Choosing a Medicare supplement insurance plan can be overwhelming, but it doesn't have to be. There are a few steps you can take to help you pick the right plan for your needs. First, it's important to understand what Medigap is and how it works. Medigap, or Medicare Supplement Insurance, is a supplemental insurance policy that helps cover the out-of-pocket costs of Medicare. It's designed to fill the gaps in coverage left by original Medicare, and it's offered by private insurance companies. Next, you'll want to compare the different Medigap plans available in your state, considering factors such as monthly premiums, deductibles, and coverage amounts. Finally, match your needs to the policy that best addresses them, taking into account your current and future health care needs, budget, and preferences for choosing your own doctors and hospitals. It's important to buy a policy during your Medigap Open Enrollment Period, as you may not be able to switch policies later.

| Characteristics | Values |

|---|---|

| Time of purchase | During the Medigap Open Enrollment Period |

| Plan selection | Compare benefits of each lettered plan, considering current and future health care needs and budget |

| Plan availability | Not all plans are offered in every state, and not all insurance companies sell policies for all plans |

| Company selection | Buy a Medigap policy from any licensed insurance company in your state |

| Company comparison | Compare the same lettered plan offered by different insurance companies |

| Company practices | Watch out for illegal practices by insurance companies |

| Company communication | Ask for an official quote and a clearly worded summary of the policy |

| Policy start date | Generally, Medigap policies begin the first of the month after you apply |

| Policy receipt | Call your insurance company if it's been 30 days without receiving your Medigap policy, and your State Insurance Department if it's been 60 days |

| Policy switching | You might not be able to switch policies later, and insurance companies are not required to sell Medigap policies after the Medigap Open Enrollment Period ends |

| Policy protection | Medigap policies must follow federal and state laws designed to protect consumers |

| Additional resources | Contact your local State Health Insurance Assistance Program (SHIP) for free help, and use Medicare.gov's Medigap Policy Finder |

Explore related products

What You'll Learn

![]()

Understanding your Medicare supplemental insurance options

Medicare Supplemental Insurance Options:

Medicare supplemental insurance, also known as Medigap, is a type of private insurance policy that fills the gaps in original Medicare coverage (Part A and Part B). These policies help cover the out-of-pocket costs associated with Medicare, including deductibles, copayments, and coinsurance. Medigap policies are identified by letters, with each plan offering different benefits and coverage levels.

Comparing Medigap Plans:

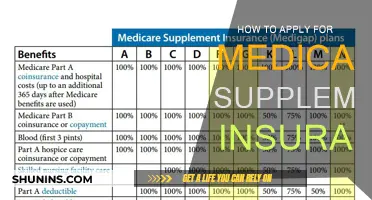

When comparing Medigap plans, it's crucial to understand the differences between the lettered plans. Plans with the same letter offer the same benefits regardless of the insurance company, so it's important to compare Plan A from one company with Plan A from another. Consider factors such as monthly premiums, deductibles, and coverage for specific health needs. Evaluate your current and future health status, including any chronic conditions, to choose a plan that covers your anticipated out-of-pocket expenses adequately.

Choosing the Right Plan:

Selecting the most suitable Medigap plan involves matching your needs to the policy that best addresses them. Consider your current and future health care requirements, your budget, and your preferences for choosing your own doctors and hospitals. If you have specific health concerns or frequent doctor visits, a plan with more comprehensive coverage for out-of-pocket expenses might be beneficial. On the other hand, if you're generally healthy, a high-deductible plan may be a more cost-effective option.

Enrollment and Coverage:

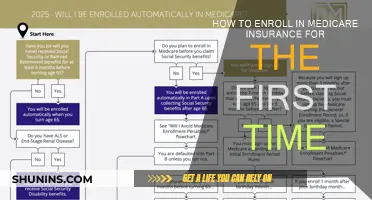

It's important to be mindful of the Medigap Open Enrollment Period, as you may not be able to switch policies later. During this period, insurance companies are required to sell you a Medigap policy, regardless of any pre-existing health conditions. Remember that Medigap policies typically take effect on the first of the month after you apply. If you don't receive your Medigap card or proof of insurance within 30 days, contact your insurance company.

