing a health insurance plan, it's essential to consider your unique circumstances and healthcare needs. If you have a chronic condition requiring frequent specialist visits, a PPO might be more suitable, despite the higher costs. On the other hand, if you're generally healthy and only need occasional preventive care, an HMO could provide adequate coverage at a lower cost. Additionally, keep in mind that some plans offer wellness programs, telemedicine services, or prescription drug coverage, which can add value to your overall healthcare experience. By understanding the nuances of HMOs, PPOs, deductibles, copays, and out-of-pocket maximums, you'll be better equipped to select a plan that meets your needs and budget.

Practical tips for newcomers to the U.S. healthcare system include: researching plans during open enrollment periods (typically November-December), considering your expected healthcare usage for the upcoming year, and seeking guidance from a licensed insurance broker or navigator. Remember, the cheapest plan isn't always the best value – carefully evaluate the costs, benefits, and restrictions of each option. By taking the time to understand these basics, you'll be well on your way to making an informed decision about your health insurance coverage in the U.S.

Who Regulates Florida's Insurance Companies: Understanding the Governing Bodies

You may want to see also

Explore related products

![]()

Assess Your Health Needs: Evaluate current health, medications, and potential future medical requirements

Your health is your most valuable asset, and understanding its current state is the cornerstone of choosing the right insurance plan. Begin by taking stock of your overall health. Are you managing any chronic conditions like diabetes, hypertension, or asthma? Do you have a family history of diseases that might require specialized care? For instance, if you’re a 35-year-old with a family history of heart disease, you’ll want a plan that covers preventive cardiology services, such as regular cholesterol screenings and stress tests. Similarly, if you’re pregnant or planning to start a family, maternity care and pediatric services should be a priority.

Next, evaluate your current medications. Are you on daily prescriptions like insulin (e.g., 10–20 units per day) or blood pressure medication (e.g., 5 mg of Lisinopril)? Insurance plans vary widely in their prescription drug coverage, often categorizing medications into tiers with different copays. For example, a Tier 1 drug might cost $10, while a Tier 3 specialty drug could be $100 or more. Make a list of your medications and their dosages, then compare it against the plan’s formulary to ensure affordability.

Don’t overlook potential future medical requirements. If you’re an active 25-year-old with no current health issues, consider whether you engage in high-risk activities like skiing or cycling, which could lead to injuries requiring emergency care. Alternatively, if you’re over 50, think about age-related concerns like joint replacements or cataract surgery. Plans with lower deductibles and robust specialist networks may offer better value in these scenarios.

Practical tip: Use a health needs checklist to streamline this process. Include sections for current conditions, medications, anticipated procedures (e.g., dental implants or physical therapy), and preventive care needs (e.g., annual mammograms or colonoscopies). This structured approach ensures nothing slips through the cracks and helps you communicate your needs clearly to insurance providers or brokers.

Finally, consider the flexibility of the plan. If your health needs are likely to evolve—say, you’re planning to expand your family or anticipate a career change that might affect your activity level—opt for a plan with a broad network of providers and comprehensive coverage. While it may cost more upfront, it could save you from unexpected out-of-pocket expenses down the line. By thoroughly assessing your health needs today and anticipating future requirements, you’ll be better equipped to choose a plan that safeguards your well-being in the U.S.

Will Insurance Cover Breast Reduction Surgery? What You Need to Know

You may want to see also

Explore related products

$33.74 $245.95

![]()

Compare Plan Types: Marketplace, employer-sponsored, private, or government plans (Medicaid, Medicare)

Understanding the landscape of health insurance in the U.S. begins with recognizing the distinct categories available: Marketplace, employer-sponsored, private, and government plans like Medicaid and Medicare. Each type serves different needs, eligibility criteria, and financial situations, making it crucial to compare them carefully. For instance, Marketplace plans are ideal for individuals without employer coverage, while Medicaid caters to low-income families and individuals. Knowing these differences is the first step in making an informed decision.

Analytical Breakdown: Marketplace plans, offered through Healthcare.gov, provide a range of options categorized by metal tiers (Bronze, Silver, Gold, Platinum) that balance premiums and out-of-pocket costs. Employer-sponsored plans often share costs between the employer and employee, typically offering lower premiums but limited flexibility in choosing providers. Private plans, purchased directly from insurers, offer customization but can be expensive. Government plans like Medicaid and Medicare are need-based: Medicaid for low-income individuals and Medicare for those aged 65+ or with specific disabilities. Each plan type has unique advantages, but eligibility and cost-sharing structures vary widely.

Instructive Steps: To compare effectively, start by assessing your eligibility. If you’re employed, check if your employer offers health insurance—this is often the most cost-effective option. If not, visit Healthcare.gov to explore Marketplace plans, where you may qualify for subsidies based on income. For low-income individuals, apply for Medicaid through your state’s health department. If you’re 65 or older, enroll in Medicare, ensuring you sign up during the Initial Enrollment Period to avoid penalties. Private plans are a last resort for those seeking specific coverage but come with higher costs.

Comparative Insights: Employer-sponsored plans often provide comprehensive coverage at a lower cost due to employer contributions, but they lack portability if you change jobs. Marketplace plans offer flexibility and potential subsidies but may have limited provider networks. Private plans provide the most customization but are the most expensive. Government plans like Medicaid and Medicare are highly affordable but come with strict eligibility requirements. For example, Medicaid covers essential health benefits with minimal or no premiums, while Medicare Part A is premium-free for most enrollees but requires additional coverage for comprehensive care.

Practical Tips: When comparing plans, consider your health needs, budget, and long-term stability. If you’re young and healthy, a Bronze Marketplace plan with lower premiums might suffice. Families or those with chronic conditions may benefit from Gold or employer-sponsored plans with lower deductibles. Always check provider networks to ensure your preferred doctors are included. For government plans, verify eligibility early—Medicaid applications can take weeks, and Medicare enrollment has strict deadlines. Lastly, use tools like Healthcare.gov’s plan comparison feature to evaluate costs and coverage side by side.

Life Insurance Agents: Accessing Your Medical Records

You may want to see also

Explore related products

![]()

Check Network Coverage: Ensure preferred doctors, hospitals, and specialists are in-network

One of the first steps in choosing a health insurance plan in the USA is to verify the network coverage. This is crucial because out-of-network services can be significantly more expensive, often leaving you with unexpected bills. Start by making a list of your preferred healthcare providers, including primary care physicians, specialists, and hospitals. Most insurance companies have an online provider directory where you can search for these names. If you’re unsure who your preferred providers are, consider asking for recommendations from friends, colleagues, or local community groups. Once you have your list, cross-reference it with the insurance plan’s network to ensure compatibility. This simple step can save you both money and stress in the long run.

Analyzing network coverage goes beyond just checking names on a list. It involves understanding the nuances of in-network versus out-of-network costs. For instance, some plans may cover out-of-network services but at a much higher coinsurance rate, typically 50% or more, compared to 20% for in-network care. Additionally, certain plans might require a referral from your primary care physician to see a specialist, which could limit your flexibility. If you have a chronic condition or require specialized care, ensure that the specialists you need are not only in-network but also accepting new patients. Calling the provider’s office directly to confirm their participation in the plan can be a prudent step, as online directories are not always up-to-date.

A persuasive argument for prioritizing network coverage is the potential for long-term financial stability. Out-of-network charges can quickly escalate, especially for complex procedures or emergency care. For example, an out-of-network emergency room visit could result in a bill that is thousands of dollars higher than an in-network visit. If you’re on a tight budget or prefer predictable healthcare costs, selecting a plan with a robust network that aligns with your needs is essential. Moreover, in-network providers often have pre-negotiated rates with the insurance company, which can significantly reduce your out-of-pocket expenses. This makes network coverage a cornerstone of cost-effective healthcare planning.