Seeking Assistance:

Choosing a Medicare supplemental insurance plan can be overwhelming, so don't hesitate to seek help. Contact your local State Health Insurance Assistance Program (SHIP) to receive free counselling and guidance in choosing the right plan for your needs. They may also provide a Medigap rate comparison shopping guide for your state. Additionally, Medicare.gov offers an online tool called the Medigap Policy Finder to explore different Medigap policy options.

Canceling Insurance Post-Procedure: What's the Soonest You Can Do It?

You may want to see also

Explore related products

$19.95 $14.95

$5.99

![]()

Comparing health and drug plans

When comparing health and drug plans under Medicare Supplement Insurance, also known as Medigap, there are several factors to consider. Medigap offers additional coverage to fill the gaps in Original Medicare, and there are different plans available with varying benefits and costs. Here are some key considerations to keep in mind when comparing health and drug plans:

Plan Benefits

Medigap plans offer a range of benefits, including cost-sharing coverage, freedom to choose healthcare providers, coverage for foreign travel emergency services, and no network restrictions. Evaluate the specific benefits offered by each plan and choose the one that best aligns with your healthcare needs and preferences. Some plans, like Plans K and L, show how much they'll contribute towards approved services before you meet your out-of-pocket yearly limit, providing clarity on your financial responsibility.

Cost Considerations

Evaluate the premium costs, deductibles, coinsurance, and copayments associated with each plan. Consider your budget and determine how much you are willing and able to pay for healthcare services. Plans with higher premiums may offer more comprehensive coverage, while plans with lower premiums may have higher out-of-pocket costs when you require medical services. Additionally, some plans like Plans F and G offer a high-deductible option, where you must pay a significant amount out-of-pocket before the Medigap policy contributes.

Your Healthcare Needs

Discuss your healthcare needs with your primary care physician or specialists. They can provide valuable guidance based on your medical history and treatment requirements. Consider any ongoing health conditions, potential future healthcare requirements, and your personal preferences for receiving medical care. This will help you choose a plan that adequately covers your specific needs.

Enrollment Periods

Be mindful of the Medigap Open Enrollment Period (OEP), which occurs once a year and lasts for six months, starting when you turn 65 and enroll in Medicare Part B. During this period, you have guaranteed issue rights, meaning you can apply for any Medigap plan available in your state, and insurance companies must accept your application regardless of pre-existing conditions. If you miss the OEP, you may still apply for a Medigap plan, but you could be subject to medical underwriting and may face higher premiums or even denial of coverage.

Comparison and Choice

Take the time to compare multiple insurance plans and providers. Utilize online comparison tools, speak with licensed insurance agents, and review plan details thoroughly. Consider not just the costs but also the benefits, customer service, and any additional perks offered. Remember, choosing the right insurance plan is a personal decision based on your unique circumstances, so gather all the necessary information to make a well-informed choice that best suits your healthcare and financial needs.

Supplemental Medical Insurance: FSA Eligibility Explained

You may want to see also

Explore related products

![]()

Considering your current and future health needs

When choosing a Medicare Supplement Insurance plan, it's important to consider your current and future health needs. This involves matching your needs to the policy that best addresses them. Here are some key factors to think about:

Current Health Status

Consider any chronic conditions you may have and choose a plan that covers more out-of-pocket expenses. If you frequently visit multiple doctors or specialists, you may prefer a plan that offers a wider network of healthcare providers.

Future Health Needs

Anticipate any potential changes in your health and choose a comprehensive plan that can adapt to your needs. This can help you save money if your health declines or if you require unexpected medical care.

Affordability

Evaluate the cost of premiums, deductibles, and other out-of-pocket expenses to ensure the plan fits within your budget. Consider the potential impact on your finances, especially after retirement, and choose a plan that offers financial protection.

Choice of Doctors and Hospitals

If having the freedom to choose your own doctors and hospitals is important to you, ensure that the plan allows for this. Check the network of healthcare providers associated with the plan to make sure your preferred choices are included.

Medigap Open Enrollment Period

Keep in mind that you may only be able to switch policies during your Medigap Open Enrollment Period. In most states, insurance companies are not required to sell you a Medigap policy outside of this period, except under specific circumstances. Therefore, it's crucial to carefully consider your current and future health needs before making a decision.

By taking the time to understand your Medicare supplemental insurance options and considering your current and future health needs, you can make an informed choice that best aligns with your personal circumstances.

Best Medical Insurance Rates: Who's Offering the Most Affordable Plans?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Matching your needs to the policy

Choosing a Medicare supplement insurance plan involves matching your needs to the policy that best addresses them. Here are some key considerations to help you make an informed decision:

Current Health Status

Consider your current health condition and any chronic illnesses or multiple conditions you may have. If you have ongoing health issues, look for a plan that covers more out-of-pocket expenses. For example, if you regularly see multiple specialists, a traditional Plan F, as recommended by Reva Sheehan, senior director of customer insights at mPulse Mobile, may be suitable.

Future Health Needs

Think about your anticipated future health needs. Choosing a comprehensive plan can help you save money if your health declines or unexpected medical issues arise. This is especially important if you anticipate a decline in your health or if you want to be prepared for potential high-cost medical care.

Affordability

Evaluate the cost of premiums, deductibles, and other out-of-pocket expenses associated with each plan. Consider your budget and financial situation to ensure the plan you choose is affordable for you. Remember that the goal is to choose a plan that provides the coverage you need at a cost that fits within your financial means.

Choice of Doctors and Hospitals

If having the freedom to choose your own doctors and hospitals is important to you, ensure that the plan you select allows for this. Some plans may have restrictions or require you to choose from a specific network of healthcare providers. Check the details of each plan to make sure they align with your preferences and expectations for healthcare provider choices.

Availability in Your State

Keep in mind that not all plans are offered in every state. Check the availability of the plans you are interested in for your specific state. Additionally, understand that insurance companies are not required to sell you a Medigap policy outside of your Medigap Open Enrollment Period, except under specific circumstances.

By carefully considering these factors and matching them to the policy options, you can make a well-informed decision when choosing a Medicare supplement insurance plan that best suits your needs.

Traveling to Greece? US Medical Insurance Coverage Explained

You may want to see also

Explore related products

![]()

Knowing when to buy a policy

The best time to buy a Medicare Supplement Insurance policy, also known as a Medigap policy, is during your Medigap Open Enrollment Period. In most states, if you apply after your first six months of Medicare eligibility, insurance companies are not obligated to sell you a Medigap policy, except under specific circumstances. Therefore, it is important to be aware of your Medigap Open Enrollment Period and plan to buy a policy during that time.

You can explore different Medigap policy options using Medicare.gov's Medigap Policy Finder. This tool allows you to select the year you need coverage, your ZIP code, and your county to review your Medicare supplemental insurance plan options. You can then compare the benefits of each lettered plan, considering your current and future health care needs, to decide which benefits you need.

It is important to note that not all plans are offered in every state, and even if a state offers a particular plan, not all insurance companies sell policies for it. Therefore, when choosing a plan, you should also consider which insurance companies sell the plan you want and whether they are licensed to sell policies in your state.

Additionally, be mindful of potential illegal practices by insurance companies and protect yourself when shopping for a Medigap policy. You can contact your local State Health Insurance Assistance Program (SHIP) to get free help choosing an insurance company in your area and ask if they have a "Medigap rate comparison shopping guide" for your state.

Understanding the Duration of Medical Insurance Coverage

You may want to see also

Frequently asked questions

Medigap is a supplemental insurance policy that helps cover the out-of-pocket costs of Medicare. It is also known as Medicare Supplement Insurance.

Choosing a Medigap plan involves matching your needs to the policy that best addresses them. Consider your current and future health care needs, the cost of premiums, deductibles, and other out-of-pocket expenses. You can explore different Medigap policy options using Medicare.gov's Medigap Policy Finder.

The best time to buy a Medigap policy is during your Medigap Open Enrollment Period. In most cases, you cannot change your Medigap coverage outside of this period.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)