Comparing network coverage across different plans can be illuminating. For instance, a Health Maintenance Organization (HMO) typically has a narrower network but lower premiums, while a Preferred Provider Organization (PPO) offers more flexibility with a broader network but at a higher cost. If you value having more provider options, a PPO might be worth the extra expense. Conversely, if you’re comfortable with a primary care physician coordinating your care and don’t mind a limited network, an HMO could be a more economical choice. Evaluating your priorities—whether it’s cost, flexibility, or specific providers—will help you make an informed decision.

Finally, a practical tip for newcomers to the USA is to consider the geographic reach of the network, especially if you travel frequently or plan to move. Some insurance plans have regional networks, while others offer national coverage. If you’re relocating for work or study, ensure that the plan’s network extends to your new location. Additionally, if you have family or frequently visit another state, check if the plan provides out-of-area coverage for emergencies or urgent care. Taking these factors into account will ensure that your health insurance remains effective and relevant, no matter where life takes you.

Medicaid's Reach: Insuring Millions of Americans

You may want to see also

Explore related products

![]()

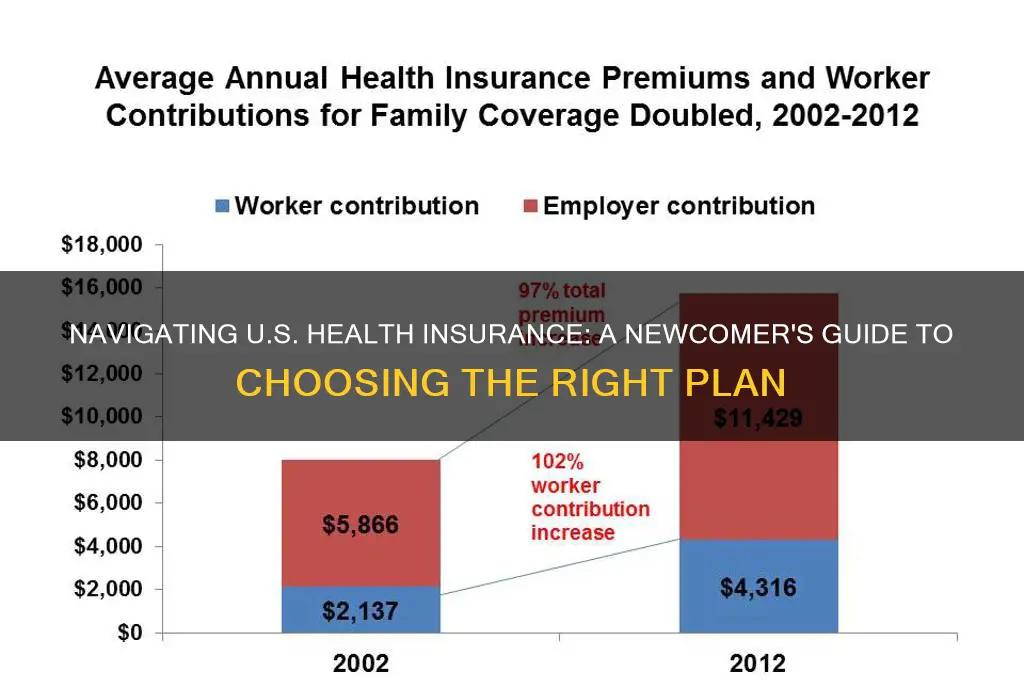

Review Costs: Premiums, deductibles, copays, and subsidies to fit your budget

Understanding the financial aspects of health insurance is crucial when navigating the U.S. healthcare system, especially for newcomers. The cost structure can be complex, but breaking it down into its components—premiums, deductibles, copays, and subsidies—can help you make an informed decision that aligns with your budget.

Premiums: The Monthly Commitment

Premiums are the recurring payments you make to maintain your health insurance coverage, typically billed monthly. Think of them as your membership fee to access healthcare services. For instance, a young adult in their 20s might find plans with premiums ranging from $200 to $400 per month, while older individuals or families could face higher costs. When evaluating premiums, consider your overall financial health. A lower premium might seem attractive, but it often comes with higher out-of-pocket costs when you need care. Conversely, a higher premium may offer more comprehensive coverage with lower deductibles and copays. Use online tools like Healthcare.gov to compare plans side by side and estimate your total annual cost, including premiums and expected out-of-pocket expenses.

Deductibles: The Out-of-Pocket Threshold

Deductibles are the amount you must pay out of pocket before your insurance coverage kicks in. For example, if your plan has a $2,000 deductible, you’ll pay the first $2,000 of covered medical expenses before the insurance starts paying its share. Plans with high deductibles (often $5,000 or more) usually have lower premiums but require you to shoulder more costs upfront. These plans are ideal if you’re generally healthy and don’t anticipate frequent medical visits. However, if you have chronic conditions or expect regular medical care, a lower deductible plan might save you money in the long run, despite higher monthly premiums.

Copays and Coinsurance: Sharing the Burden

Copays are fixed amounts you pay for specific services, such as $25 for a doctor’s visit or $10 for a prescription. Coinsurance, on the other hand, is a percentage of the cost you share with your insurer after meeting your deductible. For instance, if your plan has 20% coinsurance, you’ll pay 20% of the cost of a medical service, and your insurer covers the remaining 80%. When reviewing plans, consider how often you’ll use these services. A plan with low copays might be worth a slightly higher premium if you visit the doctor frequently. Conversely, if you rarely seek medical care, a plan with higher copays and lower premiums could be more cost-effective.

Subsidies: Financial Relief for Eligible Individuals

If you’re concerned about affordability, subsidies can significantly reduce your insurance costs. The Affordable Care Act (ACA) offers premium tax credits to individuals and families with incomes between 100% and 400% of the federal poverty level. For example, a single person earning up to $54,360 annually (as of 2023) may qualify for assistance. These subsidies lower your monthly premiums, making comprehensive coverage more accessible. Additionally, cost-sharing reductions (CSRs) can reduce deductibles and copays for those with incomes up to 250% of the poverty level. Use the Healthcare.gov subsidy calculator to estimate your eligibility and potential savings.

Practical Tips for Cost-Effective Choices

Start by assessing your healthcare needs and budget. If you’re healthy and rarely visit the doctor, a high-deductible plan paired with a health savings account (HSA) might offer tax advantages and lower premiums. For families or individuals with ongoing medical needs, a plan with higher premiums but lower out-of-pocket costs could provide better value. Always read the fine print to understand what services are covered and at what cost. Finally, don’t overlook the importance of preventive care, which is often fully covered under ACA-compliant plans, helping you avoid costly treatments down the line.

By carefully reviewing premiums, deductibles, copays, and available subsidies, you can select a health insurance plan that not only fits your budget but also provides the coverage you need to thrive in the U.S.

Medicaid vs Employer Insurance: Making the Right Choice

You may want to see also

Frequently asked questions

Consider your budget, coverage needs, network of providers, deductibles, copays, and whether the plan includes essential health benefits like preventive care, prescription drugs, and emergency services.

Yes, you can enroll in health insurance plans through the Health Insurance Marketplace or private insurers. If you’ve recently moved, you may qualify for a Special Enrollment Period outside the regular Open Enrollment Period.

HMO (Health Maintenance Organization) plans typically require you to choose a primary care physician and use in-network providers, while PPO (Preferred Provider Organization) plans offer more flexibility to see out-of-network providers at a higher cost. Choose based on your preference for cost vs. flexibility.

Yes, some states offer health insurance programs for immigrants, and you may qualify for Medicaid or Marketplace plans depending on your immigration status and income. Check with your state’s health insurance marketplace for eligibility.